The title of this post covers a lot of ground, but the answer is identical for all three cases.

The questions . . .

Would it be a good thing if interest rates rose?

Would it be a good thing if copper prices rose?

Would it be a good thing if the dollar appreciated?

. . . are all basically meaningless. In all three cases, the prices never change for no reason at all. In each case the real question is whether the thing that causes the price to change makes us better off or worse off.

In all three cases, the price/interest rate/exchange rate might rise due to strong economic growth in America. That would probably be a good thing. The exchange rate and the interest rate might rise due to tight money. That would be a bad thing if tight money were not appropriate at that time. Copper prices might rise because of civil wars in copper producing nations. That would be a bad thing.

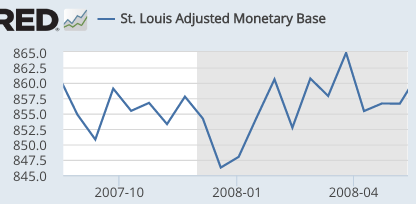

This isn’t just a minor problem; the economics profession is waste waist deep in reasoning from a price change. You can make a pretty good argument that reasoning from a price change caused the Great Recession. Most economists thought the fall in interest rates from August 2007 to May 2008 was caused by expansionary monetary policy. Not so. NGDP growth slowed, and if you are still one of those people who looks at how much money the government was actually producing, then the answer is the same. Growth in the monetary base basically stopped between August 2007 and May 2008.

The fall in interest rates from 5.25% in August 2007 to 2% in May 2008 was entirely due to a weak economy—the Fed had absolutely nothing to do with it. A more expansionary monetary policy that kept NGDP growth expectations at 5% would have led to a smaller fall in interest rates.

Almost every day I see examples of economists, including Nobel laureates, engaged in the EC101 mistake of reasoning from a price change. It needs to stop, as it is causing a lot of damage to the economy.

PS. Another misleading question is: “Should the government take steps to cause an increase in prices, interest rates or exchange rates?” The answer entirely depends on which steps they take. In late 2008, a government step to implement NGDPLT at 5% might have raised interest rates. In late 2008, an increase in the fed funds target might have raised interest rates. One would have been an expansionary policy, and the other would have been a contractionary policy. If you are simply talking about interest rates, you are not part of the solution; you are part of the problem.

PPS. And it does not help to mention “ceteris paribus”. If ceteris are paribus, then prices do not change.

READER COMMENTS

dlr

Feb 10 2017 at 1:01pm

the economics profession is waste deep in reasoning

that’s a bit on the knows, Scott, even for you 😉

marcus nunes

Feb 10 2017 at 1:09pm

They talk (reason) from price/interest rate changes and completely forget about money and mon policy!

http://ngdp-advisers.com/2017/02/08/fantasy-world-conventional-central-bankers-money-no-role/

Philo

Feb 10 2017 at 4:21pm

“Waste” deep–are those bodily wastes?

Philo

Feb 10 2017 at 4:26pm

Twentieth-century analytic philosophy struggled mightily with making sense of counterfactual conditional statements. This post suggests why the problem was so messy.

bill

Feb 10 2017 at 6:54pm

Some prices can be changed by fiat.

IOR, minimum wages, pegged currencies.

Andrew_FL

Feb 10 2017 at 6:57pm

But the bad thing here is the wars, not the price increasing. It would be worse, actually, in the same circumstances if prices did not rise.

AK

Feb 10 2017 at 7:18pm

If you zoom out on the graph for the monetary base, it looks like absolutely nothing happened over this time period.

https://fred.stlouisfed.org/series/BASE

Can you do a post elaborating on this?

Nick Ronalds

Feb 10 2017 at 8:50pm

Max Planck said science progresses “one funeral at a time”. Perhaps the same can be said for most fields, including economics. As an amateur economist I have now internalized Scott’s dictum, DRFAPC, but few of his professional peers seem to have learned it. Maybe Perhaps it also illustrates that the most important economic truths are pretty simple. TAANSTAFL, DRFAPC, and supply and demand curves are surprisingly powerful, as long as you distinguish movements along a curve from movements of the curve itself. How about a good acronym for that?

David Henderson has a great set of Ten Pillars of economic wisdom, here, http://www.econlib.org/archives/2012/04/the_ten_pillars.html. It includes TAANSTAFL but maybe it still needs DRFAPC to be completed?

Come to think of it, most economists don’t seem to believe TAANSTAFL either.

Thomas Sewell

Feb 11 2017 at 12:33am

@bill:

Are you truly changing a price (in terms of the information content) in those situations, or are you merely artificially preventing some of the transactions which would otherwise have been part of the market the price normally represents?

Example: If you pass a law stating no one may hire an employee for less than $15/hour, are you changing the price of employee labor which was previously offered and accepted for $5/hour, or are you just removing those previously agreed upon transactions from the market going forward? Or some of both, a mix of price adjustment and transaction exclusion?

Scott Sumner

Feb 11 2017 at 2:09pm

dlr, My writing style stinks.

Thanks Marcus.

bill, That’s right, and those have very specific effects, which often differ from price moves due to S&D shifts.

Andrew, Yes.

AK, The monetary base rose from 2000 to 2007, and then stopped rising. This slowdown in base growth triggered the recession. After 2008, demand for base money soared for two reasons:

1. Near zero rates.

2. Interest on reserves.

Thanks Nick, I’m working hard to make people more aware of the problem.

Mike W

Feb 12 2017 at 9:49am

“During that sit-down, on Nov. 29, Mr. Cohn [president of Goldman Sachs] briefed Mr. Trump on what he regarded as the chief hurdle to expanding the economy, according to people who were briefed on the discussion: a stronger dollar, which would undermine efforts to create jobs.” (NYT, https://www.nytimes.com/2017/02/11/business/dealbook/trump-economic-cabinet-gary-cohn.html?ref=business )

Reasoning from a price change?

Kevin Erdmann

Feb 12 2017 at 10:50pm

Scott, it looks to me like the slowdown in base growth dates to early 2006.

Scott Sumner

Feb 13 2017 at 10:17am

Mike, Yes, unless Cohn is implicitly assuming that he knows why the dollar has strengthened. It may well have strengthened due to expectations of a strong economy!

Kevin, Yes, that’s correct.

Thaomas

Feb 13 2017 at 6:13pm

This is an odd and confusing way to make a good point.

Economist “called” the reduction in the Fed’s target interest rate “expansionary” (not sure who actually said that, but I’ll stipulate) as it indeed was, relative to not reducing the rate. The problem was that their labeling of the Fed’s use of its interest rate instrument in this way did not help make the case for more vigorous use of other instruments like purchases of longer term assets or foreign exchange assets so as to at lest keep the price level and price level expectations growing at the target rate and to prevent unemployment from increasing.

There was a lot of political pressure in 2008-16 coming from the media and the Fed Regional banks to be very cautious about vigorous use of instruments like QE and to keep a virtual ceiling on inflation rates. The Fed gave in to these pressures and refused to follow its mandate, barely tried, and did not apologize for going against the instruction of Congress.

The failure to use monetary policy to maintain price stability and maximum employment was demonstrated by the fall in NGDP. To call that fall the policy is almost tautological. In your bus analogy if the bus veers off the road should be conclude that was the drivers policy?

Comments are closed.