Here’s Bloomberg:

President Donald Trump will select three members of the Federal Reserve board during his term in office, including a replacement chair for Janet Yellen when her appointment expires early next year. He should seize the chance to refresh the Fed with faces from the business community, adding executives to the roster of PhD economists who currently run monetary policy in most of the world.

If we are going to look beyond PhD economists then why not consider plumbers or hair stylists? What sort of knowledge do business executives bring to the table?

The Fed appointments come at a key juncture in U.S. economic policy, one that makes business knowhow an even more valuable commodity for a rate-setter than usual. Trump’s fiscal policies will set a new backdrop for the monetary policy environment, given his intention to cut personal and business tax rates and boost investment in the nation’s infrastructure.

So appointing executives to the Fed who’ve had to take fiscal and monetary policy into account when making decisions on where and when to build new factories or make other capital expenditure decisions makes sense.

Hair stylists must take court decisions on occupational licensing into account when setting up a business, but does that mean you want to put a hair stylist on the Supreme Court? I have an even better idea, why not have hugely important monetary policy decisions made by people who are experts on monetary policy?

It would be interesting to ask a group of business people exactly how they “take monetary policy into account”. I wonder how many would (wrongly) assume that the question referred to “taking interest rates into account”, instead of actual monetary policy?

It’s little wonder that in this populist age central bank independence is under attack. As Bloomberg News reported on Monday, the rise of populism is putting pressure on central banks as “institutions stuffed with unelected technocrats wielding the power to affect the economic fate of millions.” Leavening the boards of policy makers with executives who’ve made hiring and firing decisions and have helped build companies would be a way to address the perception that decisions about borrowing costs are made in ivory towers by economists who’ve all read the same textbooks but don’t inhabit the same world as the people they’re supposed to serve.

So are we now to believe that “populism” in the 21st century means turning the government over to business executives, instead of union leaders, teachers, nurses and electricians? And this is because people like Bill Gates are more in tune with the lives of ordinary Americans than economics PhDs making $200,000/year? What relevant information about “real people” do economists lack? Do we not know that real people don’t like unemployment? Do we not know that real people don’t like high inflation? Do we not know that real people who borrow money like low interest rates and real people who save money like high interest rates? I’m genuinely curious—what is it about real people that we don’t know?

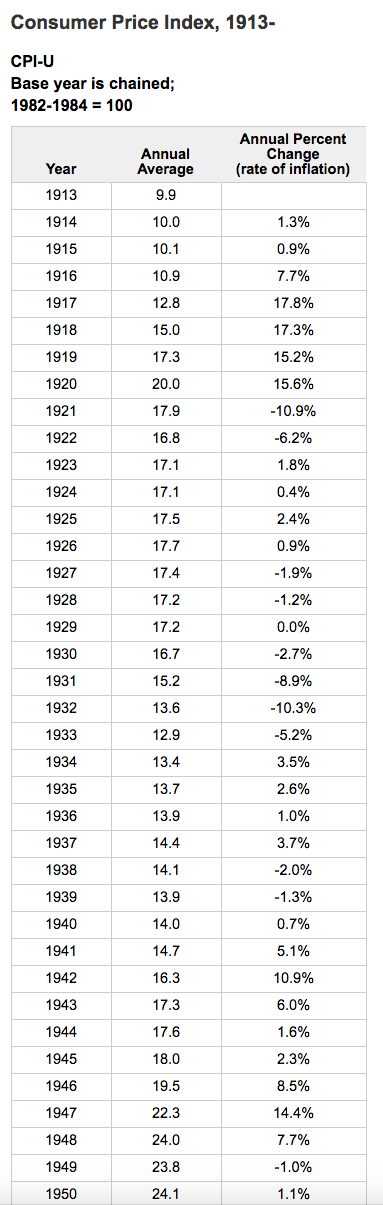

The article also points out that the Fed was dominated by non-economists from 1910 to 1950. (Put aside the fact that the Fed did not exist in 1910.) How’d the Fed do during that period?

The average inflation rate isn’t all that bad, but look at the volatility. There are three years where prices fell at roughly 10%, and 6 years where we had double-digit inflation. All in a 37-year span of time. In the following 66 years we’ve only had 4 examples of double-digit inflation, and the worst deflation was 0.4%. Monetary policy is especially harmful when it is highly unstable, and (other than 1923-29) this was never truer than during 1913-50. (You’d get similar results using NGDP growth rates.)

Readers of this blog know that I’m not a fan of technocratic experts managing the economy. I’d prefer a rules-based monetary regime when the market determined the money supply and interest rates. But as long as we have discretionary monetary policy, let’s have it run by people who are experts. Not necessarily PhD economists (Volcker had a masters in economics), but certainly people who can understand the research papers prepared by the Fed’s staff. Here’s one simple example. Ask Janet Yellen and the typical business executive why the CPI was so unstable between 1913 and 1950 (or during the Great Inflation for that matter.) Compare the answers.

Here’s an analogy. I hope to see the day where commercial airplanes are run by automatic pilots. But as long as we are using human pilots, I’d prefer they be trained jet pilots, not business executives trying out a new hobby.

READER COMMENTS

Michael Byrnes

Feb 27 2017 at 11:31am

I think that if I were forced to choose between appointing plumbers and hairstylists to the Fed vs appointing businessmen, I would opt for the plumbers and hairstylists.

The second block quote above is exactly why I wouldn’t want to turn it over to businessmen.

Steve F

Feb 27 2017 at 2:14pm

The average plumber would quickly see the logic of NGDPLT and a rules based regime.

Steve F

Feb 27 2017 at 2:29pm

Put the average businessman in as Fed chair during autumn of 2008 and he’d say “we can’t just let the price level drop to the floor.” Put the average economics PhD in the Fed and he’d say “but we’ve been ‘extraordinarily accommodative’.”

Andrew_FL

Feb 27 2017 at 3:47pm

Points if you can guess who said this and in what context. Don’t google it.

Thaomas

Feb 27 2017 at 5:22pm

@Steve F

Who was saying that QE was dangerous and would lead to inflation in 2008, your average businessman or your average economist such as Krugman? Balancing the budget during a recession isn’t called the Swabian housewife fallacy for nothing.

Scott Sumner

Feb 27 2017 at 6:21pm

Andrew, Hayek?

MikeP

Feb 27 2017 at 7:39pm

Yeah, it definitely sounds explicitly anti-Keynes.

Scott Sumner

Feb 27 2017 at 8:47pm

Mike, Yes, and didn’t Hayek have a book entitled “Prices and Production”?

MikeP

Feb 27 2017 at 8:51pm

Yes. But the two of them also had a running dialogue in public that such a statement may have come from.

Andrew_FL

Feb 27 2017 at 9:31pm

Yes, it was Hayek critiquing Keynes. The best reason not to appoint businessmen to the Fed is that your average businessman tends to think like a vulgar Keynesian.

Steve F

Feb 27 2017 at 11:34pm

Perhaps we could have used some of that business man “shortsightedness” in the summer of 08 to stop the Fed from letting the bottom fall out of short term inflation expectations.

James

Feb 27 2017 at 11:57pm

“I have an even better idea, why not have hugely important monetary policy decisions made by people who are experts on monetary policy?”

This probably sounds great to anyone who believes that there actually are experts on monetary policy. Just like having industrial policy made by people who are experts on economic planning. If only we had the right people at the controls, the right mathematical model of the economy, etc…

But here is the real problem: Central planning does not work and never will work in money for the same reasons it does not work and never will work in shoes, nails, or potatoes. The people making the “hugely important decisions” do not bear the costs of their own errors. That problem won’t go away by appointing the right experts, targeting NGDP, etc.

To be sure, appointing “business people” won’t be an improvement either but it’s not because they are the wrong people for the job of conducting monetary policy. It’s because conducting monetary policy is the wrong job for anyone.

Andrew_FL

Feb 28 2017 at 1:40am

For the record, the quote in question comes from The Pure Theory of Capital.

mbka

Feb 28 2017 at 2:12am

[Comment removed. Please consult our comment policies and check your email for explanation.–Econlib Ed.]

mbka

Feb 28 2017 at 5:26am

(second try to remove rudeness)

Scott,

as my grandmother always said, the fish starts smelling from the head down. This “businessman” of four bankruptcies now in charge of the country, puts other businessmen in charge of everything, because that’s the only people he knows. And he only appoints cronies, because he doesn’t trust anyone else. Besides, he’s profoundly anti-rationalist. He’s Dunning-Kruger become flesh. So the US will have businessmen in charge of the Fed, businessmen in charge of the FDA, businessmen in charge of NSF, businessmen in charge of the Arts, businessmen in charge of … well, isn’t the US government still missing Army and Navy secretaries too? well here we go. etc.

The bigger problem behind these small problems is that the US is just so big as an economy, and has been so geopolitically dominant for such a long time, that it has been able to afford blunders of this kind to an extraordinary degree. Over-regulation, expensive lawsuit culture, addiction to far-away wars, hysterical overreactions to threats, massive over-militarization, you name it. And no one realizes how deadly any of these would have been to lesser nations. Russia, China, Germany, no one could afford this kind of stuff. They all have much more limited resources and therefore, have to act much smarter. The US could just shake it off, still can. Trouble is, the bucket goes to the well until some day, the bottom actually falls out. One day the US may blunder to such an extent that it does not recover. Maybe we have seen peak-US already.

Mark Bahner

Feb 28 2017 at 12:15pm

It seems clear from Scott’s data for 1913-1950 that someone is learning something. Even if we subtract out the WWI and WWII war years a being extraordinary, there is the severe deflation in 1931-1933, and the deflation again in 1938-1939. And I think the numbers would look much, much worse looking at the Fed as having dual goals regarding inflation and unemployment. Look at this bull’s eye, and think about where deflation of 10.3% combined with unemployment of about 24% would show up.

Fed’s dual mandate

Mark Bahner

Feb 28 2017 at 12:24pm

Yes, Scott did write:

But maybe he could have put this in bold or capital letters. Or bold AND capital letters. 😉

Andrew_FL

Feb 28 2017 at 1:17pm

Oh, of course, Mark, why couldn’t you and Scott have been around for the Socialist Calculation Debate to explain to Mises that you just needed the planning done by a computer following rules!

mbka

Feb 28 2017 at 6:02pm

James,

Any evidence for this? Scott just showed nicely how the Fed could manage badly. And as we have seen in the past few decades, it can also much better manage the macroecomomy.

More generally, monetary policy and business production planning are entirely different things. In planning for the exact production of specific products, the price system works well as a feedback mechanism, and planning doesn’t. In planning for the maintenance of monetary and macroeconomic stability, the price system fails, as evidenced by instability, panics and depressions before central banks. How to maintain this stability isn’t worked out completely yet but it is not trivial nor does it seem to work automatically in the way the price system works on autopilot for production and consumption.

Andrew_FL,

The price system is a little bit like an algorithm dispensed by the market, a nice negative-feedback system that enhances stability. The monetary system on the other hand has elements of positive feedback (runaway dynamics) if left to its own devices (panics, deflation), that’s why a monetary policy is needed. Scott is proposing a monetary policy with rules that introduce a kind of negative feedback: add when there is not enough, subtract when there is too much. That’s a rule, a kind of algorithm, and note the similarity to the price system.

BTW even leaving money supply entirely constant would constitute a computer following rules, in this case the rule would be “Leave money supply constant at all times”. You can’t get away from monetary policy, there always is one even if you think there isn’t.

Mark Bahner

Feb 28 2017 at 6:08pm

Andrew_FL, despite the current Internet fashion, I don’t think sarcasm improves the quality of arguments.

And I don’t think “a computer following rules” is the same as, “I’d prefer a rules-based monetary regime when the market determined the money supply and interest rates.”

Other than finding this post, I’m too lazy to check on what Scott has written previously on EconLog about what he has in mind as the best way to go about doing what he proposes. But I do remember reading what Scott has proposed and thinking, “Yes, that certainly seems better than a bunch of economists figuring out what to do.” (Let alone business executives, cashiers, janitors, etc.)

A few hours later…

I’ve now read some criticisms of Scott’s idea, and they seem to be valid. (Note that the whole subject is welllll outside my areas of expertise.) But still:

1) NGDP targeting, and

2) Futures contracts to *inform* NGDP targeting…

…seem like good ideas.

I’m sure if you have some alternative(s) that you think would be even better, EconLog readers would be interested to read it/them.

Scott Sumner

Feb 28 2017 at 7:06pm

Andrew, Yes, businessmen are often “vulgar Keynesians”. Didn’t President Trump mention something about “priming the pump” the other day?

James, You said:

“But here is the real problem:”

No, that’s not the real problem. The real problem is that we have monetary policy being conducted, and when mistakes are made they are very costly. That suggests you want to have monetary policy being made by the people who are least likely to make serious errors. Not doing monetary policy at all is not (currently) an option.

I don’t favor central planning, but if we have it then I’d prefer it be done by experts.

mbka, Good points. Adam Smith’s comment about there being “a great deal of ruin in a nation” is especially applicable to America, thank God.

Andrew_FL

Mar 1 2017 at 2:13am

mbka-

I can’t make heads or tails of this from start to finish, there’s so much misunderstanding in it. If you want to explain how your planning of the money supply is not subject to critiques of socialist calculation-if you hope to have a response to James-you are going to need a better understanding of the price system than it being an “algorithm.”

Actually you can, if both what money is and how much of it there is are determined solely by market processes, there is no “policy.” Do you believe that money can only exist if there is a government?

Mark-In my opinion the NGDP futures market idea is nothing more or less than the “playing market” Mises criticized Market Socialists for proposing.

As for what I would “propose” for base money a good place to start understanding my point of view would be to read up on Menger’s theory of how money emerges from barter.

Scott-“Didn’t President Trump mention something about “priming the pump” the other day?”

I wouldn’t know I hardly watch or listen to any of his statements these days, I was finding doing so bad for my health. But I recall him using terminology like that in the past.

I’m glad to hear you don’t favor central planning but I assume you are still very much in favor of the existence of a central bank so I don’t think we understand that term in quite the same way.

Mark Bahner

Mar 1 2017 at 12:34pm

Hi Andrew,

A bit of background before I respond to your comments. I’m an environmental (formerly mechanical) engineer. My total economics education involves two Intro to Econ trimesters, and a trimester of Money and Banking. (About the time of peak inflation in the Carter era.)

About my only claim to fame in the economics area is that I bet (rather immodestly…but probably correctly ;-)) that I know more about the likely long-term economic growth of the world than (Nobel laureate!) Robert Lucas Jr.:

Long Bet #194…21st century economic growth

You write,

Well, my lunchtime is short. I’m not interested enough to read more than a few paragraphs. Is there anywhere that you have made comments that specifically and concise state what you think should be done? Or is there a website that specifically and concisely states what should be done that you agree would be better than anything Scott has proposed?

P.S. One of these days, I probably ought to contact Dr. Lucas to let him know about the bet…;-)

Andrew_FL

Mar 1 2017 at 2:29pm

Mark-Unfortunately I don’t think I can condense my ideal, or that anyone has done so, into something with sufficient brevity to be read casually over your lunch break. Certainly not and do the case for it justice.

The short version is that I think participants in the market ought to be able to select the medium of exchange from amongst whatever options the market may provide, and that governments should not be in the business of supplying a medium of exchange at all.

Beyond that, what “ought” to happen depends a great deal on what the participants in the market select as the medium of exchange.

But I am trying to concern myself solely with the selection of the basic form of money.

Mints should be private, if the medium is some metallic commodity.

Banks should be unregulated and free to issue money substitutes redeemable in the form of the base money.

Mark Bahner

Mar 1 2017 at 9:47pm

Andrew,

Wow. OK then. Good luck with that. 🙂

Seriously…the Fed has been operating for more than 100 years. And the government has been providing media of exchange for much longer than that. Do you think it’s even remotely plausible that the U.S. will even get rid of the Fed?

James

Mar 2 2017 at 5:35pm

Mika,

Are you asking for evidence that central planning doesn’t work in general or evidence that money is not a special case?

Scott,

Why should I believe economists are less likely to make errors in monetary policy than anyone else?

Comments are closed.