This article caught my eye:

When online retail giant Amazon.com Inc. announced last Friday that it would purchase Whole Foods Market Inc., a plunge in retail and grocery stocks reinforced the disinflationary tone set by three straight months of disappointing data on consumer prices. It’s an example of the technological forces that are increasing competition and further limiting companies’ ability to pass on higher wage costs to customers.

“That normally indicates that somebody thinks that they are not going to be earning as much as they were,” Federal Reserve Bank of Chicago President Charles Evans said of the market reaction to the deal while speaking with reporters Monday evening after a speech in New York.

“For me, it just seems like technology keeps moving, it’s disruptive, and it’s showing up in places where — probably nobody thought too much three years ago about Amazon merging with Whole Foods,” he said.

Evans, a voter on the Federal Open Market Committee this year who supported its decision to raise interest rates last week, says he is less confident than most of his colleagues that inflation will soon rise to their 2 percent target.

A big reason for his ambivalence: Deflationary competitive pressures could have become more important for the overall trend in prices than the so-called Phillips Curve relationship, which links inflation to the state of the labor market. That model, coined almost 60 years ago, is the basis for the Fed’s outlook for continued gradual rate increases.

I’m a bit confused by this. I certainly agree that there are good reasons to question the Phillips Curve model, for standard “never reason from a price change” reasons. The Phillips Curve only works if changes in inflation are driven by AD shocks, not aggregate supply shocks. In that sense I agree with Evans.

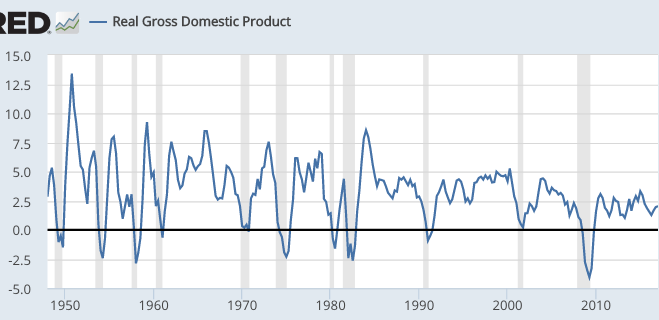

But what is the nature of these mysterious AS shocks? Evans points to technology and competition, but these are forces that would cause the long run AS curve to shift to the right more rapidly. In other words, these are factors that would lead to a higher trend rate of growth in real GDP. The most noteworthy aspect of our modern economy, however, is slowing trend RGDP growth. Instead, it seems that wage moderation has shifted the SRAS curve to the right, producing a steady decline in the unemployment rate. The economy is not growing very fast at all, and what growth is occurring (roughly 2%) appears to be well above the long run trend rate, as the unemployment rate can’t keep falling forever.

I’m not saying that he is wrong about Amazon, or even retailing as a whole. But when you look at the data it’s clear that technology is not having much impact on overall real GDP growth.

And even if you argue that we aren’t measuring growth properly, and the actual RGDP is higher because we miss all the goodies provided for free on the internet, it still doesn’t solve the puzzle. The puzzle is the low rate of reported inflation. If real growth is higher than the official figures suggest, then inflation is even lower.

And this leads us to the point where macroeconomic discussions ought to start—with NGDP growth. The real issue for monetary policymakers is not inflation and/or RGDP growth, it’s NGDP growth. The only way to have low inflation despite low RGDP growth is if the Fed has such a tight monetary policy that NGDP growth remains slow. And that’s exactly what they’ve done since 2009. If you produce 4% NGDP growth year after year after year, then why be surprised that inflation remains low? Why look for explanations having to do with “technology” or “competition” if the answer is right there in front of your eyes—NGDP.

If the Fed starts delivering 11% NGDP growth, as in the 1970s, and we still have sub-2% inflation, then we can start worrying that technology is holding down inflation. But in that case we’d have no reason to worry about the low inflation “problem”, as RGDP growth would be 9%. Which is just another stating a point I repeatedly emphasize; inflation doesn’t matter, it’s NGDP growth that matters.

HT: John Hall

READER COMMENTS

Thaomas

Jun 21 2017 at 11:04am

The thing that struck me was the phrase “three straight months of disappointing data on consumer prices.” And the quote clearly did not mean that the writer was disappointed that the Fed has yet again failed to hit its 2% inflation target, allowing the price level to drift still farther from a 2% trend rate of growth. He meant that the date disappointed the hawks who are always looking for an excuse to “normalize” interest rates.

Rob

Jun 21 2017 at 11:43am

Looks to me that, excepting a few spikes and dips, inflation has spent the last 20 years pretty consistently between 5 and 7.5 percent.

https://fred.stlouisfed.org/graph/fredgraph.png?g=eaCl

Todd Kreider

Jun 21 2017 at 11:44am

Scott, you replied on a previous thread that you didn’t see the GDP per capita growing more than 0.5% for the rest of this century. I searched your reasoning for this prediction but couldn’t find anything. Is it about the same as Robert Gordon made for zero growth, that technological innovations from 2015 to 2100 will be tiny compared to his golden era of 1870 to 1970?

Watching Gordon is painful to watch because he doesn’t understand even the basics of technological trends – true for Paul Krugman and Tyler Cowen as well, who seem to think nothing is improving much with soft A.I. and health/medicine. (Cowen stated in 2011 that he doesn’t think there will be any breakthroughs in medicine out to the year 2030 (!) )

Last year, Gordon gave a 90 minute presentation at the London School of Economics where he discussed Moore’s Law and concludes “the whole thing collapsed after 2005.” Can you see the collapse of Moore’s Law on this graph below? “No.”, right?

https://en.wikipedia.org/wiki/Moore%27s_law#/media/File:Transistor_Count_and_Moore%27s_Law_-_2011.svg

So, can you point to a blog post where you explained why you think GDP/capita will be no higher than 0.5% a year out to 2087? Thanks!

Jake

Jun 21 2017 at 12:27pm

Prof Sumner,

Another excellent post. It’s frustrating that the Fed just can’t seem to let go of its failed model and policy instruments, despite the fact that your arguments are so much more logical and intuitive.

Question: It seems like “inflation phobia” is still a major driving force in Fed policy and macroeconomics as a whole. Do you think this has anything to do with the age of policymakers, most of whom experienced their formative years during the Great Inflation? Kind of a “generals always fight the last war” sort of thing.

Scott Sumner

Jun 21 2017 at 12:31pm

Todd, There are many reasons I could give:

1. The factors that have caused the recent slowdown don’t seem likely to go away anytime soon.

2. The economy is increasingly dominated by labor intensive services, where technological gains are difficult.

Having said that, there is obviously a lot of uncertainty here, and I don’t have a great deal of confidence in my predictions for the distant future. I was asked for my best guess, and slow growth was the answer.

By the way, I still consider 0.5% a “good” outcome, given that we are already quite a rich country.

Scott Sumner

Jun 21 2017 at 12:32pm

Jake, Yes.

John Hall

Jun 21 2017 at 1:08pm

“as the unemployment rate can’t keep falling forever.”

But there is still plenty of room for the prime age employment to population ratio to recover…

LK Beland

Jun 21 2017 at 1:59pm

“as the unemployment rate can’t keep falling forever.”

I’ll pile on John Hall’s remark.

The prime-age employment-to-population ratio in the US could increase at its current rate for a decade or so. If it did, the ratio ten years from now would be 84%, which is well within the normal range for developed countries.

Scott Sumner

Jun 21 2017 at 10:42pm

John and LK, I doubt it will keep increasing for very long. But even if I am wrong, that doesn’t account for the falling unemployment rate.

I think it very likely that RGDP growth will slow relatively soon.

Thaomas

Jun 22 2017 at 5:59am

Scott,

Is your guess about future RDDP growth contingent on the the Fed continuing to have, in effect an interest rate ceiling policy which implies both growing uncertainty about future price levels and uncertainty about NGDP growth? Is it also contingent on fiscal policy continuing to fail to follow an NPV rule for public investments? How much better could RGDP do with better monetary and fiscal polices?

Antischiff

Jun 22 2017 at 8:49am

Dr. Sumner,

I’m curious as to whether you’re familiar with “aggregate efficiency” as applied to macro growth theory and what you think about it. Thanks.

Scott Sumner

Jun 22 2017 at 10:38am

Thaomas, No, it’s not contingent on those policies. They have little impact on trend growth.

Antischiff, No, I’m not familiar with that term. What does it mean?

Antischiff

Jun 22 2017 at 12:27pm

Dr. Sumner,

Sorry about that double post of mine.

Here is a link to an explanation of aggregate efficiency, as applied to macroeconomics:

http://wiki.p2pfoundation.net/Thermo-Dynamic_Efficiencies_of_the_Third_Industrial_Revolution

It is generally a claim that, given the current state of infrastructure in the US, we’re running up against a thermodynamic efficiency limit that’s limiting economic growth.

It seems a fair number of researchers have tried to apply thermodynamic concepts to macroeconomics, but it seems few, if any these approaches have been widely accepted.

[duplicated comment removed–Econlib Ed.]

Thaomas

Jun 22 2017 at 4:16pm

Scott,

So after recessions, that are inevitable without good monetary policy, RDGP grows fast enough to return to trend? It sure did not happen after 2008! How can you be sure it will in the future?

Jose

Jul 3 2017 at 9:36am

Prof. Sumner, do your conclusions still hold if we adjust NGDP to per capita working population, as you have advocated many times before?

Comments are closed.