Suppose you measure something (say, GDP) in two steps: first, you add in some number (say, the value of imports); second, you subtract the same value. You may say, focusing on the second operation, that “imports are a subtraction in the calculation of GDP.” You may equally say, focusing on the first operation, that “imports are an addition in the calculation of GDP.” But if you consider the two operations together, the truth is that imports are not a part of GDP and thus neither decrease nor increase it: +A-A=0. The reason is that GDP is defined as the domestic production of final goods and services, which is the “D” in Gross Domestic Product.

In its press releases (including the release of April 30), the Bureau of Economic Analysis (BEA) chooses the second formulation instead of the first one or of both together. This focus is highly misleading and does not correspond to the bureau’s methodology and technical literature.

The total value of the final goods and services produced domestically in an economy (including capital goods and any increase in inventories) is, by definition, equal to total expenditures (including savings and what is produced but not sold during the period under consideration). In other words, looking at GDP from the expenditures side, we have the familiar equation:

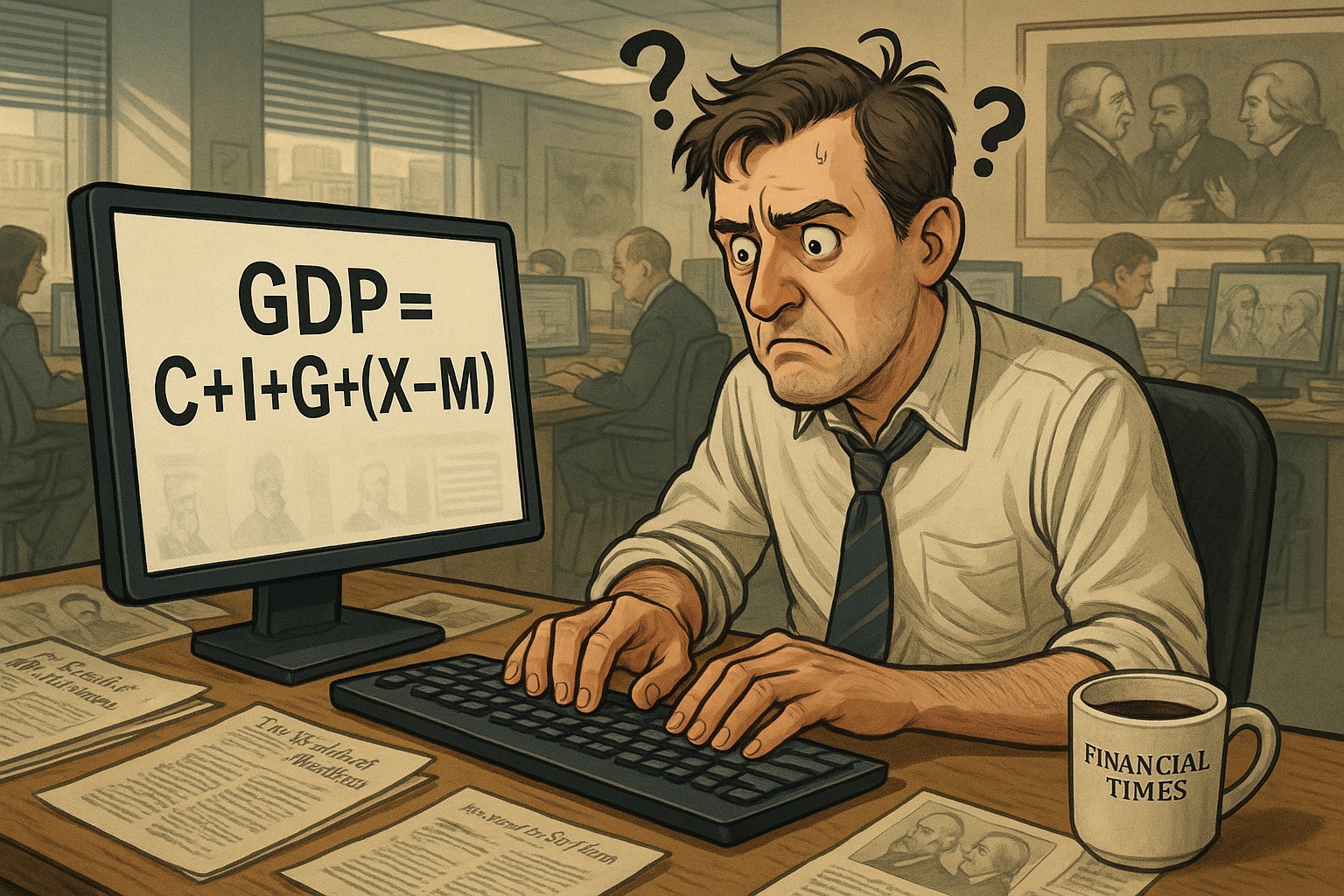

GDP = C + I + G + X – M.

Forget M for the moment. The equation, which is an accounting identity, says that GDP must also be equal to the sum of consumption expenditures (C), investment expenditures (I), government expenditures (G), and exports (X), if none of these components include imports, for GDP is gross domestic product. In fact, each of these four variables (C, I, G, X), as statistically collected, does include imports. Consequently, the (separately calculated) total value of imports (M) must be subtracted to remove the imports from the total. Hence the formula above.

The equation is typically rewritten as its exact mathematical equivalent

GDP = C + I +G + (X – M),

mistakenly suggesting the false interpretation that the “net exports” or “trade deficit” (X – M) subtract something from GDP. The expert or the economics student who has taken a good college course of introductory macroeconomics knows that this interpretation is not correct. But the ordinary person or the superficial journalist or editor is easily misled. The false interpretation also provides the protectionist activists (like Peter Navarro, despite his Harvard PhD in economics!) with an invalid argument that imports reduce GDP.

The reader interested in further explanations and citations including to the BEA) will find several articles and posts of mine: “Gross Domestic Error in The Economist,” EconLog, May 28, 2019); “The St. Louis Fed on Imports and GDP,” EconLog, September 6, 2018; “Peter Navarro’s Conversion,” Regulation, Fall 2018; “Misleading Bureaucratese,” EconLog, October 30, 2017); “A Glaring Misuse of GDP,” Regulation, Winter 2016-2017, (p. 68) ; “Are Imports a Drag on the Economy?” Regulation, Fall 2015.

As you can verify, the Wall Street Journal has not come to grips with this simple statistical fact. Very interestingly, and for the first time to my knowledge, The Economist has just shown that it understands: see “Don’t Blame Imports for the Fall in America’s GDP,” May 1, 2025.

It is important to distinguish between an accounting identity (such as the one discussed above) and an economic argument. The former is true by definition; the latter needs a valid theory and supporting evidence. It is difficult, if not impossible, to build a valid protectionist theory demonstrating that imports reduce GDP. Standard economic theory, on the contrary, can explain, among other phenomena, how a foreign war embargo or, equivalently, domestic tariffs or bans can hit production via imported inputs (inputs account for more than half of all imports in America).

According to the BEA’s advance estimate (which is nearly always revised as more data become available), the American GDP declined by 0.3% in the first quarter of 2025 compared to the last quarter of 2024, while imports increased by 41%.

One explanation for the coincidence of higher imports and lower GDP in Q1 is the frontloading of imports before President Trump’s tariffs hit. Consumers, intermediaries, and producers tried to beat the tariff deadlines. For example, car dealers increased their inventories of foreign-made cars (or those containing foreign-made parts) to satisfy the demand of their customers. The high maritime traffic between China and Los Angeles confirms the frontloading of many other imports. Responding to consumer demand, domestic production of substitutes could have been consequently reduced. But the phenomenon would soon be compensated by the (reverse) substitution of domestic for imported production as the tariffs come into force.

Another explanation is simply that the uncertainty and pessimistic expectations provoked by Trump’s protectionist intentions were sufficient to start a recession, which is defined as negative levels of GDP and their consequences in terms of unemployment, etc. We will learn more as events develop and new data become available, but not with the help of an accounting identity that says nothing about imports.

******************************

ChatGPT took the initiative of adding a wall picture. It seemed to me that the person on the left looked like Adam Smith and the one in the middle like Karl Marx. I asked “him” about that and he confirmed. The one on the right, he said, is John Maynard Keynes. I decided it was not a bad idea and kept it, although such a picture would be unusual in a newsroom.

Puzzled journalist

READER COMMENTS

Scott Sumner

May 3 2025 at 11:38am

“As you can verify, neither the Wall Street Journal nor the Financial Times has come to grips with this simple statistical fact.”

Sorry, but this is wrong. The Financial Times story is correct; the imports did reduce reported GDP, but not actual GDP. They’ll show up in next quarter’s GDP, when they are counted in inventory investment and consumption. The BLS calculation technique is flawed, which is why imports may reduce measured GDP.

Here’s what the FT said:

“Morgan Stanley economists said the surge of imports ultimately contributed to inventories, consumption and investment — positive factors in calculating GDP that were not fully reflected in Wednesday’s data.

‘In effect, the imports don’t fully appear in the spending parts of the GDP accounts and therefore exaggerate GDP weakness,’ they said.”

They’ll be “fully reflected” next quarter.

Scott Sumner

May 3 2025 at 1:33pm

To be clear, I agree with your overall take that people mistakenly assume that the GDP equation implies imports reduce GDP. Imports have no direct effect on actual GDP, for the reasons you suggest.

Pierre Lemieux

May 3 2025 at 2:37pm

Scott: I reread the FT story and I think you are right. (But I find this story badly written.) It quotes Morgan Stanley economists as saying–a quote you reproduce in your comment:

I understand this as meaning that data collection timing understated C and I by a certain amount of imports in calculated Q1 GDP, thereby not totally compensating for the M in the accounting identity. I agree that this is a valid argument. (I think that’s also Craig’s point.)

I’ll think about whether I should delete the mention of FT that accompanies that of the WSJ in my post. If I do, readers from now on will know they owe this to your comment. (The FT cup on the featured image will alas remain there forever as a symbol of human imperfection!) And thanks for your comment.

José Pablo

May 4 2025 at 10:20pm

It may have to be with the precision/timing of how imports are measured (customs records) compare with how inventories increases (investment) are measured (voluntary surveys)

Some of the imports of the first quarter could have not been properly measured as “investment” just yet

Pierre Lemieux

May 5 2025 at 5:40pm

Jose: Yes, that’s what I meant by “data collection timing.“

Craig

May 3 2025 at 11:53am

I think we will find out for sure next quarter. Sonething similar can happen with companies reporting income that engage in channel stuffing to manipulate quarterly reporting. Of course that then gets reported in the next quarter, so the reality is the reality but the accounting is the accounting and even presuming good faith the moment we do accounting over specific time oeriods, I don’t care what they are, there WILL be some degree of imprecision with respect to events that straddle the time in one way or another.

David Seltzer

May 3 2025 at 2:27pm

Pierre: Informative as always. Thinking about this: Imports are paid for to foreign exporting countries. The exporting country has cash which means more money for investment in the importing country. A percentage of that money goes to savings. Assumption: Ceteris paribus, an increase in the supply of savings lowers the price of money. Cheaper money allows individuals to invest more. In the longer run, wouldn’t that mean more investment in physical and human capital would increase in GDP?

Pierre Lemieux

May 3 2025 at 8:41pm

David: Yes, that’s a good point, ceteris paribus.

Jose Pablo

May 3 2025 at 4:38pm

The equation is typically rewritten as its exact mathematical equivalent

GDP = C + I +G + (X – M),

mistakenly suggesting the false interpretation that the “net exports” or “trade deficit” (X – M) subtract something from GDP

As you rightly point out, it’s astonishing how much confusion this equation can cause for the untrained mind.

Remarkably Trump supporters fail to see that if a reduction of the trade deficit truly increases GDP, then by that same logic, a reduction of government spending must decrease it. Yet former President Trump has been on a mission to cut government spending. In fact, using some of the figures “promised” by DOGE the net effect of fully eliminating trade deficit plus getting the targeted reduction of government spending, should result in a net reduction of GDP. Trump’s supporters don’t seem to notice the contradiction.

But GDP accounting is not the right tool to understand how much an economy can produce. For that, we need to turn to the production function, which focuses on inputs like labor, capital, and total factor productivity (TFP).

So, what Trump supporters should really be asking is how reducing the trade deficit affects these productive inputs:

Labor: It’s hard to see how reducing the trade deficit would boost this factor. Especially when immigration restrictions should have a negative impact on it.

Investment: Reducing the trade deficit would necessarily reduce capital inflows. Foreign investment in the U.S. is largely financed by the trade deficit itself.

Total Factor Productivity: It’s also unclear how reshoring the T-shirt production to Alabama would enhance TFP.

Warren Platts

May 4 2025 at 4:18am

Per Mankiw’s textbook, the full, expanded GDP equation is this:

Y = (Cd+Id+Gd) + (Cf+If+Gf) + (X-M)

where M = (Cf+If+Gf) and Y = (Cd+Id+Gd)+X and (C+I+G) = (Cd+Id+Gd) + (Cf+If+Gf).

So what happens to Y if you go from an initial state of M >> X to a subsequent state where M is reduced by ΔM such that M = X? I think it would have to depend on how consumers, investors, and the government react, right? (C+I+G) represents total spending, including imports; i.e., I don’t think it would be too incorrect to say that (C+I+G) is a measure of total aggregate demand. So if imports are reduced by ΔM because of a tariff, and if (C+I+G) are also reduced by ΔM, then Y need not budge one inch. But if (C+I+G) stay constant, that entails that (Cf+If+Gf) declines by ΔM and that (Cd+Id+Gd) must increase by ΔM (as consumers, investors, and the government substitute domestic production for imports) and thus Y must also increase by ΔM. Of course there is an entire spectrum of possibilities between these two extremes.

Jon Murphy

May 4 2025 at 7:52am

Never reason from an accounting identity. One needs economic theory to understand what happens and what is possible.

Jose Pablo

May 4 2025 at 3:31pm

How, precisely, would a reduction in imports enhance the American economy’s capacity to produce more goods and services.

Increased output requires a larger labor force, greater capital investment, or higher productivity. Yet, it is difficult to find a credible mechanism by which restricting imports would directly improve any of these factors.

On the contrary, by limiting access to cheaper inputs, advanced technologies, and competitive pressures, protectionist measures such as tariffs are more likely to reduce investment and stifle productivity.

I am all ears. A meaningful theory of how this work from the “production side” is long overdue

If the goal is to stimulate economic dynamism, reducing the flow of goods, ideas and competition from abroad seems an oddly self-defeating strategy

Warren Platts

May 4 2025 at 5:01pm

Jose, think about it this way: one function of a big trade surplus is to export unemployment; your workers may not have enough money to buy their own production, but you can still put them to work if you can sell the excess production overseas. The obverse side of this coin is that you will be importing foreign demand.

Conversely, the deficit countries must export demand and import unemployment. Note I am using “employment” to mean more than just the number of hours supplied: because the trade deficit reduces the demand for home labor, wage levels will decline, even if the number of jobs stays the same. (Yes, the real wages for some people will go up, especially the laptop class who, for the most part, do not labor in import-competing sectors; however, real wages for the working class will go down because the cheaper imports do not outweigh the erosion of their real wages through inflation and unemployment.)

Thus the plan is that by insisting on balanced trade in goods, demand for American manufactured goods will increase. The increase in demand will provide justification for more investment that currently is not there. This will indeed raise labor productivity because the new manufacturing jobs will not be filled by the most productive of our workforce: namely the lawyers, Wall Street financiers, academics, and the army of federal workers or the laptop class in general. Rather, the workers will be poached from Dollar General, McDonalds, and Walmart. Not only will these workers make more money, but more importantly, the GDP they generate per hour will be even more. And of course there bill be multiplier effects. However, laptop class real wages will go down somewhat in the short run. And I think it’s safe to say that most of the people actively debating these issues belong to the laptop class: thus, we must beware to try and not let an element of self-dealing bias our analysis. However, in the longer run, laptop class real wages will increase as the overall GDP growth rate increases.

Again, I’ve done a statistical analysis of average GDP growth rates by comparing post-NAFTA and Pre-NAFTA growth rates. They declined by one percentage point (a 28.5% decline). The null hypothesis that the pre & post NAFTA GDP growth rates are the same is rejected at p=0.90; granted, that’s not p=0.95, but it’s still pretty suggestive. There’s only a 10% chance the rates are the same and the observed difference is merely due to random variation. Note this was not supposed to happen: GDP growth rates were supposed to go up. That certainly didn’t happen: GDP growth rates either went down or stayed the same; they did not go up. Therefore, by insisting on balanced trade, the opposite effect is predicted to happen: GDP growth rates should go up; or in a worst case scenario, they will stay the same.

Jon Murphy

May 4 2025 at 8:52pm

That is insanely false.

Warren Platts

May 5 2025 at 6:43pm

That’s not “insanely” false; it’s necessarily true. When importing widget X, as you go from autarchy to free trade, the supply curve the importer faces moves to the right. The price goes down, the quantity demanded goes up until until it matches the quantity supplied by the world. Meantime, the quantity supplied by Home producers goes down. Thus, the Home country imports supply and exports demand.

If you are exporter of gadget Y, the situation is the opposite: as you go from autarchy to free trade, the demand curve you face effectively moves to the right. The price goes up, the quantity supplied goes up until it matches the quantity demanded by the world. Meantime, the quantity demanded by Home consumers goes down, but this is more than made up by the exports. Thus, the Home country imports demand and exports supply. (Yes, I know about Krugman’s dissertation where through clever industrial policy a country can corner the world market and thus obtain an economy of scale that reduces overall costs, thus potentially reducing prices worldwide, assuming monopoly pricing is not imposed.)

Thus, if you are a chronic, big surplus country, then you are a net importer of demand. If you are a chronic, big deficit country, you are a net exporter of demand. And demand is the most valuable comodity there is. This is why I disagree with Say’s so-called law. It is demand that drives supply. If there is not a pre-existing demand, then the supply is worthless and technically not even worthy of the name supply.

Pierre Lemieux

May 5 2025 at 9:31pm

Sorry, Warren, but this looks very confused. “Importing demand” is as meaningless as “buying demand” or “demanding demand.” And, of course, if the importing country (that is, the horizontal addition of the demand curves of this country’s residents) is small compared to the rest of the world, the world supply curve is, for all practical purposes, perfectly elastic. Technical terminology is useful because it avoids confusion.

Warren Platts

May 7 2025 at 10:03am

Sorry, I guess I should have written “aggregate demand” that the AI defines as: “Aggregate demand is the total demand for final goods and services in an economy at a given time.” It’s calculated by an equation that should look familiar:

AD = C + I + G + (X – M)

Of course AD is not identical to GDP. According to Investopedia: “GDP represents the total amount of goods and services produced in an economy, while aggregate demand is the demand or desire for those goods.” [emphasis in original] Of course some of that AD will reflect a desire for imports. Thus the question is whether it can possibly make sense to say that a surplus country “imports” AD or whether a deficit country “exports” AD. I don’t see why not. The willingness to spend money on goods & services can be regarded as a commodity that world producers compete over in bidding wars. In that sense, it can be said that a surplus country is a net importer of aggregate demand.

Pierre Lemieux

May 7 2025 at 4:51pm

Warren: Aggregate demand is a concept in Keynesian theory. It can be represented by C+I+G+X-M in equilibrium or, by definition, in the accounting framework of national accounting (which is Keynesian inspired). If, as you seem to, you argue that aggregate demand drives GDP, you are doing Keynesian economics, and believe that increasing government expenditure creates some GDP. Still, after a century of analysis, I don’t think that any Keynesian theorist would find it useful, as opposed to confusing, to speak about importing or exporting aggregate demand. A standard introductory text on macroeconomics is Cowen and Tabarrok’s (Macroeconomics), which discusses different macroeconomic theories including the Keynesian one. (It seems to me it could have been a bit clearer on C+I+G+X-M, at least in the edition I have.)

Jose Pablo

May 5 2025 at 10:48pm

Thank you, Warren, for your detailed response.

I happen to know a few people in the business of importing lumber, steel, and cement. But I certainly don’t know anyone in the business of importing unemployment. These kinds of narratives tend to obscure more than they clarify.

The idea that insisting on balanced trade in goods will automatically increase demand for American-made products is questionable. An alternative scenario is that such a policy could simply reduce consumption and investment, especially in goods and services that the U.S. either cannot produce at all, or cannot produce at reasonable prices.

Not to mention the abundant “granularity issues”, which seem to be overlooked in your narrative. For all we know, some states, and for sure some sectors, could be running a trade surplus. Forcing a balanced trade upon these regions and/or sectors could increase unemployment in these areas of the economy. We have virtually no data on subnational trade balances, yet some cities, counties, or even states are likely running trade surpluses.

Your theory seems to assume a level of labor mobility, both geographically and in terms of skill sets, that may not exist in reality.

I’m not sure it’s worth taking such risks, especially when the potential payoff is, at best, a questionable 4% (the whole amount of the trade deficit) boost in domestic production.

Jon Murphy

May 5 2025 at 8:56am

It is theoretically possible under certain conditions. If imports are a substitute for domestic production and there are economies of scale, then it is possible that reduced imports could increase the capacity for production.

One should note that every time this method has been applied in the past, it hasn’t worked.

One should also note that such necessary conditions do not apply to the US. For one, our imports are complimentary to domestic production, not substitutes (so, increasing their prices via tariffs will reduce domestic output, as we are already seeing). For another, given we are one of the largest manufacturers in the world, it’s unlikely there are unexploited economies of scale.

TMC

May 5 2025 at 8:57am

The BEA announced Government spending (G) went down 5.1% this past calendar quarter.

Also, US Debt Clock on:

Jan 2023 – 31.6 Trillion;

Jan 2024 – 33.6 Trillion = 2 Trillion Increase;

Jan 2025 – 36.3 Trillion = 2.7 Trillion Increase;

May 2025 – 36.8 Trillion = 500 Million in 4 months, a projected 1.5 Trillion by Jan 2026, maybe closer to a Trillion if we continue to decrease 5.1% each quarter.

Sometimes GDP going down isn’t bad.

Pierre Lemieux

May 5 2025 at 3:32pm

TMC: I don’t know how you get your conclusion. According to the BEA data published on April 30, 2025 (see Table 3), Q1 federal expenditures, were $1,925.3 billion, compared to $1,924.7 in 2024 Q4, for a reduction of 1.3% (all data in constand dollars of 2017). (Compared to 2024 Q1, the table shows an increase of federal expenditures in current dollars.) Wishfully assume a continuing reduction of 1.3% per quarter (quarter to quarter) in 2025, that is, a reduction of federal expenditures of about 5% in 2025 (calendar year). This would have little impact on the public debt. To reduce the latter, a budget surplus is required, which would require a reduction of about one-third in annual expenditures.

Anyway, we should not reason from an accounting identity (as Jon Muphy says above), including from the (strange) idea that government expenditures increase GDP. Any reimbursement of the public debt comes from government revenues, which crucially depend on the level of GDP. Reducing GDP reduces the possibility of reducing the public debt, ceteris paribus.

TMC

May 5 2025 at 5:31pm

First step is to reduce the debt is to reduce the deficit. We are going in the right direction. I don’t think anyone expected a $2 Trillion reduction in the first three months.

My point is though, GDP went down because a big component of it (G) went down.

Jose Pablo

May 5 2025 at 10:15pm

a big component of it (G) went down.

Nah! No “big component” involved. The federal government’s share of G in the GDP formula is actually quite small, around 6.5%.

In fact, most of the federal budget (around 2/3) consists of transfer payments between Americans, which don’t count toward GDP (transfers like, for instance, interest payments on the national debt.)

TMC

May 6 2025 at 8:22am

Well were in luck then, as imports are even smaller, 2/3s the amount. No need to even discuss these piddling amounts.

To me 6.5%, or $6T is not small.

Jose Pablo

May 5 2025 at 2:34pm

My favorite way to think about the identity used to calculate GDP is:

GDP + (M – X) = C + I + G

This essentially means that the goods and services “we” (American individuals added together) produce domestically, plus the trade deficit, must equal the total of American consumption (both private and government) plus American investment (also private and government).

So, the trade deficit actually enables us to consume and invest more than we produce. In that sense, it “helps” us!.

Of course, this is still just an accounting identity (as Jon rightly points out). It’s just the way of working out GDP, not a model that can, by itself, explain causality or behavior (is that clear?). So, no conclusions should be drawn from it alone. Still, I think this formulation could help to avoid some common misconceptions.

Also important: These figures represent real goods and services, even though they’re expressed in dollar terms for comparability. But they are not dollars themselves. This distinction matters, especially when people start thinking in terms of “substitutions.” The currency is a commodity, you can substitute it, trade it, hoard it. But goods and services in the GDP identity are not interchangeable in the same way. You can’t just swap one for another freely.

And let’s put some real numbers to it, which is very illustrative.

Suppose GDP = 100, then (M – X) = 4

Really? All this noise over a 4% increase in our ability to consume and invest?! Come on. We sure have more serious things to worry about.

Now, breaking it down further, C (Consumption) = 69, I (Investment) = 18, G (Government Spending and Investment, excluding transfers like, for instance, interest payments) = 17

Note: This 17% includes all levels of government, federal, state, and local. Only about 6.5% of it comes from the federal government, most of whose actual outlays are in the form of transfers, which don’t count toward GDP.

Now, if you really want to (mis)use this formula the way some Trump supporters tend to do, you’ll quickly find that the real “enemy” isn’t imports, but exports. Reduce exports, and, voilà!, you increase domestic consumption and investment. That’s the real path to “Making America Great Again,” right?

Oh, and one more thing: Cutting government spending, as this administration is doing, reduces G, which in turn reduces GDP. That’s the textbook definition of a recessionary force. Though, to be fair, the federal government’s contribution to production is just 6.5%, so maybe not a huge immediate concern…

Macroeconomic thinking “a la Trump” certainly is a lot of fun!!

Warren Platts

May 6 2025 at 4:38am

This is not exactly true. For example, the government spends $1.35 trillion on Social Security. This may not show up on the G variable of the GDP equation, but it sure as heck shows on on the C variable. If the government somehow magically canceled Social Security, C would decline by 6.5% and GDP would decline by 4.5%

Pierre Lemieux

May 6 2025 at 10:42am

Warren: No. Transfers are not included in GDP. GDP is production of final market goods and services.

Jose Pablo

May 6 2025 at 1:36pm

it sure as heck shows on the C variable

Well, maybe the recipients of the transfers have a higher propensity to spend than “forced donors”. Or maybe not. I am always agnostic about these kinds of things. But I am pretty sure that “forced donors” have a higher propensity to invest. Which also shows on the GDP.

Warren Platts

May 7 2025 at 9:38am

OK, after thinking about it some more, I concede Jose and Pierre’s point: transfers per se wouldn’t affect GDP, at least in the short run. However, transfers could affect the values of various GDP boxes: old folks barely scraping by probably spend most of their social security checks on consumption, hence counted in the “C” box. If the government decided to spend the $1.6 trillion on infrastructure construction and procuring of expensive weapons systems, then it would be in the “G” box. Or if the payroll tax was ended entirely, then perhaps most of the tax savings would be invested in IRAs, in which case it would wind up in the “I” box. Which of these three scenarios would be the most desirable I reckon is debatable.

Pierre Lemieux

May 7 2025 at 4:31pm

Warran: Two points:

Of course, transfers could affect GDP, for example if they led people to produce less. It is simply that transfers are not production and, thus, by definition, not part of GDP.

A simple introduction to GDP is provided by the BEA; an even simpler one, by my Regulation article, “What You Always Wanted to Know about GDP but Were Afraid to Ask.” For more, the BEA has a big book on the NIPA’s sources and methods.

Jose Pablo

May 5 2025 at 2:50pm

GDP + (M – X) = C + I + G

GDP = 100, (M – X) = 4, C = 69, I = 18 and G = 17

Once you start thinking like a Trumpist macroeconomist, it’s hard to stop!

Let’s imagine, for a moment, that the Trumpists are right—and that: a) the entire trade deficit can be eliminated, and b) domestic production can perfectly substitute for all imports we currently rely on.

That would mean, using this (misapplied) identity, GDP would rise by 4%. Not bad, it’s roughly equivalent to two years of organic growth. But it’s hardly Making Anything Great Again.

Now imagine the uncertainty created by erratic tariff policy and trade wars causes consumption and investment to fall by 20%. That would imply an 18% drop in GDP + (M − X).

Add to that another 2% drop in government spending, let’s say DOGE becomes a wild success and deep federal cuts follow. That’s a full 20% contraction in domestic demand.

Trumpists would argue that 4% of that is offset by eliminating the trade deficit. But that still leaves a 15–20% drop in GDP.

So under this hypothetical, and using the Trump-style misinterpretation of this identity, tariff-driven trade policy could lead to a deep recession.

This kind of “Macroeconomics, Trump Edition™” is dangerously simplistic… but admittedly, kind of addictive to play with!

Pierre Lemieux

May 5 2025 at 5:18pm

Jose: I think you did not draw the final corollaries and results of your Keynesian analysis. Interestingly, it can help us derive the correct values for the increase in Trump’s “reciprocal tariffs” for each country i. The White House already published its formula. Now, recognizing that Trump=Biden=Keynes=φ and neglecting ε (which is just a decreasing remnant of the Biden economy), the numerator can be written 3φ×mi. So, counter-intuitively and interestingly (I am myself surprised), the greater is φ (=Trump=Biden=Keynes), the smaller should be the increase in the reciprocal tariff imposed on imports from country i.

Jose Pablo

May 5 2025 at 10:07pm

the greater is φ (=Trump=Biden=Keynes), the smaller should be the increase in the reciprocal tariff imposed on imports from country i.

Interesting! But since φ = φ(t) and quite likely ε = ε(t) as well, it follows that the reciprocal tariff adjustment—Δτᵢ—should also be time-dependent: Δτᵢ = Δτᵢ(t).

Clearly, we need to establish a Technical Committee for the Continuous Adjustment of Reciprocal Tariffs. Who knew? Trump might actually be boosting demand for economists!

Of course—strictly domestic economists need apply.

Rui Viana

May 7 2025 at 7:59am

I looked through the articles you linked but didn’t you engage with the steelman of the opposing argument. The argument that made JD Vance the VP. Imports can substitute for domestic production and directly reduce GDP. What’s your take on that?

Pierre Lemieux

May 8 2025 at 9:13pm

Rui: See my response to your longer message. And don’t think you will learn economics with JD Vance. Even if he knew some economics, you never know if he will tell the truth: he and Trump claimed that Haitians ate pets in Springfield, Ohio, knowing that it was false.

Rui Viana

May 7 2025 at 8:16am

And I don’t mean to pick on you, but I’ve seen a lot of “imports don’t reduce GDP” takes on accounting identities, like the above, and not a lot of economists engaging with the core argument the other side is making. It’s a powerful argument that is moving our politics, and warrants a heads-on response.

For example: Noah Smith starts touching on it but stops short. If you follow his logic you’d conclude that tariffs on consumer products raise GDP, as long as you avoid tariffs on intermediate inputs. Trump should just tariff iphones and not steel?

https://www.noahpinion.blog/p/once-again-imports-do-not-subtract

Pierre Lemieux

May 8 2025 at 9:03pm

Rui: As I explained, one has to distinguish between an accounting identity (which does not include imports at all) and economic analysis, which has shown over the past three centuries that protectionism is inefficient and thus cannot increase production. The burden of the proof is on those who think the earth is flat–and very few economists think that forbidding your fellow citizens to import has generally good economic consequences. Just to illustrate, let me take the first paragraph you quote from Noah Smith.

The GM car produced in the US and unsold is accounted for in inventories (within I). GDP (which is domestic production) in year 1 is thus unchanged. In year 2, GM would produce one fewer car, and GDP would diminish in that year if nobody’s behavior changes. If the economy is flexible (that is, free), some resources (like labor) will be diverted from Ford production to produce something else US residents want (say, hotel services, since the purchaser of the BYD can now afford and may demand more vacation). Now, if the economy is not flexible and producers persist in producing things that consumers don’t demand, GDP will indeed be permanently reduced (think Soviet Union). You don’t need ANY imports for that to happen. Assume complete autarky. If producers produce stuff that consumers do not want, GDP (production) will certainly decrease: no producer will produce at a loss stuff that he cannot sell. Producers could only continue adding to their inventories if somebody, like taxpayers, were forced to pay for that, that is, to subsidize producers. If producers want to make money, they will produce what they have a comparative advantage in, and consumers will import stuff that is cheaper elsewhere. (It’s the same between California and Mississippi.)

My little book What’s Wrong With Protectionism provides some introduction to the economics of trade. I also have many posts on EconLog. Nothing replaces an introductory college course on international trade.

David Nowakowski

May 7 2025 at 10:31am

One additional way to illuminate the fact that imports don’t subtract GDP is a simple ‘degenerate case’. Imagine two countries, Williput and Blefescu. There is one good, eggs, which are produced and consumed. Williput’s chickens lay white eggs (W), but Williputians want brown eggs (B), which are only made by their neighbours, who in turn consume only white eggs.

So Williput’s Consumption is C=B, and exports are X=W.

If we sum up production, it is B+W. But clearly that is off: we know that production was just the white eggs. That’s because consumption was not produced in Williput, but imported from Blefescu. Hence GDP (W) = C + I + G + (X-M) = B + 0 + 0 + (W-B) = W.

That gives the right answer, production in Williput is W, white eggs. And it doesn’t matter if Blefescu produces more/less brown eggs which are imported and consumed by Lilliputians: Lilliput’s GDP is solely determined by its production of W, white eggs. [And vice versa for Blefescu – its GDP is B no matter what it imports).

Pierre Lemieux

May 8 2025 at 5:44pm

David: This is clever. It is worth noting, though, that your model includes both an accounting identity and an economic theory. The economic theory is that, left to themselves, the inhabitants of both Williput and Blefescu will produce what they have a comparative advantage in and consume what they prefer.

Dan Lieberman

May 12 2025 at 8:52pm

Aren’t imports a transfer from purchases of domestic production to purchases of foreign production? Without having imports in the GDP equation the GDP would decrease by double the amount. (X-M) reflects the GDP decease and this is due to the transfer from domestic production to imports. Imports affect GDP; money that could purchase domestic products or services leaves the country. That money supply is replaced by credit and this is one reason why the debt has grown. The PRC knows this and that is why it remains an exporting nation.

Pierre Lemieux

May 16 2025 at 3:17pm

Dan: No on all questions. Please reread my post and pursue your inquiry though my links and serious economic theory.

Comments are closed.