To understand how monetary policy went off course, it might help to look at Lael Brainard’s recent speech on monetary policy. Here is an excerpt:

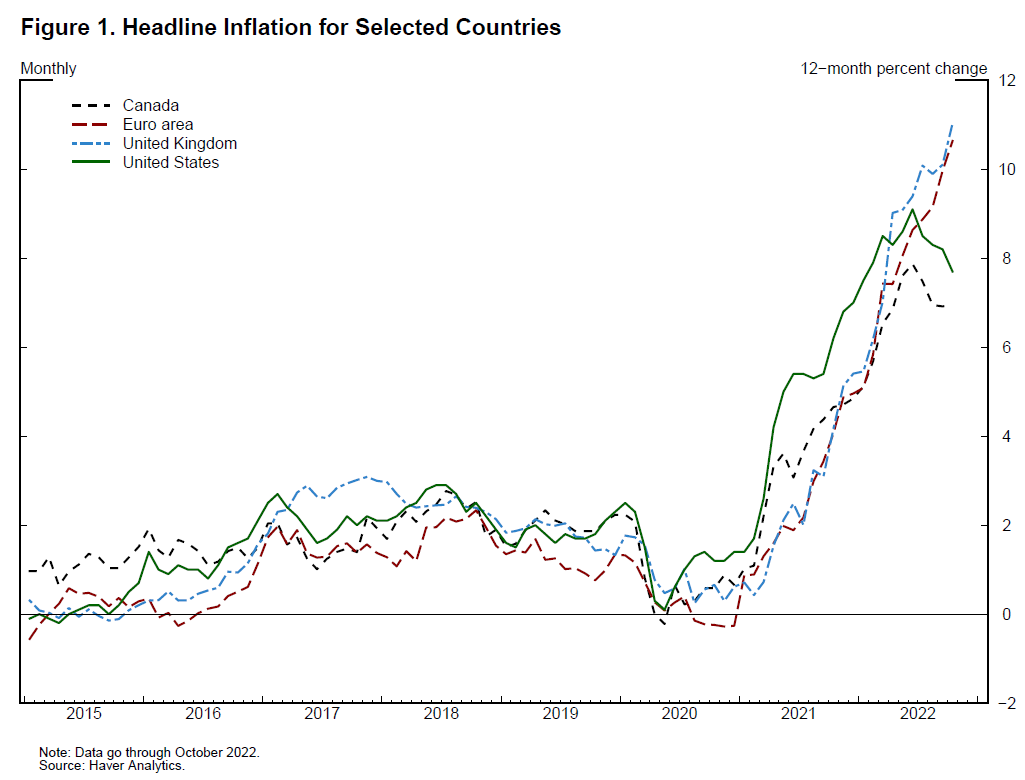

Inflation in the United States and many countries around the world is very high (figure 1). While both demand and supply are contributing to high inflation, it is the relative inelasticity of supply in key sectors that most clearly distinguishes the pandemic- and war-affected period of the past three years from the preceding 30 years of the Great Moderation. Interestingly, inflation is broadly higher throughout much of the global economy, and even jurisdictions that began raising rates forcefully in 2021 have not stemmed the global inflationary tide.

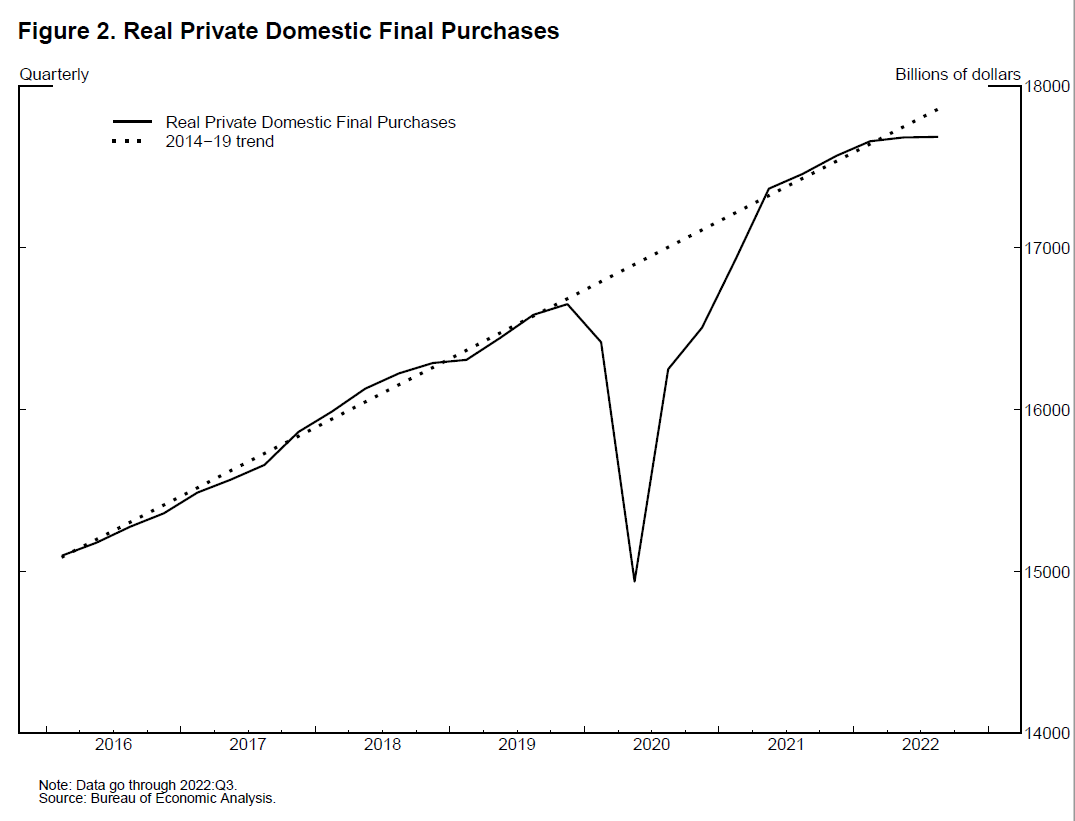

In the United States, as a result of significant fiscal and monetary support, the level of private domestic final purchases recovered extremely rapidly in 2020 and 2021 to levels consistent with the pre-pandemic trend before moving below trend in 2022 (figure 2). Although demand came in near the pre-pandemic trend on an aggregate level, the pandemic induced a shift in composition that concentrated large increases in demand in certain sectors where the supply response was constrained.

{kind=link}

{kind=link}

To keep inflation at 2%, the Fed needs to keep growth in demand at roughly 3.5%/year in the long run. Since 2019, nominal demand has risen by a total of about 8% more than the growth rate consistent with the Fed’s 2% inflation target, and PCE inflation has also overshot its target by roughly 8% over the past three years. Thus almost all of the excess inflation is demand side.

So how does Brainard reach the opposite conclusion? She links to a figure showing growth in real spending, which she uses as an indicator of aggregate demand. It isn’t. It is nominal spending that represents demand, not real spending. In 2008, Zimbabwe saw an astronomical increase in nominal spending, even as real GDP declined. By Brainard’s criterion, there was no problem with excess demand in Zimbabwe, as real spending was falling at the time.

It isn’t just Brainard; I’ve seen many other economists confuse nominal and real spending. Real spending reflects the interaction of supply and demand shocks and is an unreliable indicator of whether there is excess demand in the economy. A positive supply shock will boost real spending without impacting the aggregate demand curve at all. It’s the macroeconomic equivalent of conflating oil consumption and oil demand.

Brainard discusses the fact that central bankers traditionally tried to look past energy supply shocks, assuming that their effects on inflation were transitory. She then suggests:

Although these tenets of monetary policy sound relatively straightforward in theory, they are challenging to assess and implement in practice. It is difficult to assess potential output and the output gap in real time, as has been extensively documented by research.

This is correct and is the reason why the Fed should completely ignore the output gap. Instead, policymakers should focus like a laser on promoting slow and steady growth in nominal spending. If they do so, the economy will stay relatively close to its natural rate. But they should not try to figure out the natural rate of output, which (as Brainard rightly suggests) is impossible to determine in real time.

So what causes so many respected economists to conflate real spending and “demand”? I blame Phillips Curve models, particularly the view that causation runs from strong real economic growth to high inflation.

Milton Friedman had a much better interpretation. Positive nominal shocks have real effects in the short run, which explains the negative relationship between inflation and unemployment seen in the Phillips Curve. Output adjusts in the long run, and the economy goes back to the natural rate, even if inflation remains elevated. In that case, the observation that real output is near the natural rate tells us next to nothing about whether the economy has experienced excess demand.

PS. Brainard’s graph refers to “real final sales”, not real GDP. But while those two variables are slightly different in an open economy, Neither variable measures anything close to “demand”. The slight difference between the two in no way changes the conclusion that only nominal variables can adequately measure aggregate demand conditions.

READER COMMENTS

David Henderson

Dec 1 2022 at 4:59pm

Excellent post!

“In 2008, Zimbabwe saw an astronomical increase in nominal spending, even as real GDP declined. By Brainard’s criterion, there was no problem with excess demand in Zimbabwe, as real spending was falling at the time.”

Great reduction ad absurdum.

AN

Dec 1 2022 at 5:22pm

An increase in the real demand for consumption goods (in all future periods of time) without an expansion of the aggregate consumption/production possibility frontier (i.e. you have not discovered a treasure trove of goods or started receiving tribute from abroad) is deflationary for a given a NGDP level path, right?

Increased real demand for consumption goods presumably makes people increase their labor supply at all wage levels (for it has to be due to a shift in preferences away from leisure and towards the consumption of goods if endowments have not expanded), output goes up and since the NGDP path is unchanged, the price level declines.

Scott Sumner

Dec 2 2022 at 10:48am

There is no such thing as real aggregate demand. It doesn’t exist. It’s a meaningless concept. Aggregate demand is a nominal concept.

Thomas Lee Hutcheson

Dec 1 2022 at 10:36pm

I think yoy mis the point of her chart. It was to say that inflation was not caused by ARA. That is of course true. All inflation is caused by the Fed.I liked the hint that the Fed might need to raise its average flexible rate target and might need to be more flexible as well because economic shocks in an era of less globalization.

Scott Sumner

Dec 2 2022 at 10:46am

No, that is definitely NOT what she is saying. She is claiming that real final sales represent demand, and that demand is back on trend.

Spencer

Dec 2 2022 at 9:46am

The FED’s technical staff was censored during Bernanke’s reign and thereafter. Today’s speeches are not academic, they are political.

…

You can call nominal “final product”, but that’s not equal to AD. N-gDp is a subset of AD. AD = M*Vt.

…

And the monetary transmission mechanism was never entirely via interest rate manipulation until after Powell reduced the reserve requirement ratio to zero percent across all deposit tiers as of March 26, 2020.

…

Economists never knew how the “system” worked. Banks aren’t intermediaries. The FED’s accounting is so screwed up they need audited. Their definitions eliminated the ability to conduct double-entry bookkeeping on a national scale after the 70’s.

…

The FOMC’s monetary policy objectives should be formulated in terms of desired rates-of-change, roc’s, in monetary flows, volume times transaction’s velocity, relative to roc’s in the real-output of final goods and services -> R-gDp.

…

Roc’s in N-gDp, or nominal P*Y, can serve as a proxy figure for roc’s in all physical transactions P*T in American Yale Professor Irving Fisher’s truistic: “equation of exchange”. Roc’s in R-gDp have to be used, of course, as a policy standard.

Michael Sandifer

Dec 2 2022 at 1:33pm

The only problem I see with this very clearly-written and otherwise well-reasoned post is that assumption that equilibrium long-run GDP growth should be 3.5%, which if inflation averages 2%, would mean an average real growth rate of 1.5%. The confidence with which this prediction is made is unjustified, and obviously very many good enonomists have been wrong when making such predictions.

Forget for a moment that there are models that suggest that productivity growth could go much higher in the years to come. Just consider how unprecedented permanent productivity growth gains were that came from the agricultural and industrial revolutions. Prior to that, productivity growth had been relatively flat for all of human existence. We should not assume that something similar won’t happen again, as AI technology advances and dessiminates. One of the observations Paul Krugman is most famous for is that the internet technology of the 90s seemed to be adding no more productivity growth than the fax machine.

It took electricity adoption decades to fully manifest in terms of productivity. It allowed for a great expansion of more efficient automation. What will the ability to automate everything do, in principle, as AI promises?

Comments are closed.