Understanding Modern Monetary Theory: Part 1

By Scott Sumner

In recent years, a heterodox model called “Modern Monetary Theory” (MMT) has gained adherents. For those who follow the policy debate in the media, this theory is most often associated with advocates of expansionary fiscal policy, perhaps financed by money creation. A federal jobs guarantee is another important MMT policy idea. But theories are about more than real world policies, and it is important to understand the theoretical model that underlies these policy recommendations.

Mainstream economists have been somewhat dismissive of MMT, even where they might agree with particular MMT fiscal policies in the special case of a “liquidity trap”, that is, in a world of zero interest rates. Brad DeLong complained that the model is mislabeled,1 that it is neither modern, nor about money, nor a theory. One might call it an old fiscal tautology. I will show that in order to accept Modern Monetary Theory, one must reject modern monetary theory—that is, the current view of mainstream economists on the role of monetary policy.

In this essay, I begin with an explanation of how MMTers view the role of fiscal policy. I show that they overestimate the role of fiscal policy precisely because they underestimate the importance of monetary policy. In addition, MMTers are too dismissive of the constraints faced by governments that wish to borrow money to finance spending.

The biggest problem with MMT, however, is its model of monetary policy, which is deficient in a number of respects. In section two, I discuss why MMTers deny that monetary policy determines the path of aggregate demand, and hence why in their view it is pointless to give central banks a 2% inflation target. They see the path of inflation as being determined by fiscal policy.

1. MMT views on fiscal policy

Economists William Mitchell, Randall Wray, and Martin Watts (MWW) have written an undergraduate macroeconomics textbook2 that uses the MMT approach. On page 85, they define private sector “net saving” as follows:

- (6.4) (GNP – C – T) – I ≡ (G – T) + (X – M + FNI)

- The terms in Equation (6.4) are relatively easy to understand now. The term (GNP – C – T) represents total income less the amount consumed by households less the amount paid by households to government in taxes net of transfers. Thus it represents household saving.

- The left-hand side of Equation (6.4), (GNP – C – T) – I, thus is the overall net saving of the private domestic sector, which is distinct from total household saving (S) denoted by the term (GNP – C – T).

The equation itself is fine, as it merely rearranges terms in the national income identity. The definition of private sector “net saving”, however, is radically different from the way mainstream economist define the term. This can be seen most easily in a closed economy where there are no trade imbalances, or alternatively using the entire global economy. In that case the MMT net saving identity reduces to:

- (GNP – C – T) – I = (G – T)

In plain English, in the MMT closed economy model net saving equals the budget deficit. To a mainstream economist, GNP – C – T by itself represents private sector gross saving, and to get net saving you subtract depreciation. In contrast, MMTers define private sector net saving as the difference between private gross saving (conventionally defined) and investment spending. Because aggregate saving must equal aggregate investment, any excess private sector saving represents negative public sector saving, i.e. the budget deficit (G – T).

I don’t think it is a good idea to radically redefine basic economic terms in an undergraduate textbook, as students would be hopelessly confused if they later took a mainstream economics course. But the biggest problem with MMT is not semantics; it is the way they seem to draw causal implications from a tautology. On page 88, the authors claim:

- [I]f the external account is in deficit and the private domestic sector is saving overall, then the drain on aggregate demand would require the government to run a deficit of sufficient size to ensure that the total spending is sufficient to absorb the real productive capacity in the economy.

Identities have no necessary causal implications. Indeed, at one level the previous statement does nothing more than repeat the fact that net saving is defined by MMTers as the budget deficit plus the trade surplus. The authors are implying that this equation shows that an attempt to save more will cause a recession unless the government runs a budget deficit (which is negative public saving.)

It is certainly possible that causation goes from some sort of increased desire to save among the public to reduced aggregate demand. Indeed, in early Keynesian models there was a concept called the “paradox of thrift.” In these models, if the public tried to save more this could push the economy into recession. But this is not necessarily the case, as the central bank could offset the effect by easing monetary policy. Again, the national income identity has no causal implications.

In the MMT model, a decreased budget deficit (i.e. “austerity”) is likely to be contractionary and perhaps disinflationary. That’s because a smaller deficit forces the public to engage in less “net saving” (as defined by MMTers, not actual net saving.) This will be brought about by a decrease in aggregate demand and thus a reduced national income, which leads to less net saving.

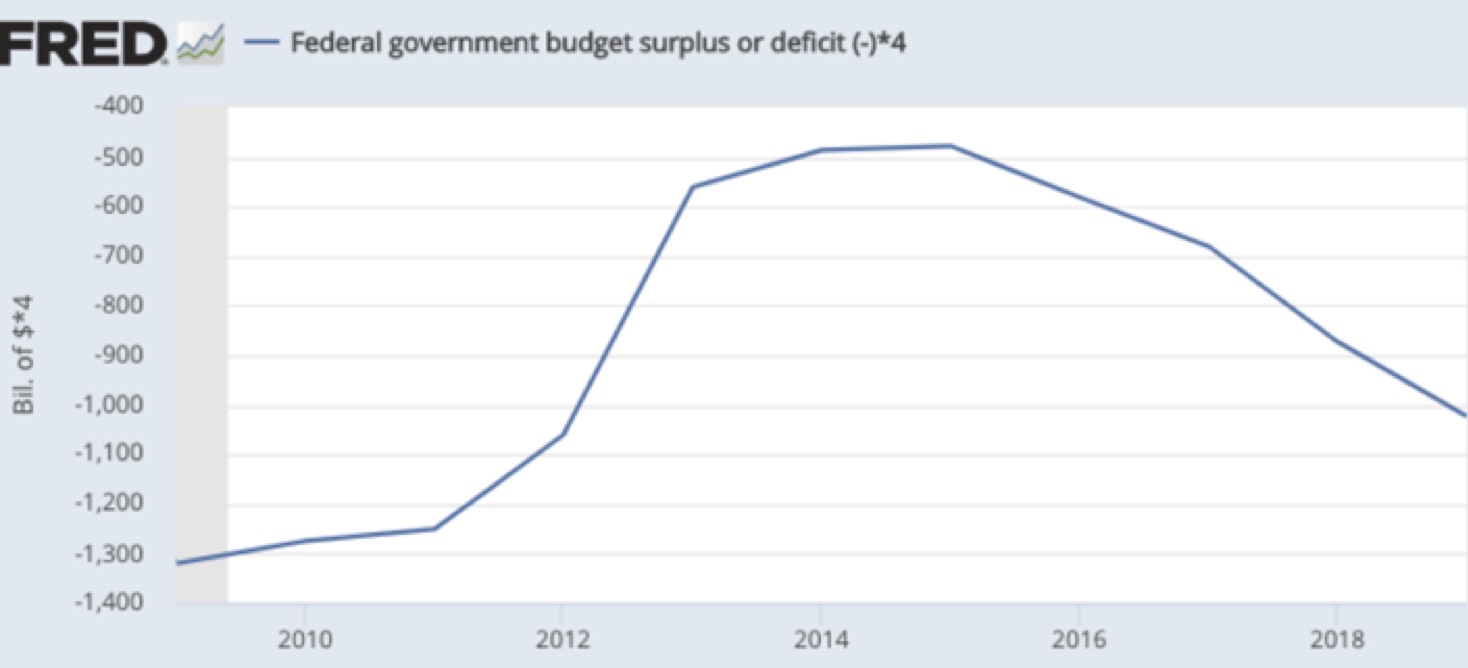

This is not what happens in the real world. A near perfect experiment occurred in 2013, when congressional Republicans forced a sharp move toward austerity. The budget deficit plunged from $1061 billion in calendar 2012 to $561 billion in 2013. (See Figure 1.)Yet growth in aggregate demand actually accelerated. MMTers missed the fact that the Fed tries to offset the effect of changes in fiscal policy, in order to keep inflation close to 2%. Right after the fiscal austerity was announced in late 2012, the Fed adopted a much more expansionary monetary policy. There was no recession in 2013.

Figure 1. Federal government budget surplus or deficit, 2010-2018

Figure 1. Federal government budget surplus or deficit, 2010-2018An even clearer example occurred in 1968, when President Johnson raised taxes to slow inflation. Even though the federal budget quickly swung into surplus, inflation continued to accelerate due to an expansionary monetary policy. Fiscal policy does not determine aggregate demand.

The exact opposite occurred in 2015-19, when a doubling of the budget deficit led the Fed to increase interest rates nine times, with the goal of preventing inflation from overshooting their 2% target. In retrospect, the Fed overreacted a bit, but the basic point is that monetary policymakers set policy at a position expected to lead to macroeconomic stability. It is monetary policy that determines the path of aggregate demand, not fiscal policy.

To be clear, this isn’t just a problem of “causation doesn’t imply correlation”. While budget deficits usually get much bigger during recessions, this by itself does not mean that budget deficits are contractionary. That would be confusing correlation with causation, and is not a valid criticism of MMT. But the austerity of 2013 and the fiscal expansion of 2016-19 were exogenous shocks, that is, fiscal policy changes that were not caused by changes in the business cycle.

For instance, the economy was still somewhat depressed in 2013, and thus the budget deficit did not suddenly decline by $500 billion for cyclical reasons. By 2018-19, the economy was booming, and thus there was no need for switching to a highly expansionary fiscal policy. The surge in deficit spending in 2018 and 2019 was not caused by an economic slump in the way that the surge in deficit spending during 2008-09 was caused by the Great Recession. Indeed both the 2013 and the 2018-19 fiscal shocks reflected domestic political considerations, not stabilization policy.

Rather than being a stabilizing factor, reckless and irresponsible shocks to federal deficit spending often push the Fed to adjust monetary policy to avoid a change in aggregate demand. When the budget deficit is inappropriately enlarged, the Fed responds with tighter money to keep inflation at 2%, and vice versa.

In the next section, we’ll see that MMTers get fiscal policy wrong because they get monetary policy wrong—they underestimate the extent to which monetary policy offsets the impact of fiscal policy changes.

2. MMT views on monetary policy

During the 1930s, John Maynard Keynes began to question the efficacy of monetary policy, especially when interest rates were near zero. As an alternative, Keynes recommended using fiscal policy to assure an adequate level of aggregate demand, especially during periods when the public mood turned bearish, business investment plunged, and/or the propensity to save rose sharply.

MMTers take this idea much further than even Keynes. They aren’t just skeptical of the efficacy of monetary policy when interest rate are near zero; they argue that monetary policy is largely ineffective even during normal times, that is, when interest rates are positive.

For instance, when interest rates are positive, mainstream economists believe that open market purchases of bonds by the central bank are highly expansionary, and will boost aggregate demand. In contrast, MMTers don’t believe that open market operations have a significant impact on the economy, even if it enlarges the size of the monetary base. Here is MWW on page 342:

- Second, [MMTers] would challenge the theory of inflation based on [the quantity theory of money], and argue that if a fiscal deficit gives rise to demand pull inflation, then the ex post composition of ΔB + ΔMb in Equation (21.1) is irrelevant. Overall spending in the economy is the driver of the inflation process, and not the ex post distribution of net financial assets created between bonds and base money.

Thus MMTers claim that money financed deficits are no more inflationary than bond financed deficits. This is an extremely radical claim, which would not be accepted by most economists, at least when interest rates are positive.

Let’s go back to 1998, when the monetary base was roughly $500 billion and risk free short-term interest rates were about 5%. In mainstream economic models, a Fed purchase of another $500 billion in bonds, paid for with newly issued base money, would be highly expansionary and highly inflationary. This action would immediately double the size of the monetary base.

Monetarists would explain the effects by focusing on the increased money supply. There would be a surge in spending as the public and banks tried to get rid of excess cash balances. Keynesians would focus on the role of interest rates. The huge open market purchase would push rates much lower—probably to zero—leading to a surge in aggregate demand.

MMTers take the Keynesian model as a starting point, and assume that this sort of large open market purchase would drive rates down close to zero. But MMTers don’t believe that interest rates have much impact on aggregate spending.

Because MMTers don’t believe that money creation is inflationary, they don’t worry about the burden of a large government debt, at least for countries with their own currency. They argue that there is no danger of default, as the government could repay the debt by printing money. That may be true in a technical sense, but throughout history, a policy of monetizing debts has often led to hyperinflation.

So where does this heterodox MMT view of money come from? Just as with the net saving equation discussed above, the MMT model of money includes claims that do not mean what MMTers think they mean. Their model of money is often summed up in a series of maxims:

- Banks don’t lend out reserves

- There is no money multiplier

- Money is endogenous

- There is no natural interest rate (other than zero)

In each case, there is a kernel of truth, and in each case, MMTers draw implications that go far beyond what is justified by the narrow sense in which each statement has validity.

For instance, when banks make loans they often credit the borrower’s account at the bank. MMTers point out that unless the borrower withdraws the funds as cash, there is no direct impact on the total aggregate stock of bank reserves. But this does not mean that a Fed injection of new reserves into the banking system has no indirect impact on the quantity of loans. Here’s Paul Krugman,3 responding to MMT criticism of his claim that increased bank reserves will spur more lending:

- When we ask, “Are interest rates determined by the supply and demand of loanable funds, or are they determined by the tradeoff between liquidity and return?”, the correct answer is “Yes”—it’s a simultaneous system.

- Similarly, if we ask, “Is the volume of bank lending determined by the amount the public chooses to deposit in banks, or is the amount deposited in banks determined by the amount banks choose to lend?”, the answer is once again “Yes”; financial prices adjust to make those choices consistent.

- Now, think about what happens when the Fed makes an open-market purchase of securities from banks. This unbalances the banks’ portfolio—they’re holding fewer securities and more reserve—and they will proceed to try to rebalance, buying more securities, and in the process will induce the public to hold both more currency and more deposits. That’s all that I mean when I say that the banks lend out the newly created reserves; you may consider this shorthand way of describing the process misleading, but I at least am not confused about the nature of the adjustment.

To mainstream economists, everything in the macroeconomy is interrelated. This is what Krugman meant by suggesting, “it’s a simultaneous system “. Thus, while a banker might believe that a Fed open market purchase of Treasury bonds makes his or her bank no more likely to make a loan to the local property developer, economists see an open market operation as setting in motion a series of changes in asset prices that affect the economy through what is sometimes called a money multiplier.

MMTers often say that there is no money multiplier. If that means the money multiplier is often unstable, then the claim is true. But mainstream economists have always understood that the money multiplier can be unstable at times. MMTers seem to go even further, denying that an injection of reserves into the banking system will boost lending, deposits and, ultimately, nominal GDP. That claim is not valid. Indeed when interest rates are positive, a doubling of the monetary base will double all nominal variables in the long run, including the broader monetary aggregates (M1 and M2), the price level (CPI), and nominal GDP.

When confronted with thought experiments such as the effect of doubling the money supply, MMTers respond that the central bank is unable to control the money supply. On closer inspection, however, their actual claim is that the money supply is endogenous if the Fed is targeting interest rates at a positive level.4 In other words, they believe that the Fed must passively adjust the money supply to hit their interest rate target.

Once again, there is a grain of truth in the MMT claim that the money supply is endogenous when the central bank targets interest rates. But MMTers overlook the fact that interest rates are also endogenous when the central bank targets inflation. The central bank must passively adjust interest rates as necessary to hit the 2% inflation target. Yet MMTers view interest rates as the instrument of monetary policy.

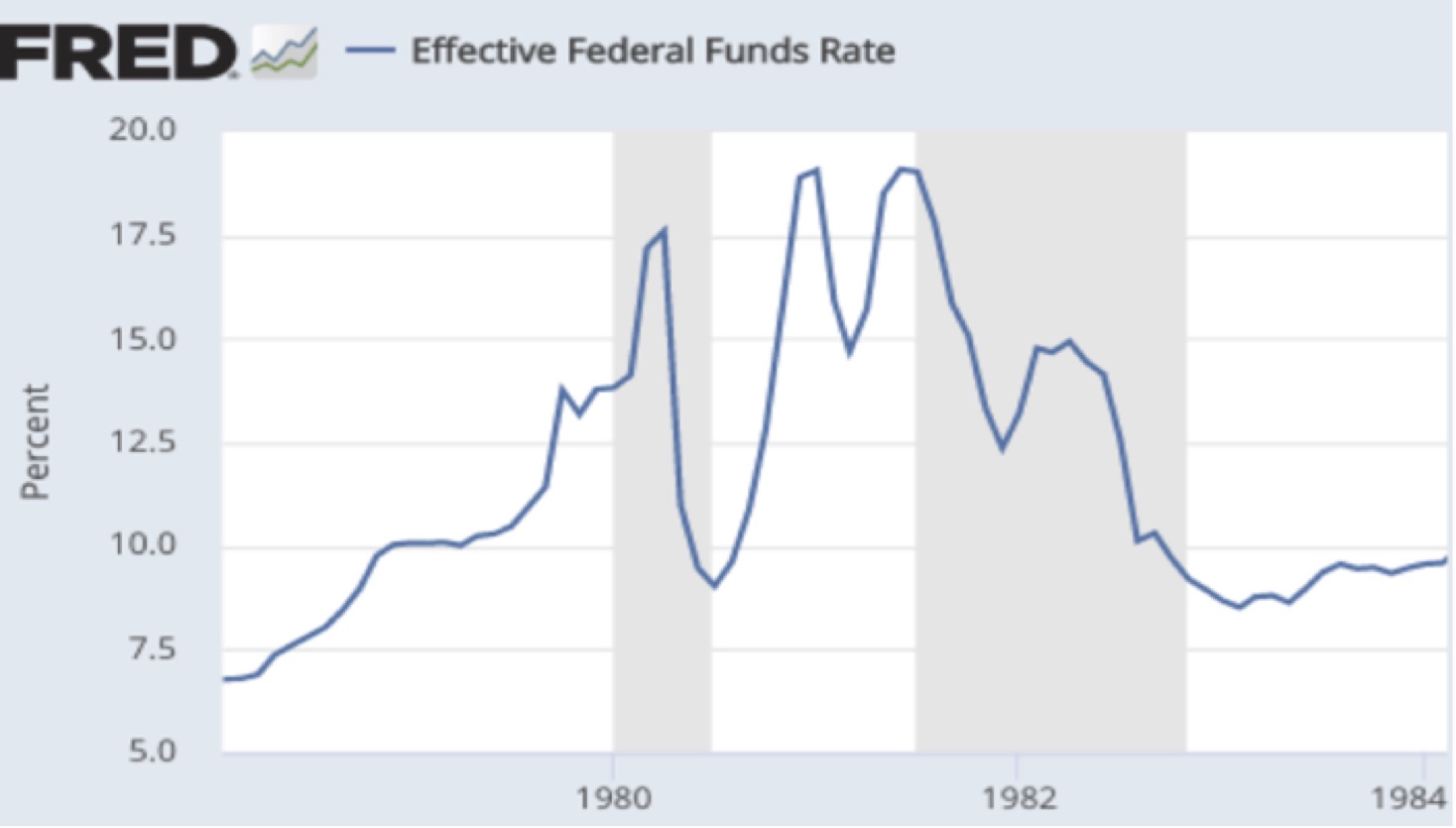

More importantly, endogeneity doesn’t mean what MMTers think it means. It doesn’t mean that central banks can not, do not, or should not control the money supply; it just means that in order to do so the central bank must allow interest rates to fluctuate. But we know that central banks are willing to adjust their interest rate target quite actively, if that is what is required to control the money supply and inflation. Look at how sharply interest rates moved around during 1979-82, when Paul Volcker’s Fed was willing to allow dramatic moves in short-term interest rates in order to get the money supply and inflation under control as shown in Figure 2.

Figure 2. Effective Federal Funds Rate

Figure 2. Effective Federal Funds RateEven if the Fed is targeting interest rates, it remains true that an adjustment in the interest rate target (say a rate cut) that leads to an increase in the money supply will have the same sort of multiplier effect on the economy as would occur if the central bank simply injected money without worrying about the impact on interest rates.

The central bank of Singapore targets exchange rates, not interest rates. In Singapore, both the interest rate and the money supply are endogenous. But their decision about where to set exchange rates impacts both interest rates and the money supply, and those policy decisions affect the economy just as much as if they were directly targeting the money supply or interest rates.

Ultimately, MMTer seem confused about the meaning of “endogenous”. Variables are not inherently exogenous or inherently endogenous. Instead, economists treat variables as exogenous or endogenous for purposes of convenience. An endogenous variable is a variable explained by the model being considered, whereas an exogenous variable is one that is not explained by the model.

MMTers assume that saying “money is endogenous” is equivalent to saying that the central bank cannot control the quantity of money. Not so. It merely indicates that in order to control the stock of money the central bank must allow variables such as exchange rates and interest rates to move around.

As long as the Fed targets interest rates at a fixed rate, say 2.25%, it has no independent ability to adjust the monetary base. But if the central bank wishes to increase the monetary base they can simply engage in open market purchases and simultaneously reduce their target interest rate. At this point, MMTers would argue that any attempt to force significantly more base money into the economy would quickly reduce interest rates to zero. This is not necessarily the case, as MMTers tend to ignore the role of the natural rate of interest.

Economists generally define the natural interest rate as the short-term interest rate that will lead to macroeconomic equilibrium. For simplicity, define the natural interest rate as the interest rate setting that allows the Fed to hit its 2% inflation target. This rate is sometimes viewed as being policy invariant, which is not the case. If previous Fed policy has been much too tight, producing a severe recession, then the interest rate setting required to hit a 2% inflation target will be lower than if previous monetary policy had been expansionary. The natural interest rate moves around for many reasons, including factors related to monetary policy. It almost always declines during recessions.

Unfortunately, the fact that the natural interest rates moves around over time doesn’t mean what many people seem to think it means. Contrary to the assumption of MMTers, an injection of new base money into the economy can easily raise both the natural rate of interest and actual market interest rates. This occurs because monetary stimulus boosts both inflation and (in the short run) real GDP. An inflationary and/or booming economy will have a higher natural rate of interest due to the income effect and the Fisher effect.

In the previous thought experiment where the Fed suddenly doubled the monetary base back in 1998, MMTers would assume the action would immediately push interest rates down to zero. But it is at least as likely that this action could produce extremely high inflation, which would push interest rates up into double digits. There are many examples in Latin America and elsewhere where rapid money supply growth is associated with high inflation and high nominal interest rates.

The income effect is also quite important. During a recession, interest rates tend to fall, as there is less borrowing to finance investment spending. MMTers see this decline as representing “monetary policy”, but interest rates declined during recessions even before the Fed was created. Because MMTers see all interest rate movements as representing monetary policy, they even deny that a positive “IS shock” (such as a housing boom or a tech boom) would push up interest rates. Here are MWW (p. 464):

- The fact that the money supply is endogenously determined means that the LM schedule will be horizontal at the policy interest rate. All shifts in the interest rates are thus set by the central bank and funds are supplied elastically at that rate in response to the demand. In this case, shifts in the IS curve would not impact on interest rates. From a policy perspective this means the simple notion that the central bank can solve unemployment by increasing the money supply is flawed.

Once again, MMTers misunderstand the concept of endogeniety, as the final two sentences don’t follow from the first two sentences. Because central banks target inflation, an investment shock will lead central banks to adjust their interest rate target in order to avoid missing their inflation target. This is why changes in the business cycle do impact interest rates.

Indeed, market interest rates respond even before the central bank adjusts its official interest rate target. Thus, the election of Donald Trump in November 2016 immediately led to higher market interest rates, as investors looked ahead to the impact of his proposed corporate tax cut. To claim that central banks determine the path of interest rates is like claiming that a little boy that runs out ahead of a Rose Bowl parade is determining the path of the parade through the city.

In Part 2, I will show where MMT fits on the ideological spectrum, relative to other schools of thought. On a wide range of issues, MMT occupies a position on one extreme of the ideological spectrum, where Chicago school economists such as Milton Friedman are at the other extreme. Finally, I will examine why MMTers have difficulty communicating their ideas to other economists.

Footnotes

[1] Brad DeLong, Is “Modern Monetary Theory” Modern or Monetary or a Theory? Delong, 2011/04.

[2] William Mitchell, L. Randall Wray, and Martin Watts. Macroeconomics. Red Globe Press, 2019.

[3] Paul Krugman, “Bans and the Monetary Base–Wonkish” The New York Times, August 16, 2013.

[4] Even MMTers concede that the Fed can control the monetary base when interest rates are zero, or interest is paid on bank reserves; I focus on the positive interest rate case because this is where MMT views are most distinctive relative to those of mainstream economists.

*Scott Sumner is Professor Emeritus in Economics at Bentley University in Waltham, Massachusetts, and Research Associate on monetary policy at the Mercatus Center. He earned his Ph.D. in economics at the University of Chicago in 1985. He blogs both at EconLog and also at his personal blog at The Money Illusion.

For more articles by Scott Sumner, see the Archive.