Earlier this year, when the Trump administration floated Stephen Moore’s name as an appointee to the Federal Reserve Board, a one-liner came to mind: “Someone must have told him there’d be no math.” Moore is infamous for math errors.

Other reactions were less light-hearted. My Cato colleague George Selgin tweeted, “I don’t believe that [he] is qualified to serve on the Fed” and wrote an extensive criticism of one of Moore’s prominent claims about Fed policy. Bruce Bartlett tweeted that Moore “knows absolutely nothing about the Federal Reserve or monetary policy.” Harvard economics professor Greg Mankiw blogged that Moore “does not have the intellectual gravitas for this important job.”

Moore ultimately did not get a formal nomination, and rightly so: Selgin, Bartlett, and Mankiw were right that he is unqualified to sit on the Fed board. His policy work has been on tax and budget policy; making him one of the nation’s top monetary policymakers would be akin to having a psychiatrist perform the work of a heart surgeon (or vice-versa).

That said, when his name was floated, Moore’s critics attacked him in part for some economic ideas that he’s endorsed over the years. I thought some of those attacks were unfair to the ideas (though perhaps not to Moore’s specific use of them). With 2019 almost over, let’s circle back and think through a few of those ideas and their criticisms.

Capitalism and Democracy

One idea was Moore’s claim that “capitalism is a lot more important than democracy,” which he said in Michael Moore’s 2009 documentary Capitalism: A Love Story and echoed elsewhere. Here’s more of what Stephen Moore said in the documentary:

Michael Moore thought this was outlandish, as did plenty of Stephen Moore’s critics a decade later. For instance, Rolling Stone’s Peter Wade wrote: “So as long as people are ‘free’ to make as much money as they can, let’s throw away civil rights and democracy in favor of the almighty dollar. Sounds like a true, Trumpian nominee.” Added Counterpunch’s Paul Street, “Give Stephen Moore some credit: he doesn’t mind going public with an elementary if sadly scandalous fact of social and political life past and present: capitalism and democracy work at cross purposes with each other.”

Thing is, capitalism does not “throw away” civil rights and democracy (nor does democracy necessarily protect civil rights for anyone but the majority), and capitalism and democracy do not “work at cross purposes with each other.”

Democracy, of course, is a political system in which the majority of voters decides public questions—or decides on representatives to decide those questions. Capitalism is an economic system in which people privately invest and take risks to provide goods for exchange. Democracy properly concerns public goods: goods that are most efficiently procured by government for its constituents—think national defense, public safety, and environmental protection. Capitalism mainly concerns private goods: goods that are most efficiently procured by private exchange—think food, shelter, and clothing. Government typically sets the quantity and quality of each public good that it provides to everyone, while capitalism usually offers a broad array of private goods and individual buyers then choose the quantities and qualities they consume.

Deciding whether democracy or capitalism is “more important” is, in essence, deciding whether public or private goods are “more important.” If a person especially values the military, emergency services, environmental protection, and other public goods, and if that person generally approves of the quality and quantity decisions made by half of the electorate plus one voter (or those voters’ representatives), then that person would likely consider democracy more important. But if a person especially values food, shelter, clothing, and other private goods, as well as the freedom to choose the quantities and qualities he consumes, he would likely consider capitalism more important.

Both types of goods are important, so it is understandable why some people would favor capitalism and others would favor democracy. The debate between the virtues of public goods and private goods, and between public and private choices over the qualities and quantities of those goods that are exchanged, is interesting and important. For that reason, it’s disappointing—and hard to understand—why Street and Wade think it’s so obvious that public goods are more important that they attacked Stephen Moore for saying otherwise.

The Gold Standard

Moore has, at various times, endorsed the idea of the United States returning to the gold standard; that is, legally equating the value of the dollar to a specific quantity of gold. Of course, gold-backed and other hard currencies were common throughout much of human history, only being broadly replaced by fiat currencies in the 20th century. According to Moore’s critics, returning to the gold standard is a laughable idea; they say no serious economist would advocate such a thing.

George Mason University’s Lawrence H. White is a serious economist, and he has devoted much of his career to researching the history and theory of hard currencies. In a wonderfully iconoclastic 2013 paper, he concludes in part:

As White notes, the virtue of hard currencies is that it’s hard for governments to alter their value, outside of express revaluation. That protects the value of money and helps guard against recession. On the other hand, sometimes government has legitimate, publicly beneficial reasons to revalue money. In U.S. history, monetary policy has been—by far—the more effective tool government has to combat recession. But then, government meddling with the currency was also responsible for two of the worst economic crises of the last 100 years.

Put simply, the benefit of fiat currency is that it allows government to engage in monetary policy, while the benefit of hard currency is that it keeps government from engaging in monetary policy. There is something to be said for both.

Regardless of what one thinks of monetary policy making, the modern Federal Reserve is explicitly tasked with carrying out monetary policy. Appointing a proponent of the gold standard to the Fed board is not unlike appointing a die-hard Chicago Bears fan to coach the Green Bay Packers. However, Moore’s ill-suited candidacy does not diminish the virtues of hard currency. As with democracy and capitalism, the debate over monetary policy making is interesting and important, and it’s disappointing that Moore’s critics seem not to appreciate that.

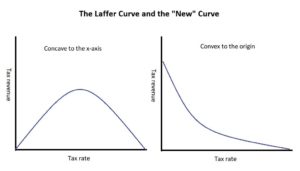

Laffer Curve

Other criticisms of Moore involved his championing of the idea of efficient tax rates. Though this idea has a long history, it is commonly associated with the economist Art Laffer, who is a business partner and frequent co-author of Moore’s.

The (probably apocryphal) story about Laffer and this idea is well known: While meeting with some Gerald Ford administration officials in 1974, he supposedly sketched a concave curve on a restaurant napkin, explaining that it depicted the relationship between tax rates and government revenue. Set the rate too low and government would receive little revenue; set it too high and government would likewise receive little revenue because taxpayers would either forgo the taxed activity or find ways—licit or illicit—to avoid the tax. Somewhere between the two extremes would be a rate that would maximize revenue. Laffer pointed out that, under this idea, tax rates could be lowered and yet government revenue would increase. It’s worth remembering that, at the time he made this argument, the top marginal income tax rate for individuals was 70%, and had been as high as 91% in the previous decade.

However, this notion seems to have transformed in recent decades into the idea that lowering any tax rate would result in a government revenue increase from increased economic activity. That is, instead of a concave curve, the relationship would be convex, with government revenue always rising as tax rates fall.

I suspect that Moore would disavow this new curve and maintain his faithfulness to the original. However, his advocacy of lower tax rates seems to never acknowledge that there is a tipping point where lower rates mean less revenue.

(This is not to say that government should pursue efficient tax rates. There are good arguments for rates below the efficient rate, e.g., respect for taxpayers, questions about the returns to government spending. However, if policymakers are concerned with maximizing government revenue, tax rates above the efficient rate are counterproductive.)

These two curves probably best exemplify my thoughts on Moore and these ideas. While I agree that he would have been a poor Fed governor, some of the ideas he espouses have merit that his critics seem not to appreciate. We should not make that same mistake.

Thomas A. Firey is a Cato Institute senior fellow and managing editor of Cato’s policy journal Regulation

READER COMMENTS

Loquitur Veritatem

Dec 30 2019 at 1:13pm

Fair and balanced, as they say. It’s good to see my Cato successor’s name popping up here occasionally. Regularly would be even better.

Jon Murphy

Dec 31 2019 at 10:36am

With respect, I don’t particularly like your defense of the capitalism/democracy question. I think within the framework you build (capitalism is about private goods, democracy [or politics in general] is about public goods), your point is correct, but I don’t like that framing.

Public goods can, and often are, provided (and in desirable quantities) by the private sector. For example, see Coase’s paper The Lighthouse in Economics, or more recently Rosolino Candela and Vincent Geloso’s 2018 Public Choice article The Lightship in Economics. Further, given that what constitutes a public good is both subjective and technical, the framing you provide doesn’t exactly tell us much about the distinction between capitalism and democracy.

Rather, allow me to broaden the question to include all forms of government, not just democracy. Since market transactions are broadly consensual and political transactions are broadly coercive, I think a better way of framing the question is between which actions should be consent-based and which should be compelled through coercion. Framing the question this way, I think, helps shape the conversation around matters of justice and foments a presumption of liberty, rather than just some technical box to check (“Is this a public good? Yes? Then government should provide it.”)*

*To be clear, I do not think you’re making this argument, but rather that your framing could be used in this manner, just like how people use “externalities” to justify all kinds of programs just because of the checkbox welfare economics establishes.

Thomas Firey

Dec 31 2019 at 9:12pm

Jon: Well put.

Comments are closed.