Commenter Cove77 directed me to an article in The Economist, discussing the “curious” lack of inflation in Japan:

Entrenched expectations built up through decades of little to no inflation play a big role in explaining why rising producer costs have not fed through to consumer prices. Domestic companies are notoriously unwilling to pass on increases in the prices of imports to consumers. At a press conference in October Kuroda Haruhiko, the governor of the Bank of Japan, attributed this reluctance to habits picked up during the country’s periodic bouts of deflation. Companies have a good reason to resist increases. Last week Kikkoman, a producer of soy sauce, announced a 4-10% increase in its prices from February. Such an event might barely be noticed in America. But in Japan it made the national news.

Another crucial factor is the weakness of Japan’s consumer recovery. Private spending fell in the third quarter of the year, and is now 3.5% below where it was at the end of 2019. Spending on durable goods, the source of much American inflation, has been practically flat for the past eight years in Japan.

The second paragraph is correct; a lack of consumer spending is the cause of Japan’s low inflation. (I prefer to focus on NGDP, but the two aggregates tend to move together.)

Given the lack of NGDP growth in Japan, low inflation is inevitable. The supposed “reluctance” of firms to raise prices (mentioned in the first paragraph) plays no role on the low Japanese inflation. To claim it does is to confuse causes and symptoms. (Conversely, in America you see people complain about “price gouging” by oil companies, an equally erroneous claim.)

It is theoretically possible that an unwillingness of firms to raise prices would lead to lower inflation, at least for a period of time. Thus suppose the BOJ increased Japanese NGDP at 5%/year over the next few years. If Japanese firms refused to raise prices then real GDP would also rise at 5%/year. At some point, however, you run out of workers; the growth in real output could not continue at that pace.

But this is not what is happening in Japan, where NGDP growth since the late 1990s has been negligible. Slow NGDP growth (i.e. tight money) fully explains the lack of Japanese inflation since 1996. After accounting for near-zero NGDP growth, there’s nothing left to explain from the pricing behavior of Japanese firms.

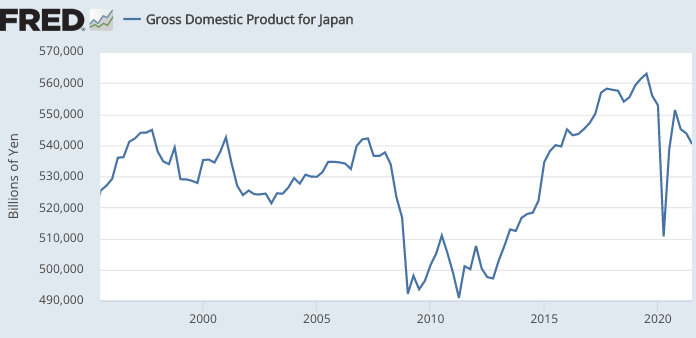

PS. Take a second look at the graph. It shows levels of NGDP, not growth rates. This is one of the most mind-boggling graphs in the entire history of modern macroeconomics. And by the way, Japan’s total population in 2020 is about the same as in 1996; so per capita NGDP is also flat. Imagine no raise in a quarter century! (In real terms Japan has done OK, but even there I’d say its performance has been a bit disappointing compared to countries such as the US, Australia, and Germany.)

READER COMMENTS

Alan Goldhammer

Nov 26 2021 at 1:59pm

Maybe Japan is also resistant to supply chain disruptions. They are only a short distance from the big export countries of Asia and also have a vibrant manufacturing economy of their own. Maybe the scenes of cargo ships waiting to unload in Los Angeles are just not an issue in Japan. This is the Occam’s Razor explanation from a non-economist.

Scott Sumner

Nov 26 2021 at 2:08pm

More likely, their lack of NGDP growth means there are few if any “shortages” to worry about in Japan. Our ports would not be backed if if not for the crazy surge in spending for goods during 2021.

Matthias

Nov 26 2021 at 7:15pm

Once stuff is in a container and loaded on the ship, physical distances cease to matter much.

The US also has a vibrant manufacturing economy.

Market Fiscalist

Nov 26 2021 at 4:10pm

‘Given the lack of NGDP growth in Japan, low inflation is inevitable. ‘

Couldn’t low NGDP growth combined with a supply shock lead to inflation ?

Scott Sumner

Nov 26 2021 at 5:48pm

Yes, for a brief period. But it’s very unlikely that you’d get any significant persistent inflation without NGDP growth.

rsm

Nov 27 2021 at 1:28am

Why do you have so much religious faith in magical numbers imputed by government bureaucrats,according to zero-sum assumptions about money that are relaxed by finance?

What if companies hedge inflation with inflation swaps, getting paid if their costs rise, and selling insurance to their customers not to raise their own prices?

《After accounting for near-zero NGDP growth, there’s nothing left to explain from the pricing behavior of Japanese firms.》

Why ignore finance? Do Japanese firms make more from financial markets than from real economy sales? Does NGDP even include financial returns? How much is off-balance-sheet?

How much do government statistics really tell you? Are you telling stories that say a lot about your fervent belief in government-supplied, opaque statistics reported without error bars, and say little about inflation?

BC

Nov 28 2021 at 5:27am

If Fed policy was to exchange money for gold until the price of gold was $35/oz, then hardly anyone would wonder why the price of gold was $35/oz. They would cite neither supply chains nor consumer spending. They would also understand that, as long as the relative price of gold to other goods was fairly stable, then the Fed’s gold trading would also explain why other prices were stable. If the relative price of gold to other goods were dropping or rising, however, then the Fed could still stabilize the average price of other goods by adjusting its gold price target. In other words, the Fed doesn’t need to trade other goods directly to affect their average price level; trading gold is sufficient because such gold trading increases or decreases the money supply and hence the value of money, which is the inverse of the average price level.

For some reason, however, when a central bank trades money for other assets besides gold such as treasuries and other securities, then many people — even people that think Fed gold-for-money trading is a good way to preserve the value of money — start looking for other factors beyond central bank money trading that might explain inflation, or lack thereof.

Scott Sumner

Nov 28 2021 at 1:53pm

BC, You said:

“If Fed policy was to exchange money for gold until the price of gold was $35/oz, then hardly anyone would wonder why the price of gold was $35/oz.”

Don’t be too sure about that!

Irving Fisher once told the following story (in a book entitled “The Money Illusion”:

I once jokingly asked my dentist —at a time when people were complaining about “the high cost of living”—whether the cost of gold for dentistry had risen. To my surprise he took me seriously and sent his clerk to look up the figures. She returned and said: “Doctor, you are paying the same price for your gold that you always have.”

Turning to me the dentist said: “Isn’t that surprising? Gold must be a very steady commodity.”

“It’s exactly as surprising,” I said, “as that a quart of milk is always worth 2 pints of milk.”

“I don’t understand,” he said.

“Well, what is a dollar?” I asked.

“I don’t know,” he replied.

“That’s the trouble,” I said. “The dollar is approximately one twentieth of an ounce; there are, therefore, twenty dollars in an ounce of gold, and naturally an ounce of gold must be worth $20. The dollar is a unit of weight, just as truly as the ounce is the unit of weight masquerading as a stable unit of value, or buying power.”

BC

Nov 28 2021 at 6:02pm

That’s funny. I stand corrected.

rsm

Nov 29 2021 at 1:26am

《trading gold is sufficient because such gold trading increases or decreases the money supply and hence the value of money, which is the inverse of the average price level.》

Why did banks regularly suspend convertibility? Why does the ratio you mention remain unobservable in available data? Has anyone ever kept strict convertibility?

Didn’t even von Mises acknowledge this problem with the naive theory of the price level you present, which reminded me of this passage from https://www.econlib.org/library/Mises/msT.html?chapter_num=12#book-reader

《The other similarly complete theory of the value of money is that version of the quantity theory associated with the name of Davanzati. *30 According to this theory, all the things that are able to satisfy human wants are conventionally equated with all the monetary metal. From this, since what is true of the whole is also true of its parts, the exchange ratios between commodity units and units of money can be deduced. Here we are confronted with a hypothesis that is not in any way supported by facts. To demonstrate its untenability once more would nowadays be a waste of time. Nevertheless, it must not be overlooked that Davanzati was the first who attempted to present the problem as a whole and to provide a theory that would explain not merely the variations in an existing exchange ratio between money and other economic goods, but also the origin of this ratio.》

If prices cannot be proven non-arbitrary, why even target nominal inflation? Why not simply index to maintain real purchasing power stability, no matter how high or fast nominal prices might rise?

In the Fisher story told in a comment below, wasn’t that $20 peg out of date very soon, thus revealing its ultimately arbitrary, political nature?

MarkLouis

Dec 2 2021 at 3:40pm

I’m not sold that Japan’s lack of inflation matters at all. The majority of GDP growth calculations fail to adjust for Japan’s aging population.

GDP per Capita (15-64 only) – 20 year annualized:

US: 1.26%

Japan: 1.30%

Comments are closed.