The most powerful weapon in an economist’s arsenal is the law of demand. When the price (or opportunity cost) of something increases, people will purchase, consume, or choose it less often. The law of demand is a common backbone for many arguments. If the spine breaks the body falls. Naturally, those who want to undermine economic arguments will attack the law of demand directly. Typically the law of demand is derived from simple indifference curve analysis that relies on the idea that individuals maximize with respect to constraints. The simple retort that individuals don’t actually maximize would, if true, cut the heel of the indifference curve defense of the law of demand. Regardless of whether or not the retort is true, whenever it’s brought up the resultant conversation is often hopelessly pedantic and includes a lot of talking past each other.

Gary Becker defended the law of demand and avoided the pedantic conversation by dropping the maximization assumption. In fact, he drops the whole utility function. The law of demand can be derived from the nature of:

![]()

Assume that our individual chooses a bundle (x,y) at random within the above constraint (conjure a familiar triangle in your mind). As pxx and pyy vary, the slope and intercept of the triangle will shift. As the triangle changes shape the probability that some given I or I bundle is chosen will also change. If it increases, a larger proportion of bundles that have higher x with given y are eliminated. A mathematically stronger version of this argument exists if we assume that they consume their entire income (a small amount of rationality in choice is required). In a very clever way, Gary Becker has rescued the law of demand, or at least a version of it sufficient to retaining most arguments made by most economists.

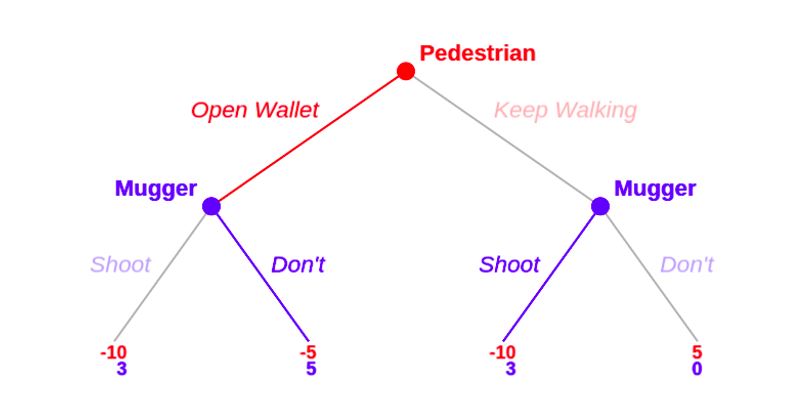

There still remains a problem: Becker’s defense only functions in environments where the parameter shift directly changes the choice set. It is not generalizable to all situations where we argue that some behavior declines when an associated cost increases. Consider the following game: A mugger accosts a pedestrian who has five dollars in his wallet. The pedestrian has the choice to open his wallet willingly or to keep walking. Subsequently, after the mugger observes the pedestrian’s choice, he may either shoot or not shoot the pedestrian. If he shoots, he always gets the cash, but he would prefer to not shoot as it includes the risk of him being put away for a much longer time. Typically the Subgame Perfect Nash equilibrium is as shown below:

The pedestrian always opens his wallet based on the idea of backwards induction. He anticipates that the mugger will never shoot if he’s already received the money, and that the mugger is willing to shoot to get the money, despite the extra risk. Thus, he always opens his wallet, and the mugger never shoots. If we take the mugger’s behavior as given in each contingency, the anticipation of mugging acts similarly to a constraint on the pedestrian. Formally, however, the pedestrian is not constrained by the mugger. He is only constrained by his strategy set {Open Wallet, Keep Walking}. If we wanted to make Becker’s defense here we might say that the pedestrian chooses a mixed strategy between his two options. The presence or absence of a mugger would not deter his behavior whatsoever.

To the extent that the actions of the mugger can be properly analogized to a budget constraint, they must be considered a cognized budget constraint. Becker’s defense only works for forms of constraint that directly impact the choice set. The law of demand applied generally is that when the opportunity cost of something rises, people do less of it (and vice-versa). Kirzner (1962) argued in response to Becker that for a market equilibrium to hold all agents could not be price-takers, at least some must be acting purposefully. Economists who focus on non-market decision-making might find Kirzner’s point moot outside the market context, where all they are concerned with is shifting opportunity costs often couched in the market term “relative prices.” If we hope to expand the use of economic theory in arenas beyond markets (as Becker did), we must bring in more tools than just the budget constraint.

Thanks to Henry Thompson for sarcastic yet useful comments.

References:

- Becker, G. S. (1962). IRRATIONAL BEHAVIOR AND ECONOMIC THEORY. The Journal of Political Economy, 70(1).

- Kirzner, I. M. (1962). RATIONAL ACTION AND ECONOMIC THEORY. Journal of Political Economy, LXX, 380–385.

Marcus Shera is a Hayek Fellow with the Mercatus Center at George Mason University in his fourth year where he studies Economic History and Smithian Political Economy. He also writes at theeconplayground.com.

READER COMMENTS

Andrew Humphries

Jun 12 2023 at 9:12pm

One should I add that even when people are “price takers” they must cognize opportunities “to buy” and “to sell” in terms of meaning. People go to stores in person or navigate to the “add to cart” button. They take credit cards or cash out of their pockets. They don’t bounce around and vibrate like atoms. So purposeful behavior and verstehen are needed even when in Becker’s story in which the question of “what” people buy is assumed to be “random” or inertial.

nobody.really

Jun 18 2023 at 6:26am

Editorial note: I think there’s a glitch in the graph. If the pedestrian keeps walking and the mugger doesn’t shoot, then the mugger gains nothing (0)–but the pedestrian also gains nothing (0). The pedestrian does not gain $5 by refusing to open his wallet. (I’ve declined to open my wallet many times; it has not resulted in more money appearing there once I do open it.)

Comments are closed.