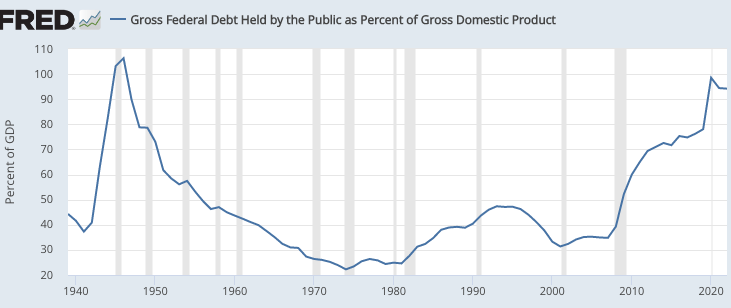

Ever since the late 2010s, the US fiscal situation has been on an unsustainable path. Of course, the problems began even earlier. But since the late 2010s, the budget deficit has become so large that the ratio of debt to GDP keep rising even during boom periods.

The situation is about to get worse. Here’s Bloomberg:

The US economy is set for an unexpected fiscal boost if lawmakers back a potential deal for $70 billion worth of tax breaks for businesses and families. . . .

“This is going to be a decent amount of fiscal cost with very little of it going to encourage new investment in a time when there are still inflation pressures,” Goldwein said.

Still, the plan could be a boon for President Joe Biden, whose poll numbers have slumped amid voter anxiety over the economy. Asked how the White House is weighing the potential inflationary impact of any proposal, Biden’s top economic adviser instead emphasized benefits of the bill.

Inflation is not the issue here—the Fed offsets the impact of fiscal stimulus. The real problem is the debt time bomb. Our political system no longer has “grown-ups in the room”, and thus our fiscal policy increasingly resembles that of a banana republic:

At the very least, the tax negotiations underscore that lawmakers remain a long way from entering an era of austerity even amid warnings from ratings firms and investors that the US fiscal trajectory is unsustainable.

After WWII, our public debt to GDP ratio fell sharply. That occurred due to a combination of small budget deficits and fast rising nominal GDP. Over the past three years, NGDP has again risen rapidly, but this time we no longer have the small budget deficits. Even worse, NGDP growth is set to slow sharply as part of the Fed’s anti-inflation program. If this happens, the debt ratio will begin rising again:

Even permanently high inflation would only be a temporary expedient, as it would eventually feed into higher nominal interest rates due to the Fisher effect. (In addition, it’s recently become clear that inflation is extremely unpopular with the general public.)

The only long run solution is some combination of higher taxes and lower spending. The longer we wait, the more painful the adjustment. I don’t see any major candidate addressing these issues, and thus it’s reasonable to assume that things will get much worse before the problems are addressed.

READER COMMENTS

Jim Glass

Jan 22 2024 at 3:52am

It’s even much worse than that, as I have stated when this subject has come up in the past, and will continue to repeat in the future. The Treasury itself says so. Quoting myself from a few months ago…

What’s $70 billion total on top of $4.2 trillion for just one year? Bah, hardly nuthin’.

Who says the two parties can’t work together happily when they see an interest to do so?

What’s interesting is how the journalists of all stripes go along with them. Even the few who claim to be shocked, shocked by the commonly cited debt number never, ever cite the hugely larger annual accrued number above. It’s not like it is from some hack partisan source. It’s from the Treasury!

Matthias

Jan 22 2024 at 7:10am

I wonder if this will trigger eventual dethroning of the USD as the reserve currency.

None of the options for eventually resolving the issue are pretty, and the impact will get worse as they are kicking the can down the road.

If it happens, it will likely still take a long time. Especially as there’s no obvious single replacement candidate. Though perhaps we might get a more multipolar financial world.

Jose Pablo

Jan 22 2024 at 8:23pm

this will trigger eventual dethroning of the USD as the reserve currency

to use what instead?

The Euro area debt to GDP is above 90% similar ballpark to the US’

Japan debt to GDP ratio is around 220%

This is not an American problem this is a “democracies” problem.

And the USD is the reserve currency because there is a huge amount of assets denominated in USD. And ever-increasing amount of US government debt increases, not reduces, this advantage.

JP

Jan 22 2024 at 7:23am

Scott, what is your opinion of the policy itself, debt not included?

Scott Sumner

Jan 22 2024 at 12:31pm

There are many policies in this bill, and I’m not well informed on all of the details. In general, I prefer a simpler system with lower rates and fewer deductions/credits. I also prefer a consumption tax over an income tax. My views on tax changes depend on how they are financed. Any tax reduction is going to look good if you ignore the cost.

SK

Jan 22 2024 at 7:59am

Scott, what rate to you is permanently high inflation? The US growing debt burden, I have labelled a “Debt Trap” which we entered some time ago and yet for now capital markets seem all too accommodating and not yep penalizing the US. And all across the globe, debt levels seem to be elevated vs historical metrics and again markets seem to be accommodative of debt issuance. The US in a growing debt world might appear to be in a bad situation, but relatively vs other nations with elevated debt, for now, not so bad. Yes, the day of reckoning will be coming, but for now hard to see when that will be the case.

Scott Sumner

Jan 22 2024 at 12:32pm

Something above 2%.

Thomas L Hutcheson

Jan 22 2024 at 8:56am

Democrats are not deficit angels, but at least they never passed three bill (Reagan, GWB and Ryan-Trump that cut tax revenue and added to the deficit. And in negotiations, Democrat’s have been open to some spending reductions but Republicans never been to any tax increases.

Jim Glass

Jan 22 2024 at 8:04pm

Rethink your take on Reagan. He passed one big tax cut early, then several smaller tax increases later to ameliorate the deficit that had grown really big (by the standards of then, not now) largely due to his military spending.

He also passed the Social Security tax increase and benefit cut to “save” SS a couple days before it went broke. And the big “Reagan Tax Cut” he is famous for (the Tax Reform Act of 1986) was revenue neutral across all income levels by design — and in fact *increased* the amount of tax actually paid by the very richest (top 1% etc.) to more than that paid by any other group for the first time in the recorded data.

The “tax cut” in TRA 1986 was not a reduction of taxes collected, but of tax rates, with the highest going down to 28%. It remained revenue neutral by also slashing tax breaks that were overwhelmingly used by the rich. When Reagan took office the top tax bracket rate was 70% — liberals who fantasize that anybody ever paid that rate love to oooh and ahhh over how great that was. But nobody paid it. There was a massive tax shelter industry back then that everybody with top-level income (actors, celebrities, business people, politicians, sports stars) used to escape tax. (I was a young lawyer then and received a lot of very nice free meals from shelter salespeople.) TRA 1986 destroyed the shelter industry. Thus the very richest, with no shelters to use but only a 28% rate to pay, started reporting all their income straight up and paying the tax on it.

Note that the “Reagan tax bills” is a misnomer, they all were bipartisan bills as the Democrats had control of the House. TRA 1986 was passed by overwhelming majorities of both parties in both House and Senate. Both parties got what they wanted: Repubs got lower tax rates and Dems got to slaughter tax loopholes for the rich. And economists were joyous because lower rates plus the death of the shelter industry made the tax system much more efficient, imposing much less deadweight cost on the economy.

It was a huge success on all counts, and was copied by countries around the world for a generation. A testament to how the parties once upon a time could work together for the greater good. Once upon a time… Once upon a time…

So be careful what you say about Reagan and taxes.

Jose Pablo

Jan 22 2024 at 8:55pm

Politicians are “socialist of all parties” we were warned of that 80 years ago.

The incentives that they (all of them from all parties) have, can only lead to overspending and under taxing (for a given level of expending). We also know that since, at least, the 60s. This insight was even rewarded with a Nobel price.

Same old, same old.

steve

Jan 22 2024 at 10:06am

This isn’t about the economy so much as it is about electoral politics. Cutting taxes while increasing spending, leading to debt, is very popular. It has been the cornerstone of GOP politics since Reagan. The Democrats used to be spend and tax, at least theoretically sustainable but it looks like they plan to join the GOP with this bit of electoral bribery. So you are right, things got worse.

Steve

johnson85

Jan 22 2024 at 10:53am

You’re giving democrats too much credit. They advocate for taxes, but even when they have had full control, they do some symbolic stuff to “the rich” but don’t do much else. Flip side of Republicans claiming they are going to cut spending, and then at best they do some symbolic cuts to “discretionary” spending, and even then they only do that if they don’t have the presidency.

We either have to slow “entitlement” spending or raise taxes on the middle class. We’re not going to have the political will to do either unless and until there is a crisis.

steve

Jan 22 2024 at 3:22pm

Agreed. It’s why I said theoretically. Occasionally the funding they build into a program pays for the new program but often, probably most fo the time it does not. Just gets added to the debt so from the public POV it’s free stuff they dont have to pay for.

Steve

Scott Sumner

Jan 22 2024 at 12:34pm

Everyone, It’s too glib to suggest that this is just politics as usual. Things have gotten much worse since the late 2010s—we are in uncharted territory.

Jose Pablo

Jan 22 2024 at 9:17pm

We have been in “uncharted territory” for quite a long time. It seems that we keep “charting” new territory while “sailing” through it.

In 1992 debt to GDP ratios above 60% were considered “uncharted” enough for the European countries signing the Maastricht Treaty.

In 2010, Reinhart and Rogoff were still considered 60% significant and 90% definitely “uncharted”. We have been sailing the uncharted 90% (if properly accounted for as Jim rightly suggests) for quite a long time.

Japanese sailors seem to know a thing or two about “uncharted territories”.

I don’t know …

Warren Platts

Jan 22 2024 at 1:26pm

Well, we are currently importing $4 trillion dollars worth of goods every year. Maybe we should consider a revenue-raising tariff. A 25% tariff on all imports could potentially cut the budget deficit in half. I’m not hanging my hat on 25%; presumably there is an optimal tariff that would maximize revenue. Maybe that’s less than 25% or maybe even more. That’s a job for you economists to figure out..

Yes, this would make every trading partner in the world mad at us; but we just have to explain that we gotta do something to get our fiscal house in order. As for deadweight losses, they’re probably a lot less than would be the case for corporate or personal income taxes that raised a similar amount of revenue..

Scott Sumner

Jan 23 2024 at 12:28am

Wouldn’t a VAT be far better than an import tariff?

Warren Platts

Jan 23 2024 at 4:21am

I’ve given considerable thought to this. In principle, a VAT does not provide protection for home import-competing producers. But for that very reason, VATs actually generate better terms of trade gains than do tariffs! Thus, from a selfish perspective, if we want to balance the budget with as much foreign tax revenue as possible, a VAT would work better than a tariff.

Vivian Darkbloom

Jan 23 2024 at 8:38am

“In principle, a VAT does not provide protection for home import-competing producers. ”

This is often stated, most notably by Mankiw. However, the “in principle” has to be considered in light of overall tax policy and not just the VAT in isolation.

The consumer bears the same amount of VAT on imported goods as on domestically produced goods. Thus, a VAT shouldn’t raise any problems under existing trade agreements. However, raising considerable revenue through a VAT should allow a reduction (or at the very least not a raise) in other taxes that *are not* neutral. This would include corporate income tax and taxes on domestic labor. A reduction in the rate of tax on the latter vis a vis competing importers is *not* trade neutral.

Warren Platts

Jan 23 2024 at 3:45pm

Heh! Why do you think every country that got rid of most of their tariffs in order to fit into the WTO system instituted VATs instead? Mexico never had a VAT until right after NAFTA. 😀

Scott Sumner

Jan 24 2024 at 11:48pm

“Foreign tax revenue”? Good luck with that!

Michael Sandifer

Jan 22 2024 at 6:46pm

Yes, we’re in uncharted territory for the US, but it’s not surprising to me. I have long expected that the deficits and debt would rise as baby boomers retire, because most Americans do not want to make compromises. This is a voter problem, just as is the rise of fascism, and it may be too late to try to turn the tide at this point. That said, no one should stop trying to do so.

Jose Pablo

Jan 22 2024 at 8:44pm

The only long run solution is some combination of higher taxes and lower spending ..

you should add

... while allowing the politician/s adopting the solution to win the next election

This necessary condition significantly reduces the actual solution space.

The debt problem is not just “American”; it happens to a similar (or worse, look Japan) extend in every mayor democracy. In fact, you can predict that in democracies it is always a matter of time before entitlement expending (used to “buy” votes) outpaces tax income (that will only be popular on a very narrow base of voters)

And so is happening all over the world! Politicians (we were warned that they are “socialist of all parties”) have progressively discovered that they could use deficits to win votes without real consequences.

This cannot be “unlearned” by election winning politicians. At least in the absence of much more serious consequences. Serious consequences that we have not seen even in Japan.

You are just being a party pooper. Earth will be grilled by Global Warming before any consequential ratio of debt to GDP is reached in the US.

Gary Marshall

Jan 23 2024 at 1:04am

Hello Mr. Sumner,

I was reading your article Just When You Thought …

You should note that Inflation soared throughout the late 60s and 70s as Public Debt to GDP dropped, and declined through the 80’s as Public Debt to GDP soared. Something is wrong with your analysis.

The official Deficit and, thus, Public Debt is not the problem many think it is.

Let us say that the US Federal Gov’t spends $5 trillion annually. $4 trillion taxed and $1 trillion borrowed. I ask what the deficit is? The conventional answer would be $1 trillion. I ask again, “How much did the government contribute to its expenditures?” The answer must be nothing for obvious reasons.

Simply, the government has no money, or rather resources. Whatever it spends comes from taxpayers or lenders, the latter with the presumption that taxpayers shall settle incurred debts. Therefore, all public expenditures are deficit or debt financed if you will, unaccounted as they are. There is a taxed portion to the deficit and a borrowed portion to the deficit, but its all deficit. Thus, government can never escape a deficit.

Resident citizens, and, specifically, their combined assets, property, and incomes fund government, all of it. And it is this aggregate that one must examine in order to arrive at truth in Public Finance, not the finances of an entity that has no funds or resources.

When done, one quickly discovers that it makes no difference whether a community has its government tax or borrow from that aggregate, but only on a superficial basis; For taxing is not the same as borrowing.

Many economists, because of this ceaseless blunder, make declarations and concoct theories for which they have little or no basis. They believe that the Fed can cause or control inflation. They believe public expenditures, about 80% of which go to waste, funded by Public Borrowing are a curse while those funded by Taxation are benign. Waste is waste regardless of the source of funds.

I do agree with many of the things that free market economists argue for or against, but on this fundamental and broad issue they are completely wrong.

I have offered to debate the Mises people, Cato members, AIER’s experts, etc, but they all refuse to engage. They must know they are wrong, but they won’t part with any element of their cherished theories.

Perhaps you are not yet bound to aged conventions.

Here is a link to an article of mine at Real Clear Markets. It should have been titled, An End of Tyranny, but editors.

https://www.realclearmarkets.com/articles/2021/03/31/a_case_for_government_as_a_borrower_to_end_tyranny_770572.html

The problem in economics is not one of money, although that is important sometimes. It is fundamentally a question of resources and how they are employed. Many economists are errantly lost in questions of money. Were they to look at resources they would gain a far better understanding of what is going on.

Let me know if you’re interested in a different view of things.

Regards,

Gary Marshall

Jose Pablo

Jan 23 2024 at 11:43am

I tend to sympathize with your argument, and I do believe that something is fundamentally wrong in the way we normally look at taxation and spending.

But I don’t quite get your system. Appreciate if you could clarify:

How is the debt incurred by the government going to be paid back?

In order to “chain” the government (and I couldn’t support more this objective!) the best term for this debt will be “demand deposits”. The lenders will have the right to withdraw their funds at any time. A government facing the permanent risk of a run certainly makes me salivate with pleasure but, is that what you are suggesting?

It is clear that the whole (private) wealth of a nation “backs up” government debt. The government can confiscate at any time any amount of wealth. But it doesn’t need to do so as far as their lenders rest assured that it has the capacity to do so. Debt is always about credibility. And the government shouldn’t tax even one dollar in excess of the amount required to assure its lenders that they will, eventually, be paid. But I am not sure that the minimum amount of confiscation required by the lenders to remain “confident” would go all the way to zero.

Jim Glass

Jan 23 2024 at 9:04pm

Hello Gary: I always try to keep my mind open to new ideas, so I looked at your web site’s presentation in favor of the massive advantage of $0-taxation, 100% debt financing for government…

No. It is the amount of the expenditure in future taxes collected, period. Say the expenditure and borrowing are both $100X. The govt must pay annual debt service, interest, on the borrowing. Say the interest rate is 5%. This annual interest payment is financed by taxes. Thus the govt must collect $5X in taxes annually to service the debt. If the debt is never paid off but rolled over perpetually, the result is an endless stream of annual $5x tax collections — which discounted to current value equals, by amazing coincidence, exactly $100X in taxes. (Go figure. An expenditure of $100X requires $100X of cash collected to pay for it! Who knew?)

As $100X = $100X, the only difference is the timing of the tax collection. Debt finance produces current cost deferral but future cost growth. This year the $100X annual expenditure is financed with $5X of tax. In year 24 the annual $100 expenditure is financed with $120X of tax. Although if this really is the national budget, things will have … *changed* … long before then. See projections for USA circa 2040. That ain’t gonna happen as projected.

Tell that to Louis XVI. Who learned that his taxpayers didn’t want to pay $120X francs in debt service to pay for $100X francs of government.I make modest additions in bold below…

You can keep the $10,000. My contribution to Canadian relations. But please, don’t say you’d avoid collecting any tax for debt service by just adding the interest on top of the debt, never paying any tax-financed cash interest, such as…

Lenders to govts really, really insist on receiving cash interest on the bonds that they receive in return. That cash flow to them is what gives the bonds their value. When the tax-financed backing of the bonds becomes uncertain or fails, the bonds drop in value towards zero. That impoverishes and saddens the “community”, and makes the lenders angry.

In the $100X annual expenditure, 5% interest illustration above, after 24 years just the annual interest is $223X and rocketing upward via compounding. You are telling lenders they’ll never receive even a penny cash for any of it, just more balance sheet entries forever. And they are putting up a guillotine in the town square.

Jose Pablo

Jan 23 2024 at 10:06pm

Jim,

noninterest expending has outpaced revenue collected on 37 of the last 50 years. And in any single year for the last 20.

So, paying interest by raising new debt can be considered by now a well stablished “tradition” of the US government.

If any debtholder thinks / expects their interest payment are going to be paid out of tax revenue, he/she should be either immune to reality or held in isolation in a remote island.

Why do we keep using a “mental model” that has no connection whatsoever with reality when talking about public debt?

Jose Pablo

Jan 23 2024 at 10:41pm

No. It is the amount of the expenditure in future taxes collected, period. Say the expenditure and borrowing are both $100X. The govt must pay annual debt service, interest, on the borrowing.

The govt doesn’t pay the annual debt service, the citizens will pay that.

But the cost of the debt service for the citizens would be precisely equal to the “opportunity cost” of the tax raised to finance the initial $100.

For the “community of citizens” the cost of financing government expending thru debt (in this case the interest payments for the term of the debt) is exactly the same cost of financing government thru taxes (in this case the opportunity cost during the term of the debt of the taxes collected in time = 0)

Jose Pablo

Jan 23 2024 at 11:19pm

You are telling lenders they’ll never receive even a penny cash for any of it, just more balance sheet entries forever.

No. You are telling lenders that they will be fully repaid (if they wish so) because the government will borrow money from other people.

And they should be very aware by now that this is what the government intends to do. In fact, they are. Nobody is hiding this reality from them.

They just seem to think that the cash raised through future debt is as good for them as the cash raised through future taxes. Afterall, this is what has been happening for quite a long time (and everybody is forecasting it to keep happening for another quite long time) and they are not putting any guillotine in any square.

https://www.pgpf.org/blog/2023/06/what-is-the-primary-deficit

Maybe your definition of “forever” is “for more than 50 years”. In this case you still have a chance of being right at some point in the future. And also, it could be that the fact that they accept being repaid with “the new lenders money left after financing with new debt the current primary deficit” doesn’t mean that they are going to accept being repaid with “the new lenders money left after financing with new debt the whole government budget“.

But I would give, at least, careful consideration to the possibility of the debt holders being right in their apparent indifference to being repaid by either future taxes or future additional debt. Afterall both are totally equivalent / have the same “cost of carry” (well, debt is better since the cost of managing this way of funding the government is wayyy lower)

Jim Glass

Jan 25 2024 at 1:03am

Nope. He is saying lenders will never receive cash interest on the debt, the interest will just compound on it: “Many will argue that the debt carries interest and the lender must be repaid. Correct. However … Let us say the government allots interest on the public debt, say $10 on the $100 debt. The interest increases the public debt … by $10 to $110… “

But, alas, it is not what the government intends that rules, but what the “other people” decide.

When Louis XVI went broke on debt incurred to finance the American Revolution (“Merci, Ben Franklin”) he did of course ask other people to lend him more francs to carry over. They replied, “Non! You can’t pay the interest on the debt you owe us now. How stupid do you think we are?” … When Russia defaulted in 1998 because its tax revenue couldn’t cover its debt service, the Kremlin asked the other people for more rubles but they said “Nyet! ” … When Sri Lanka recently explicitly embraced MMT principles to borrow without end or tax revenue because, hey, what could go wrong? … what went wrong?

Nope. Gary is very clear that the lenders aren’t getting any cash. Period. He gives numerical examples. That’s the entire wonderful benefit from his program: “the community” gets the gains from expenditures without being drained of the cash cost of financing them.

You are the person saying that in the future “they will be fully repaid (if they wish so)”. OK, let’s see how that works…

In the 5% example I gave above we follow Gary’s model until, after only 15 years, the investors decide they wish to be fully repaid, as per you. Annual debt service then is 108% of the total cost of govt. A good deal? Hey, after Gary’s “zero taxes” start, that’s taxes a plenty!… or after 23 years, >200%, twice the cost of govt … or after 35 years, >4.5 times the cost of gov’t, >100% of GDP — and just what “other people” are going to pay that??? 🙂

Where? The USA has paid 100 cents cash interest on each dollar of its debt service since 1789. Its debt service cost was 2.5% of GDP in 2023 — with taxes paying 75% of debt service over the last 10 years (deficits = 25% of spending).

Name for us any country, kingdom, empire in all history, that followed the “Gary model” of financing itself: All borrowing, no tax.

Which brings up a point. All the kings, emperors, finance ministers, chancellors, treasury secretaries et.al., of all history would have loved to reap the great proclaimed benefits from using Gary’s proposal. Yet none did. On his web site he calls all the world’s economists “babbling children”, and much worse, for not seeing the self-evident huge benefits of his plan — but he is equally slurring all the government leaders of all history.

It follows that either: (A) Gary is correct and all the national leaders of all history plus all the worlds’ economists have been “babbling children” and worse forever; or (B) Gary is wrong and all the national leaders of all history plus the economists have been, you know, correct. Occam’s Razor: Your choice is… ?

Good question! You tell me.

Jose Pablo

Jan 25 2024 at 9:31pm

Name for us any country, kingdom, empire in all history, that followed the “Gary model” of financing itself: All borrowing, no tax.

Jim, the US (and many other countries, Japan as the “best” example) has been moving in that direction, little by little, for the last 50 years: tax covers a diminishing amount of their expenditures … and it is working pretty well so far!

Japan has had a primary deficit since WWII except for 5 years (1986-1991). And the projections for the years to come are for the primary deficit to double. No investor in Japanese debt, and they are aplenty, expects his debt or interest being repaid out of taxes. The only hope they have is that the Japanese government can find other “suckers” that, basically, send the “old investors” their money’.

All the governments are moving in the direction of “Gary’s model” and it’s working. Maybe the reason why it is working is because, you know, it works!

Jose Pablo

Jan 25 2024 at 9:43pm

Jim, I am really sorry for the “brick” that follows. I am about to abuse your patience big time. Please read what follows mercyfully, it is dense and badly written. Hope you can follow the idea despite that. Sorry again.

Now, don’t call this security I am about to describe “debt” (that’s a mental trap), call it, for the sake of the argument, “TUSWBS” (Total US Wealth Backed Securities). This TUSWBS works as follows:

* the US government issues TUSWBS which are legal claims over a part of the “collective wealth of the nation” (term to be defined by the lawyers on the prospectus), equivalent to the principal of the security in nominal US$. The TUSWBS pay a fixed amount of dollars per year and pay back the principal at the end of a fixed term.

* all American citizens are the underwriters of the TUSWBS issued by the government. They hold the risk of the issuer non fulfilling their obligations with the TUSWBS investors.

* The US government issues TUSWBS every year in the amount required to finance their expenditures. The issuer makes clear that it intends to fulfill its obligations with TUSWBS investors, only by issuing more TUSWBS. If this mechanism fails then, and only then, the government will force the “underwriters” (the citizens) to fulfill their contractual collective obligations with the investors by confiscating part of their collective wealth.

The buyers of TUSWBS, when evaluating the attractiveness of the investment, should look at:

a) the ratio (KR, Key Ratio) between the collective wealth of the nation and the amount of outstanding TUSWBS. The part of this collective wealth collected by the government through taxes in a particular year is irrelevant. It does not improve the KR (it, very likely, makes it worse)

and, maybe,

b) the ability of the government to force the underwriters to fulfill these legal obligations in the very unlikely case that it is required to do so.

Now, the “collective wealth” of the country is by no means decreased if the government expends 5% of GDP or 50% of GDP (including annual interest payments) AS FAR AS the money is spent in ways that increase the “collective wealth” by more than the principal raised.

If the government expends $100 (raised through TUSWBS and including interest payments) creating $110 of “collective wealth” the KR improves, making TUSWBS more (not less) attractive.

Now, whether the government collects 5% or 50% (or 0%) of GDP through taxes is irrelevant for the KR, AS FAR AS the government creates, with the amount raised thru taxes, the same wealth that would have been created if the money have remained in the pockets of the underwriters. If the government creates, with taxes, less collective wealth than the citizens would have done with the uncollected taxes, then, raising more taxes makes the KR worse (not better!) and the TUSWBS less attractive.

The ability to collect taxes could have some influence on b), the “credibility” of the underwriting obligation of the citizens. But once this mechanism is fully understood, I am sure that more specific and effective ways of improving this credibility could be designed.

My point is that “actual US government debt” is closer to this TUSWBS security than to “private debt” and that the name “debt” obscures the true nature of government “debt” (you are right, it has been doing so for centuries!) and makes us look the wrong way at the influence of taxes and expending in the attractiveness of TUSWBS.

Under the “TUSWBS framework” the ratio between what the government expends and what it collects through taxes is utterly and totally irrelevant. What is relevant is:

a) whether or not the money raised by issuing TUSWBS and expended by the government increases more than 1:1 the wealth of the nation. If the government expenditures destroy value the KR decreases and, eventually, the whole TUSWBS mechanism collapses.

b) whether or not the money left in the pockets of the underwriters as uncollected taxes, creates more value than the interest paid by the government on TUSWBS. If it creates more value the KR improves by non-collecting taxes, making this security more (not less) attractive!

I can’t help but think that these two things SHOULD be the relevant ones (they do “sound” like the relevant ones!) for the TUSWBS investors, and that we are focusing (yes, even very brilliant minds, you are also right on that!) on an irrelevant ratio like the “annual deficit.”

Calling government bonds “debt” (like in “private debt”) leads us to this mistake. What the US government is issuing is closer to TUSWBS and investors should be realizing little by little that this is the case and focusing on the right ratios.

Jim Glass

Jan 26 2024 at 12:55am

Pablo, name one government that doesn’t collect taxes to pay interest on its bonds. For extra credit, name one *other* government that has seen the tax backing of its bonds fail and the bonds go unserviced without very bad result.

Here is Gary’s explanation on his web site for how his government bonds will meet their payment obligations to lenders with no taxes ever collected to service them…

So an amount is borrowed incurring an obligation to repay it plus interest. But that amount is spent, gone — and there is no source of revenue to use to repay it or pay the interest. So we borrow another amount to use to do so, incurring more interest (remember the compound growth in my 5% example), and then we borrow again to repay that and incur more interest, and then …

This model of financing is familiar, actually well known, there’s a name for it … Ponzi Scheme.

Your TUSWBS seem very much the same, with the exception of being backed by “all American citizens [being] the underwriters of the TUSWBS issued by the government. They hold the risk of the issuer non fulfilling their obligations” When the Ponzi Scheme fails and the US Marshalls start working their way through Texas, Oklahoma and Montana to collect on that backing from the citizenry there, who never individually agreed to underwrite anything … I dunno, that citizenry owns guns.

Beyond that I can’t say anything. I can’t analyze hypothetical financial systems, real ones are too tough for me. If you think you are going to attract investors away from AAA corporate bonds and tax-backed sovereign debt to the likes of this … maybe start small, get a town to try it out. There have been communities that issued their own money, like Ithaca Hours. I guess one could have its own local central bank to manage its finances too.

Don’t apologize to me for “bricks”, as to walls of text, I’m the worst offender.

Jose Pablo

Jan 26 2024 at 11:06pm

Pablo, name one government that doesn’t collect taxes to pay interest on its bonds

Japan, USA, Italy, Spain, France … every country in the world running a primary deficit is doing that!

A primary deficit means that governments don’t collect enough taxes to pay for their expenditures, much less to pay for interest or repay the maturing debt!

So you can very well say that interest payments are made with the money raised by issuing new debt. If the government were unable to raise additional debt, interest payments will have to stop, maturing debt will not be honored, the government expenditures will have to be cut by around 5% and the government will have to send US Marshalls to collect taxes from gun owning citizens exactly like with TUSWBS. No difference. Your “collecting taxes goverment” also depends to a significant extend on raising new debt on a daily basis. And lenders keep lending money to governments at negative real interest rates.

This model of financing is familiar, actually well known, there’s a name for it … Ponzi Scheme

No, has nothing to do with a Ponzi scheme. The problem with government debt is only in the way we look at it. And the problem of compound interest you see doesn’t exist.

Imagine we live in a country with a balanced budget. Taxes = expenditures. And, in that very imaginary country, there is a lender willing to lend every citizen an amount of money equivalent to the taxes he/she has to send to the government in year 1. This money is inmediately send to the government.

So, now, instead of having some less cash after paying “taxes”, the “taxpayer” keeps his tax money and has an equivalent liability. The taxpayer is in the same “financial shape” as if it have sent his tax money to the government. Of course, he has to pay interest in his liability!, but he has an “additional” asset in his balance sheet (the money not sent to the government) that will earn a return with which to pay interests.

In year 2 the taxpayer repeats the trick. His liability has doubled now, but he has two years’ worth of taxes as an additional asset, generating a return to pay interest with. He is in the same sound financial position (or better if he has invested his tax money with a return higher than the interest rate on the debt)

He can repeat this trick forever and his financial position does not deteriorate (for every additional annual loan he has an equivalent additional asset). If at any point the lender want his money back (what for?). The money is there, in the taxpayer balance sheet.

From a financial stand point this is totally equivalent to financing the government only through debt. And it is sound. Has nothing to do with a Ponzi scheme.

Matt Mc

Jan 24 2024 at 8:49pm

Scott,

You stated: “Fed offsets the impact of fiscal stimulus.”

The Federal Reserve raising interest rates, coupled with substantial levels of debt and deficits, results in an escalation of interest expenses. This, in turn, contributes to increased interest payments circulating within the economy. While not constituting direct spending, it nevertheless seems to be a form of fiscal stimulus.

Andy Weintraub

Jan 25 2024 at 9:30pm

The question in my mind is: what’s the “optimal” size of the debt the government can carry?

There’s so much talk about eliminating the debt, but I don’t think that’s necessary or desirable. It just has to be manageable.

Jim Glass

Jan 26 2024 at 1:06am

This is off topic except as to the idea in the title.

Never believe things can’t get worse.

This fascinating and entertaining true life story explains Russia’s unofficial national motto…

The Russian 2nd Pacific Squadron – Voyage of the Damned

“And then things got worse…”

Jim Glass

Jan 28 2024 at 5:58pm

When Does Federal Debt Reach Unsustainable Levels?— Penn-Wharton Budget Model

Jose Pablo

Jan 28 2024 at 11:21pm

Facts:

National US Debt 34 tr

https://fiscaldata.treasury.gov/americas-finance-guide/national-debt/

National US Net Wealth 140 tr

https://en.wikipedia.org/wiki/List_of_countries_by_total_wealth

Why the Penn-Wharton Model considers that a Net Wealth of 106 tr (assuming the worst case scenario that the 34 is not included in the US Net wealth calculation) is “unsustainable” is a mystery to me

Now, imagine that the National US Debt doubles in one year to 68 tr and that all this debt is bought by American nationals. Now the National US Debt is 68 tr but the US Net Wealth is 178 tr (140 tr + 34 tr of additional debt, any liability is an asset to somebody else), so still (at least) 106 tr of net wealth after “government” debt, and equally sustainable.

Imagine you ask for a loan in your children’s name and that you have the capacity to tap your children’s credit accounts at will. The outstanding loan is $34 and there is $140 in your children’s accounts. Is the $34 loan unsustainable because you have chosen, your decision, to draw from your children’s account only $4.4* a year? I don’t think so. Particularly so if you are borrowing a significant part of this $34 from those very same children’s accounts.

* 4.4 tr was the total revenue collected by the Federal Government in 2023

It could be that what is “politically unsustainable” is drawing more annually from your children’s account. But that is, by no means, a meaningful financial consideration. Your lack of guts to draw more money from your children’s accounts says nothing of the financial soundness of the whole scheme.

Jose Pablo

Jan 29 2024 at 12:08am

Even more surprising: the national US debt should be more sustainable the bigger it is!!

If it were now 68 tr instead of the actual 34 tr it would be even more sustainable. Why?, because the US will be an even richer country.

It is a clear example of Bastiat’s what is seen (the accumulated deficits aka national debt) and what is not seen (the returns that American taxpayers have gotten on the taxes they never paid “on time”, aka the accumulated deficits aka national debt).

For the simplicity of this argument, let’s assume that all the national debt is lend to the American Government by foreigners.

Scenario 1: through the years, the government has collected 30 tr less in taxes than the money it has spent (the actual scenario).

Scenario 2. through the years, the government has collected 60 tr less in taxes than the money spent. The additional 30 tr from scenario 1 has been borrowed from abroad.

a) In the scenario 2 an additional 30 tr has been left in the pockets of the American taxpayers.

b) Let’s assume that they have, collectively, invested this money with real returns above the average real interest rate paid on the sovereign debt. So, this 30 tr has been turned into 60 tr. I am totally making up the number. It would be the summatory of the annual deficits of each year compounded at the rate of return that the taxpayers have got on the money they have kept as “unpaid taxes” (aka the “annual deficit”)

c) Let’s assume that the borrowed 30 tr has turned into a liability of 50 tr once the accumulated interests on the debt are taken into account. I am again making up the figure, but it should be less than the previous 60 as a result of the hypothesis that Americans have invested the “never paid taxes” at a rate of return about the cost of debt.

d) That means that in scenario 2, American taxpayers can payback their 50 tr liability and still be 10 tr better off that in scenario 1

Corollary: If the government can borrow from abroad at interest rates below the return than taxpayers can get on their never paid tax dollars (aka the accumulated deficit, aka national debt), the government borrowing as much % of the expenditures as it can, makes Americans richer. And because of that they would be in a better (not worse) position to pay back all the accumulated debt.

Comments are closed.