My vision of macro has several components:

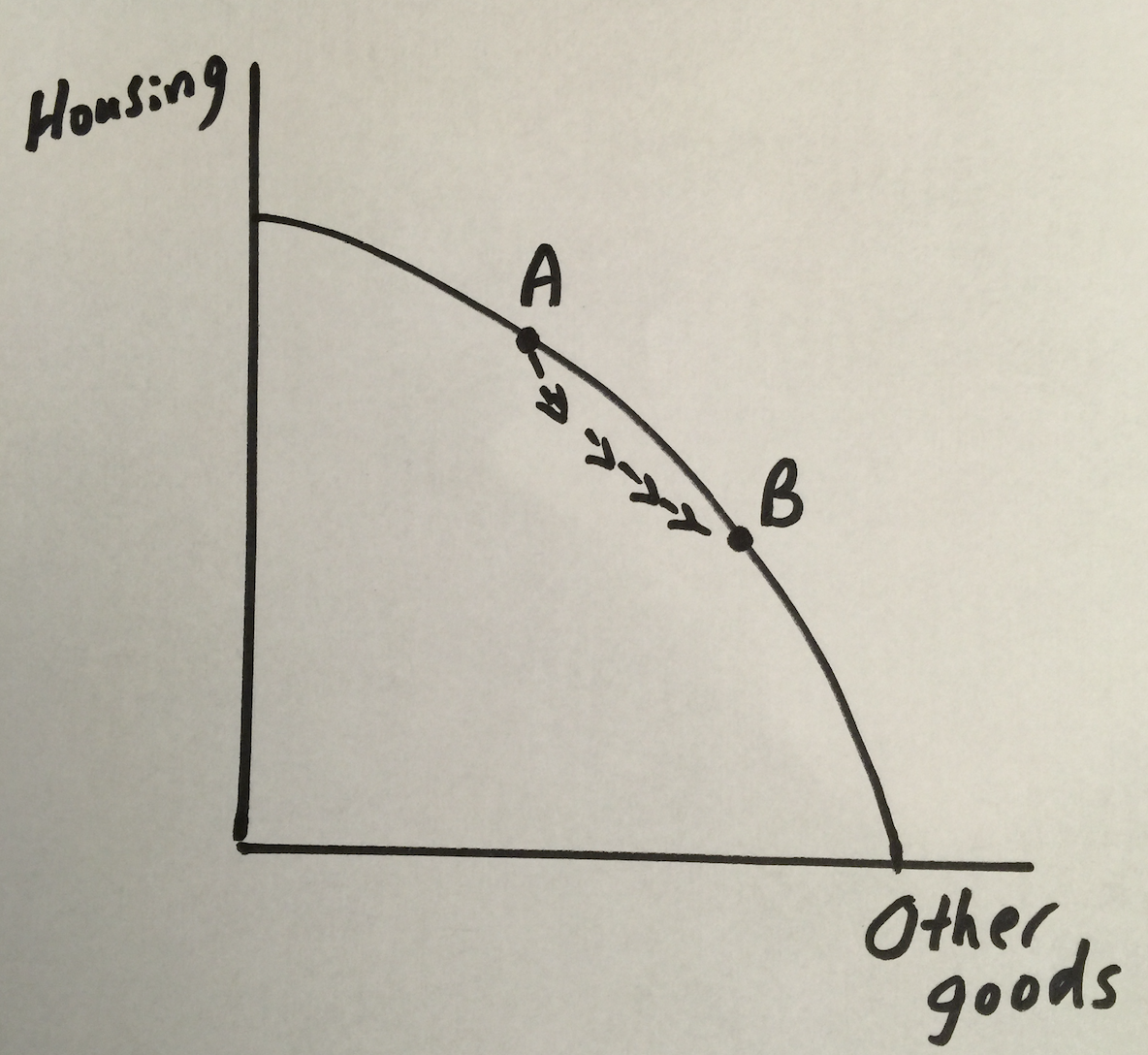

1. A production possibilities frontier, which gradually shifts out due to productivity and labor force growth. That’s the “old classical” part.

2. An AS/AD model that causes output to cycle above and below the PPF, due to monetary shocks (NGDP) plus sticky wages.

3. A “reallocation” problem when the economy needs to move quickly along the PPF. In that case, the economy will briefly dip inside the PPF, as resources in one sector cannot be costlessly reallocated to another sector:

The period from mid-2008 to mid-2009 is an excellent example of the second case, where tight money pushed the economy well inside the PPF, causing RGDP to fall by 3%. But what’s an example of the third case—reallocation?

It turns out that the period from the first quarter of 2006 to the second quarter of 2008 is a near perfect example of reallocation, showing all the trademark effects. Here are some data:

1. Housing starts fell by more than 50%, from a bit over 2.1 million (annual rate) to a bit over 1.0 million.

2. If the reallocation model is correct, then the decline in housing related industries should have been partially offset by a rise in non-housing related industries. And that’s what happened. RGDP growth average 1.27%/year over that 9 quarters, which was positive but somewhat below trend. Non-housing industries expanded.

3. Reallocation can be viewed as an adverse supply shock, so inflation should have been relatively high. And indeed the GDP deflator rose at a 2.45%/year rate, above the Fed’s target of 2%.

4. Total employment would probably have risen, but at a slower than normal rate. Unemployment would rise slightly. And indeed that’s what happened, as total employment rose and the unemployment rate crept up from 4.7% to 5.3%.

In fact, the economy was hit by a second reallocation shock at the tail end of this period, as oil prices skyrocketed in early 2008. So in addition to reallocating out of housing construction (and related activities), the economy had to reallocate away from energy intensive industries such as SUV and pick-up truck manufacturing. This 6 month period is when much of the rise in unemployment occurred. And yet despite all of that, RGDP held pretty stable.

Thus one of the biggest reallocations in modern history had only a modest impact on the business cycle, as other sectors picked up the slack. In contrast, the subsequent fall in NGDP (i.e. tight money) drove output lower in a broad cross-section of industries during 2008-09, pushing RGDP sharply lower and unemployment up to 10%.

In my view, the events of 2006-09 fit the model almost perfectly. Not sure why the Great Recession was viewed as a crisis for macroeconomics–maybe other economists have the wrong model.

READER COMMENTS

Rajat

Nov 26 2017 at 12:08am

Given that reallocation is always going on to some extent, do you think recessions pre-empt or hasten reallocation? I suppose it would be hard to test, but anecdotally it seems to be the case. That’s not to say recessions are on balance a good thing, but it’s the sort of idea that seems to lie behind the views of some hair shirt Austrians.

E. Harding

Nov 26 2017 at 1:38am

Bingo on all counts. The biggest cases of recession due to re-allocation in world history were in the ex-socialist countries in the first half of the 1990s. At the time of its collapse, the USSR was the third largest economy in the world.

Texas was a state hit hard only by the NGDP shock, FL was disproportionately hit by the housing shock, and MI was battered disproportionately harshly relative to the rest of the country by all three shocks Sumner mentions, plus a manufacturing-related reallocation shock in the early-mid 2000s.

Thaomas

Nov 26 2017 at 7:53am

Why does changing expectations, perhaps reacting to changes in RGDP or RGDP growth (whether induced by monetary policy, reallocation, or otherwise) play a role in AD?

Why do you identify the period of “tight” monetary policy as extending only until 2009? From the POV of either NGDP targeting, PL targeting, or average inflation rate targeting (the latter two as the “stable prices part of the Fed’s mandate), the period extended much longer, arguably to the present day.

During a period of inappropriately “tight” money (according to whatever model that defines the “appropriate” target) and corresponding unemployment of resources, should this not induce wealth maximizing governments to borrow and invest more, e.g, engage in “fiscal policy?”

What kind of political factors led the Fed to adopt the inappropriate monetary policy, however you define it?

@ Rajit. As I understand the “Austrian” concern with “redistribution,” they are pointing to the inefficiency caused by inappropriate redistribution toward production of capital goods when the real interest rate is being inappropriately held down by too “loose” monetary policy.

Matthias Goergens

Nov 26 2017 at 8:35am

Rajat, the null hypothesis is of course that recessions have no statistically significant influence on reallocation. (Especially those caused by tight money.)

Scott’s post here suggests that the hair shirt Austrians are sort-of right, but the kind of resl suffering they talk about that comes with adjustment of investment and reallocation is the barely noticeable (on a macro scale) pain seen from 2006 to 2008.

The Internet Austrian mistake is to misdiagnose the kind of pain from 2008-2009 as the other kind.

Ironically enough, if Scott had his way and we’d get ngdp level targeting (or alternatively free banking, if Selgin is to be believed), the Austrians would become right about how the economy works. (Or as one blogger put it, ngdp targeting makes the economy approximately classical.)

Oliver Sherouse

Nov 26 2017 at 10:29am

When describing this at more length, it might be helpful to qualify the production possibilities frontier in such a way that it makes sense to be “above it,” as you describe in point 2. I choked on that a bit at first.

Scott Sumner

Nov 26 2017 at 11:29am

Rajat, I don’t see why they’d have much effect. In one sense it makes reallocation harder–workers have more trouble finding new jobs. In another sense it makes it easier—more unemployed workers are available for new and growing industries such as fracking. I doubt the net effect is all that great.

Harding, Yes, plus bad governance in Michigan.

Thaomas, You asked:

“During a period of inappropriately “tight” money (according to whatever model that defines the “appropriate” target) and corresponding unemployment of resources, should this not induce wealth maximizing governments to borrow and invest more, e.g, engage in “fiscal policy?””

No.

You asked:

“What kind of political factors led the Fed to adopt the inappropriate monetary policy, however you define it?”

They made a simple mistake.

Regarding tight money, I meant that 2008-09 was a period of extremely tight money. Policy remained too tight for a number of years after 2009.

Oliver, Consider the PPF as the maximum feasible output when labor markets are in equilibrium. Being above it means the unemployment rate is below the natural rate.

Iskander

Nov 26 2017 at 5:19pm

I would think that recessions make reallocation worse – more noise in price signals causing peoples decisions to be worse. Think Lucas islands.

Great post, it would be great if other macroeconomists showed their vision of macro.

Lorenzo from Oz

Nov 26 2017 at 6:01pm

Great post. It reinforces my wondering if problems of automation and IT are/will be really as endemic as some folk think or are more a result of regulatory friction getting in the way of adjusting.

ChrisA

Nov 27 2017 at 1:13am

Slightly off topic, but Scott, given sticky prices and wages, do you think higher inflation economies re-allocate more efficiently? The model here is that there is more rapid price signals as to what industries and jobs are needed.

Thaomas

Nov 27 2017 at 8:39am

@Scott

Maybe I did not ask my question correctly. Here is what I meant.

I assume that in an AD recession caused by “too tight” monetary policy government borrowing rates will still have fallen relative to non-recession times. Also, many of the things inputs into government projects — people’s time, machines, real estate are unemployed, i.e. they have market prices greater than their near zero marginal costs.

It seems that both of these factors would induce a government that is not credit constrained (and the US Federal Government could pass that relaxed borrowing constraint on to SLG) to invest more. The marginal project that did not pass an NPV test in “non recession” when evaluated at the lower discount rate and marginal costs of inputs would now pass. A reduction in business income taxes — also leading to more government borrowing — would also induce businesses to invest more in positive NPV activities by offsetting some of the difference between input costs and market prices of inputs. Both of these kinds of investment would raise real income relative to the non-additional borrowing case and so seem like a rational response to the recession. This neo-classical investment response would look “Keynesian,” but what would be wrong with that policy?

It seems to me that there ought to be a “fiscal” response to recessions unless monetary policy was always optimal. It was clear by Jan 2009 that the Fed was not going to keep NGDP or even the price level on trend, so a well designed fiscal “stimulus” would raise real income.

What is wrong with this analysis that produced your “No?”

Scott Sumner

Nov 27 2017 at 2:10pm

ChrisA, That can cut both ways, as higher inflation also makes price signals more confusing. I don’t see it as being a big factor either way.

Thaomas, A recession can also lower the benefit of infrastructure projects—with fewer new homes being built, the benefit of new roads, etc., is lower.

Alex S.

Nov 29 2017 at 4:56pm

I’m not sure that you need to have an interior movement along the PPF. A concave PPF already accounts for reallocation costs, which I assume is synonymous with adjustment costs–which accounts for the rate of change and magnitude of the change between goods produced (I’m referencing Kydland and Prescott’s Time to Build paper (pp. 1346-7)).

I can illustrate your point on the adjustment between 2006-early 2008 (monetary issues aside) without an interior movement along the PPF: In 2006, let’s assume, that the housing/other goods combination, was such that the sum of the two led RGDP to be its largest possible value. By early 2008, even without movement within the PPF, just along it, any subsequent combinations of housing and other goods will translate to a lower RGDP .

From another angle: assume no adjustment costs, which implies a linear PPF. If you move from producing only housing to solely producing all other goods, RGDP would still be the same, even for any other combination. The concavity (arising from assuming adjustment costs) would imply that movements from means to extremes, would result in a lower level of RGDP at any point on the PPF.

However, I think your first point about monetary policy leading to combinations that are temporarily above or below the PPF is spot on. In fact, this is a key feature of the Austrian capital-based macroeconomics model developed by Roger Garrison.

I think the model you’ve sketched out makes one more liable to accept a position, that easy money in the early 2000s helped generate a housing bubble without giving up producing as many other goods (thus implying an above PPF outcome). Then, when tight money comes along and/or capital finds itself misallocated (Austrians aren’t particularly clear on what goes on at the turning point–I wasted my dissertation trying to make this point lol), this pulls you within the PPF.

In general, your research has convinced me that tight money is more consequential than the misallocated capital–but it leaves me sympathetic to David Beckworth’s more in the middle-of-the-road take on what occurred in the 2001-2007 period.

https://www.jstor.org/stable/1913386?seq=1#page_scan_tab_contents

Comments are closed.