George Selgin has an excellent post on the history of FDIC. I already knew that FDR had opposed the idea of deposit insurance and was pressured into agreeing to the proposal in order to achieve his other banking reform goals. But this was new to me:

Carter Golembe (1960, 195) zeros in on the truth. “[I]t is not reading too much into history,” Golembe says, to regard deposit insurance schemes as “attempts to maintain a banking system composed of thousands of independent banks by alleviating one serious shortcoming of such a system: its proneness to bank suspensions, in good times and bad.” Henry Steagall, who was second to none in his determination to save the United States’ small unit banks, made no bones about this. “This bill,” he said, referring to his May 1933 effort, “will preserve independent dual banking in the United States. … This is what the bill is intended to do” (ibid., 198).

Insurance and branching were, in short, rival reform options; one sought to preserve the unit banking status quo, and particularly state-chartered unit banks, despite their inherent weaknesses; the other would instead have allowed banks to branch statewide, if not nationwide, which would have meant more relatively large and well-diversified banks with branches, and many fewer smaller unit banks. Steagall favored the insurance option, while opposing branch banking tooth-and-nail. Carter Glass, his Senate Banking Committee counterpart, took the opposite position.

I increasingly believe that it makes sense to view federal deposit insurance and the small banking bias of our regulatory system as part of a unified regime that aims to create moral hazard—to encourage banks to take socially excessive risks. From the point of view of Congress, this risk-taking is a feature, not a bug. That’s why neither political party is proposing any sort of reforms to fix the problem. Indeed the problem is likely to get worse over time.

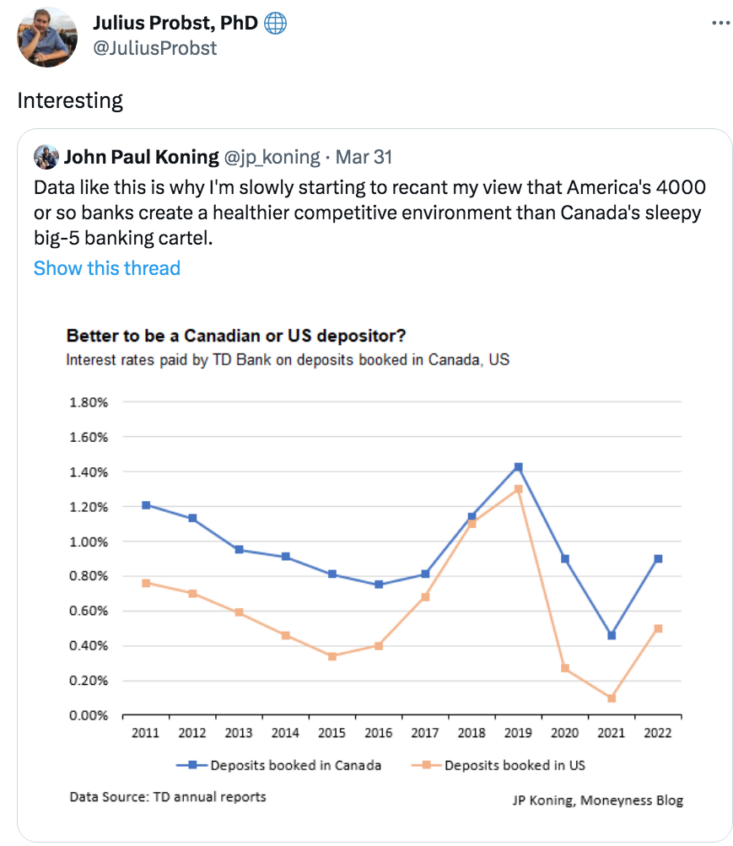

In a free market regime, the US system would consolidate into a smaller number of large, well diversified banks. Some worry that adoption of the Canadian approach would offer too little choice to consumers. But the US is much larger than Canada, and would end up with more than 5 large banks. In any case, this tweet casts doubt on the view that concentration hurts depositors:

Update: This post was certainly not well timed!

READER COMMENTS

Andrew_FL

Apr 4 2023 at 11:22am

If the number of US banks were in the same proportion to population as Canada there would be about 43 banks. Proportional to GDP, about 57.

Scott H.

Apr 4 2023 at 3:04pm

But does the optimal number of market participants in a mature, largely commoditized market depend on the number of customers or total GDP within the market?

BS

Apr 5 2023 at 12:00pm

FWIW, the US has 3 really big telecomm companies that stand out above the competition…and Canada also has 3.

TMC

Apr 4 2023 at 11:26am

Interest rates should be higher just to compensate for Canada’s higher inflation rate during that period. I don’t see any adjustment for that.

Scott Sumner

Apr 4 2023 at 1:51pm

Actually, you’d adjust by comparing spreads with other rates, say 3-month T-bills in each country. That’s a mixed picture. (Assuming these are rates on each domestic currency, not just US dollars.)

Airman Spry Shark

Apr 4 2023 at 2:27pm

I don’t doubt that Congress would seek something socially harmful, but I don’t follow why they’d do do in this specific case.

Scott Sumner

Apr 4 2023 at 5:12pm

The power of lobbyists (for small banks, property developers, etc.)

BC

Apr 5 2023 at 1:24am

Small banks, depositors, and borrowers (mortgagees and business borrowers) all have a concentrated interest in having the dispersed taxpayers backstop their activities. Ironically, the policymakers (regulators and Congress), who nominally represent taxpayers, don’t even say that their goal is to minimize taxpayer exposure. Their stated goal is to make private depositors feel perfectly safe, i.e., provide a guaranteed backstop, while ensuring that banks provide access to credit for private borrowers. Of course, “provide access to credit” is another way to say “take risk”.

vince

Apr 4 2023 at 2:47pm

“In a free market regime, the US system would consolidate into a smaller number of large, well diversified banks.”

Contrary to the ideal of perfect competition.

Wouldn’t that consolidation worsen the problem of TBTF? Private gains, public losses? Heads, banking wins, and tails, taxpayers lose?

Scott Sumner

Apr 4 2023 at 5:13pm

“Wouldn’t that consolidation worsen the problem of TBTF?”

It might, but we already have that problem. I believe the benefits would outweigh the costs.

milljas

Apr 10 2023 at 3:55pm

Can you expand here or in a post why large and diversified banks are a good thing? If there’s a run on a brand say with JPM and that run perpetuated across the entirety of the business that would seem quite terrifying. The same would hold true for RBC or BMO. I don’t understand if that is at the heart of makes the Canadian system healthier or is that the result? Both countries have deposit insurance, although we have less per person. Fragile by Design is a book that has been written about the instability of the US system premised on game theory among politicians and regulators, is that sort of book that might be helpful?

Matthew Waters

Apr 4 2023 at 6:27pm

That is interesting. I will say that the big money center banks relied on clearinghouse certificates and clearing each other checks.

The certificates were printed in 1933 and were about to be used before the national bank holiday. The New York Times on that day had ads from shops saying “we will take checks and certificates at par.”

The suspensions/certificates were better than bank holidays, but they still sort of relied on a legal fiction where banks were sort of allowed to default in bad times.

Majid Hosseini

Apr 5 2023 at 2:29am

I have accounts in both in a national bank and in a California-based regional bank. The quality of service in the regional bank is infinitely better. I consider it a loss that the regional bank is getting acquired by a larger bank. I am fairly confident the same level of service won’t be available anymore. The fact that the regional bank pays little interest is a non-issue for me.

Spencer

Apr 5 2023 at 10:22am

All monetary savings, income not spent, originates within the confines of the commercial banking system. Time/savings deposits have just been shifted from transaction deposits (bank credit remains the same).

Since time deposits originate within the banking system (and there is a one-to-one relationship between time and demand deposits — an increase in TDs depletes DDs by an equivalent amount), there cannot be an “inflow” of time/savings deposits and the growth of time/savings deposits cannot, per se, increase the size of the banking system.

From a system standpoint, TDs constitute an alteration of bank liabilities, their growth does not per se add to the “footings” of the consolidated balance sheet for the system.

So, it makes no sense for the banks collectively to pay for something that they already own, uninsured deposits. The economies of scale just produce larger and fewer banks.

Spencer

Apr 5 2023 at 11:00am

Richard Werner rightly thinks ‘big banks are a cancer on society’

steve

Apr 6 2023 at 12:50pm

Canada provided about $114 billion in liquidity support during the financial crisis. How would you view that?

Steve

Comments are closed.