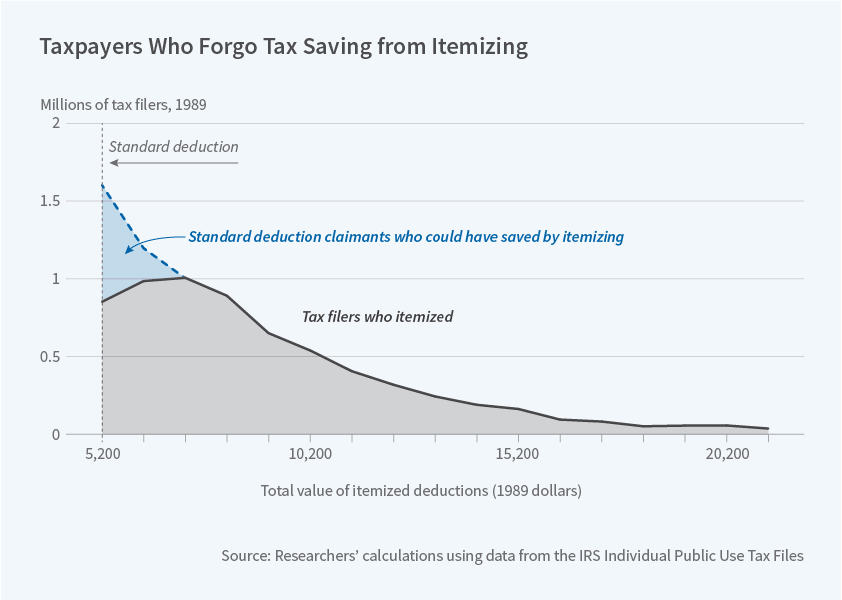

Benzarti estimates the perceived compliance costs to tax filers by computing whether there were “too few” taxpayers with itemized deductions slightly greater than the standard deduction threshold. Taxpayers who might save a few dollars by itemizing might decide that itemizing was not worth the effort; those who could save much larger amounts would presumably incur the cost of keeping records and itemizing their deductions. Using Internal Revenue Service data from 1980 through 2005, the researcher found just such a pattern of “missing taxpayers” above the standard deduction threshold.

He next examined tax years in which there had been significant reforms in U.S. tax codes, specifically increases in the size of standard deductions. He focused on 1988, when the standard deductions were increased from $2,540 to $3,000 for single filers and $3,760 to $5,000 for joint filers, and compared that year’s data to the years before and after 1988. He found that the level of deductions at which there were too few itemizers also shifted between 1987 and 1988, supporting the view that these “missing taxpayers” are the result of choices, not chance variation in the distribution of deductible expenses.

By estimating the amount of tax savings that each taxpayer forwent, Benzarti computed what they must have perceived as the filing cost of itemized deductions. He concluded that these costs are large, and that they are higher for high-income households. This is consistent with the opportunity cost of time being higher for these households than for others. Aggregate compliance costs appear to have risen over time, from $150 billion in 1984 to $200 billion in 2006 (both figures in 2016 USD). This suggests that compliance costs are about 1.2 percent of GDP in recent years.

This is from Jay Fitzgerald, “Some Taxpayers Forgo Benefits of Itemizing because of Filing Costs,” NBER Digest, January 2018. It’s based on Youssef Benzarti, “How Taxing Is Tax Filing? Using Revealed Preferences to Estimate Compliance Costs,” (NBER Working Paper No. 23903), October 2017. The paper is gated and I couldn’t find an ungated version on line.

Notice one large implication. Because the recent change in the tax law substantially raises the standard deduction, compliance costs should fall substantially. Imagine that they fell by 0.2 percent of GDP, that is, by 1/6 of the current cost. There’s, in effect, a 0.2 percentage point boost. It won’t show up in GDP: but it is what many of us would like GDP ideally to measure, that is, economic well-being.

READER COMMENTS

Steven

Feb 7 2018 at 12:47pm

An ungated earlier version can be found here:

http://www.austaxpolicy.com/wp-content/uploads/2016/09/Benzarti.pdf

David R Henderson

Feb 7 2018 at 1:02pm

Thanks, Steven.

Alan Goldhammer

Feb 7 2018 at 2:44pm

This is more of an indictment against our current tax system than anything else. The USG already collects most of the data needed to complete ones 1040 tax filing. The major exceptions are for charitable giving and self-employed individuals. I’ve been doing our family’s taxes for 30+ years and certainly the advent of computerized tax software has made things simpler. Unfortunately, one still has to manually enter most of the data which is the big time hog.

robc

Feb 7 2018 at 3:37pm

I have “always” itemized (at least for last 20 years), but the new standard deduction is going to put me right on the border.

I have already had discussions with my wife about whether it is worth our time to track all of the info going forward.

Justin D

Feb 7 2018 at 5:13pm

Isn’t also fair to assume that a significant number of taxpayers just made a mistake? How many of the taxpayers who lost money by not itemizing would have itemized if you had told them they left money on the table?

Perhaps my itemizing isn’t too difficult (and it helps to be living in an era of online tax preparation), but I don’t think I’d avoid itemizing unless the amount saved was under a few hundred bucks.

That all said, I don’t like social engineering/spending through the tax code. Figure out a threshold of poverty that should be exempt from federal income taxes, and put a flat tax on all income above that amount. Or the (consumption based) flat tax. Or even the X tax.

Hans

Feb 8 2018 at 12:09am

An illuminating subject.

I have never read a piece regarding

the cost of tax paperwork in the form

of GNP.

We have done our own tax filing to

save money, unfortunately, it has resulted

in errors; as a result of misunderstanding

IRA withdrawals.

More evidence how badly the DC sewer is

broken.

Alan Goldhammer

Feb 8 2018 at 7:45am

Hans writes,

The IRS guidelines are nothing but opaque on this topic. However, most major IRA custodians will do the calculations for you automatically. One major pitfall to be avoided is you are going to be on the hook for estimated taxes if it’s a traditional IRA and it’s always best to have a certain % witheld for Federal taxes. Usually, the threshold is 10% but that might not be enough if your IRA has a lot of money in it (common if there have been rollovers from 401(k) plans).

Hans

Feb 8 2018 at 2:01pm

Mr Goldhammer, it was self-directed. I would agree and expand the opaqueness to most of the IRS operations.

Comments are closed.