…and never were.

It has become conventional wisdom among economists that demographics are Japan’s underlying problem. Demographics are blamed for everything from slow growth to zero interest rates to deflation. But demographics are not and never were Japan’s problem. Japan may represent “the future”, but are we drawing the right lessons?

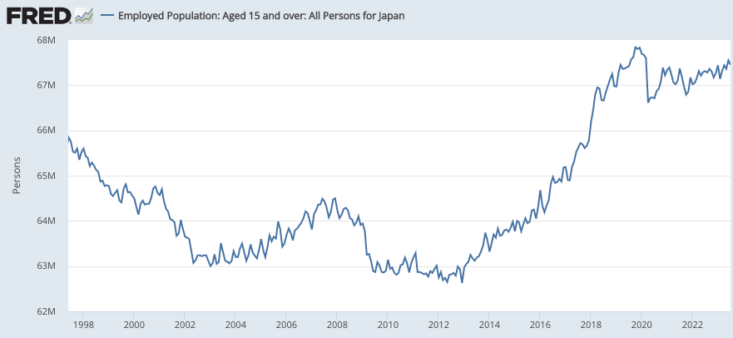

The demographics hypothesis does have a sort of superficial plausibility. Japan’s population grew 12.5% between 1974 and 1991, and then only 3.0% from 1991 to 2012. Japan’s total employment grew 23.6 % between December 1974 and December 1991, and then actually fell by 2.4% over the following 21 years. Thus as population growth slowed, employment growth slowed even more dramatically. At the time, people assumed that an aging population was the culprit.

But when the Abe administration took office at the beginning of 2013, everything changed. Employment soared by 8.1% between December 2012 and November 2019, and yet the demographics actually got far worse.

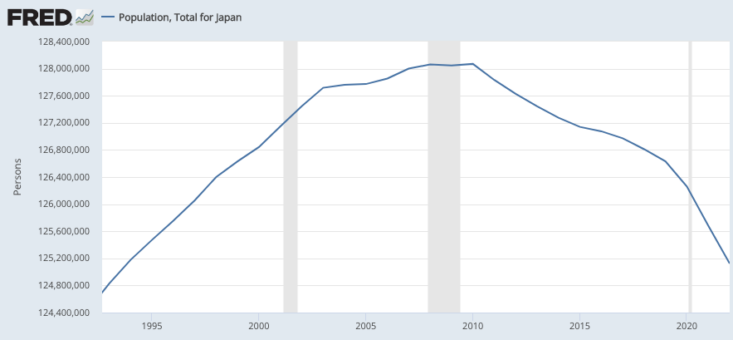

Population is now actually falling, and at an accelerating rate.

In addition to a falling population, Japan also has an aging population. But that “problem” actually got worse after 2012, so it doesn’t explain the dramatic employment shifts. I use scare quotes, as I’m not convinced that an aging population is actually a problem, at least by conventional metrics. If adults work on average during 75% of their expected adult lifespan, it really shouldn’t matter whether the life expectancy is 80, 180, or 580 years.

Many people (including me a few years ago) assumed that as Japan got older the Japanese would continue to stop working at the same age. But that doesn’t seem to have been the case, and thus the number of available bodies in Japan has risen much more than expected. That reflects both better health and less strenuous jobs.

(In the US, the employment/population ratio for age 55-64 and has hit all time high, while the ratio for over-65 group peaked in late 2019.)

It’s now clear that demographics never were Japan’s problem. Once monetary policy became a bit more expansionary, prices began rising and employment rose much faster than expected. Demographics may partly explain the low real interest rate in Japan, but the nominal rate is mostly determined by the trend rate of inflation, i.e. monetary policy.

In the future, demographics may be a problem for specific countries such as Italy, but only if they choose to make it a problem. There’s no reason to keep the retirement age at 62 as life expectancy rises sharply and jobs get softer. We may choose (in public pension plans) to allow the elderly to enjoy some extra years of retirement as we get richer, but there’s no reason for years spent in retirement to rise one for one with life expectancy. Japan is showing that there’s another way.

READER COMMENTS

Warren Platts

Oct 23 2023 at 3:06pm

So in countries like the United States where the life expectancy is falling, shouldn’t we lower the retirement age?

Mark Barbieri

Oct 23 2023 at 6:10pm

Who is “we”? In the United States, most people decide when to retire. It is not a decision imposed on them.

Warren Platts

Oct 24 2023 at 4:03am

“Retirement age” typically refers to when social security benefits kick in.

Scott Sumner

Oct 24 2023 at 6:55am

“shouldn’t we lower the retirement age?”

Life expectancy has risen significantly since Social Security was created in the 1930s with a 65 retirement age. So the answer is no.

robc

Oct 24 2023 at 12:16pm

IIRC, the original 65 was picked because it was slightly above the life expectancy. If the SS retirement age had kept track, it wouldn’t be at 67 but at 80.

Rock Lobster

Oct 24 2023 at 2:42pm

US life expectancy has fallen because younger people are dying more from guns, car accidents, drugs, etc. “Life expectancy” for a retiree, i.e. life expectancy conditional on reaching 65, has continued to rise. Therefore pension accounting is not “improved” by the lower life expectancy.

Ahmed Fares

Oct 23 2023 at 3:22pm

A bit on the methodology:

https://twitter.com/CXCarroll/status/1527323849305382920?s=20&t=a281JTmLfPCh-YXNTzcHMg

Matthias

Oct 23 2023 at 7:37pm

Even exponential decay by age cohorts is rather naive in the longer run.

Different subgroups of the population will have different fertility rates. For example, people with some specific religions might have much higher fertility rates. (And some groups like Catholic priests will have much lower fertility rates.)

To forecast for only a few decades, a single generation, simple averages per cohort can be used. But for longer you need a more complicated model, as a bigger and bigger proportion of people will be descendants of those with comparatively higher fertilizer rates.

If any of the reasons for the increased fertility rate persist across generations, like religion or even genes, that will make a difference.

john hare

Oct 23 2023 at 6:09pm

At 67 I still do concrete work, albeit at a slower rate than 30 years ago. I’ll stop when I feel like it.

Jeff

Oct 24 2023 at 5:39am

“That reflects both better health and less strenuous jobs.”

Or does it reflect rising costs of living forcing the elderly to work?

Setting some arbitrary percentage of life for people to work seems rather facile, since the capacity to work and—just as importantly—the capacity to develop oneself for future work, would not seem to scale linearly with lifespan.

Scott Sumner

Oct 24 2023 at 6:57am

“Or does it reflect rising costs of living forcing the elderly to work?”

No, because real wages have risen.

john hare

Oct 24 2023 at 6:00pm

I think that represents top down thinking determining what the retirement age should be. I’ve know people retired at 55 and others still working in their 80s, both by choice.

spencer

Oct 24 2023 at 9:54am

Bank lending is a function of the velocity of deposits, not their volume. The demand for money is much higher in Japan.

Thomas L Hutcheson

Oct 24 2023 at 5:18pm

The best reason for raising the “retirement age” is not to reduce SS expenditures, but to attack the societal norm of age based “retirement.”

Filippo

Oct 25 2023 at 8:15am

In Italy, it’s been since 2011 that retirement age is at 67, not 62. This could ease the problem for a while, but 10 years after we hace the same problem (a lot of workers are retiring and only a small number is entering in the workforce)

Rob

Oct 29 2023 at 12:29pm

Sure, raise the retirement age. You’ll get a pretty big increase in disability applications and benefit expenditures.

Many people doing physical labor have back and joint problems eventually and won’t be able to keep working until the higher retirement ages that some propose.

“Less strenuous jobs” for them? A 55 year old construction tradesman with bad knees is going to retrain as a coder. Right. Greeter at WalMart doesn’t pay very much. Hard on the knees, too.

John

Nov 11 2023 at 6:22pm

Retirement age in Italy is not 62, it’s 67 and will rise in the next decades to reach 70.

Comments are closed.