Australia has long been known as the “lucky country”, and hence many people attribute their current 28-year expansion to dumb luck—perhaps they benefited from trade with China. The NYT has a new piece that suggests the reason for Australia’s success goes well beyond just luck:

But China’s gravitational pull can explain only so much. For one thing, other countries nearby have had recessions, some severe, in recent decades. And there are a long list of policy choices that enabled the long Australian boom even as otherwise similar economies sank.

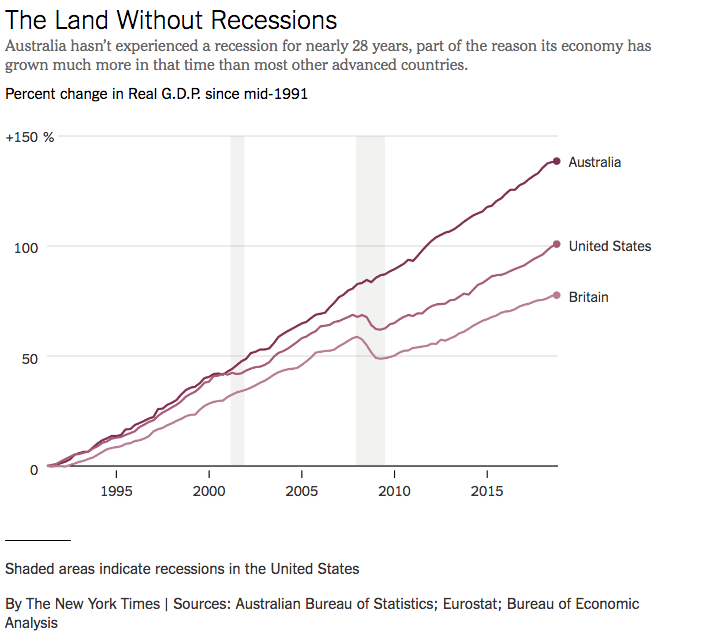

One episode is particularly telling. In 1997, an East Asian financial crisis walloped the economies of countries like South Korea, Thailand and Indonesia. These nations were major buyers of Australian exports. The value of the Australian dollar started to fall on global currency markets, putting the expansion at risk only six years in.

On the other side of the Tasman Sea, New Zealand’s central bank responded to the same problem by raising interest rates. After all, a falling New Zealand dollar indicated a lack of confidence in the currency and implied that inflation would soon rise.

At the Reserve Bank of Australia, by contrast, officials concluded that the falling value of the Australian dollar reflected shifting economic fundamentals that were ultimately healthy — part of how the Australian economy could adapt to faltering demand from East Asia.

Rather than raise interest rates to try to prevent a falling currency, they viewed a falling currency as the key to navigating the peril — by making Australian exports more competitive in the United States and Europe, for example. . . .

Sure enough, New Zealand fell into recession in 1997 and 1998, while Australia endured only a period of subpar growth. Good policy, it turns out, has a way of creating good luck. And it wasn’t the only time.

The Kiwi’s were foolish to focus on inflation targeting.

Although the NYT piece is mostly excellent, there are a few weak spots:

The housing market in Australia did not see the severe boom-bust cycle that the United States experienced as part of the global financial crisis, though the market has softened lately.

Technically that’s accurate, but most American readers will get the wrong impression. Most readers will infer that Australia was smart to avoid the excesses of 2000-06, as experienced in America. But they did not avoid those excesses; their housing boom was just as big as ours. They avoided the “boom-bust cycle” by avoiding the bust, not by avoiding the boom.

HT: Clare Zempel

READER COMMENTS

Alan Goldhammer

Apr 6 2019 at 5:17pm

Let’s export Steven Moore and Herman Cain to Australia and bring their economy back to earth.

Benjamin Cole

Apr 6 2019 at 7:42pm

I prefer NGDPLT.

But the track record of the Reserve Bank of Australia’s 2% to 3% inflation band target is impressive. Moreover, the Reserve Bank of Australia has shown a cool head and has allowed inflation into the 4% range for some periods without panicking.

It is a mark of the permanent constipation of the American macroeconomics profession that even this small change to an inflation band target, and the provision for an additional percent of inflation when needed, is a bridge too far.

Indeed, some American macroeconomists are still rhapsodizing about 0% inflation.

The People’s Bank of China also has 30-year track record of growth, and an approximate 3% inflation target during that much of that time.

So why the perennial sanctimonious sermonettes about inflation from the American macroeconomics community?

Matthias Görgens

Apr 7 2019 at 11:33am

Targeting a long enough average growth rate of any variable works out to nearly the same as targeting its level.

Australia targets average inflation, I think? Averaged over the ‘business cycle’ or so?

Perhaps getting the Fed on such an average target might be good enough in practice to get most of the benefit of the nGDP level target?

Ahmed Fares

Apr 6 2019 at 10:18pm

Bill Mitchell wrote an article describing how Australia did things right in respect of fiscal policy titled:

The effectiveness and primacy of fiscal policy – Part 1

http://bilbo.economicoutlook.net/blog/?p=41888

Here is a slice:

The agility of fiscal policy

Monetary policy is a blunt-policy tool with uncertain impacts. It operates through relative unknown interest rate impacts, which first have to work through shifts in non-government sector behaviour, which then manifest as shifts in spending.

The time lags in these shifts are unknown as are the impacts.

For example, it is often assumed that lower interest rates will stimulate business investment, on the basis that lower costs of finance will render marginal projects, that under higher rates were not profitable enough, now profitable.

However, as we have seen in the aftermath of the GFC, borrowing volumes remain relative low despite nearly a decade of low to zero interest rates.

Why? Because investment decisions are based on a range of factors, of which the cost of funds is just one. A firm will not invest, no matter how low the funding costs go, if they do not think they can sell the extra output that the increased productive capacity would produce.

That is just one example of why monetary policy is not a very effective counter-stabilisation policy tool.

However, economists started producing many articles in the 1970s and after, to justify the growing dominance of Monetarism and the associated attacks on discretionary fiscal policy, which claimed that fiscal policy was subject to time lags which would render its application dangerous.

——–

In other words, just how agile or nimble is fiscal policy?

The answer is very nimble.

In what follows I provide some recent examples where fiscal policy has been very ‘nimble’ and significantly influenced the economic cycle. —Bill Mitchell

Scott Sumner

Apr 6 2019 at 11:00pm

Borrowing is low despite low rates, and that’s evidence that monetary policy is weak? Isn’t that reasoning from a price change?

Ahmed Fares

Apr 7 2019 at 1:18am

Isn’t that reasoning from a price change?

Your article against reasoning from a price change makes sense for something like the price of oil. But then you use the IS-LM diagram to prove the same point, which is where the confusion arises. Because MMTers and others are not using the same model you are.

Your article: https://www.themoneyillusion.com/in-economics-price-changes-dont-have-any-effect-they-are-effects/

MMT comments:

In summary, the IS-LM approach is central to the bastardisation of Keynes’ work by John Hicks in the late 1930s and was consolidated into the main textbook macroeconomic exposition from then on.

Hicks rejects his own earlier work:

Hicks said he “invented a little apparatus” (the IS-LM framework) to bring together Keynesian and Classical economics into an integrated model.

By the 1970s, Hicks started to sign his academic papers John Hicks rather than J.R. Hicks, which reflected his growing sense of rejection of his earlier work.

Here in his writings, it gets even weirder:

J.R. Hicks … [is] … a “neoclassical” economist now deceased … John Hicks … [is] … a non-neo-classic who is quite disrespectful towards his “uncle”.

So looking at your article I understood exactly what you meant when you said that price changes can arise from shifts in either supply or demand, however, it may not hold if the model you use is not the correct one.

Scott Sumner

Apr 7 2019 at 12:52pm

I don’t use the IS-LM model—I agree that that model is useless.

And reasoning from a price change is always wrong, regardless of what model you choose to use. The correlation of borrowing and interest rates tells us nothing about the potency of monetary policy, in any sensible model.

Matthias Görgens

Apr 7 2019 at 11:39am

If monetary policy had long and variable lags, there would be trillion dollars bills lying on the sidewalk waiting to be picked up by (statistical) arbitragers.

Even weak versions of the efficient market hypothesis suggest that monetary policy has long and variable ‘foreshadowing’: merely the credible announcement of policy will already make market participants anticipate its effects.

Scott Sumner wrote a lot about that in his Midas Paradox. But it’s really rather common sense.

To be effective, monetary policy still needs to have a channel over which to work mechanically. But that channel doesn’t need to be fast or direct by itself.

E. Harding

Apr 7 2019 at 6:39pm

Neither Australia’s NGDP or inflation look that stable. Only its real GDP does. So the mystery is left unexplained.

https://fred.stlouisfed.org/graph/?g=nymv

Scott Sumner

Apr 7 2019 at 11:11pm

Relative to trend the Aussies did very well. Compare NGDP growth rates from 2007:2 to 2009:2 in the three countries, and you’ll see why they avoided the Great Recession.

Lorenzo from Oz

Apr 8 2019 at 6:56pm

Stable in what sense? The claim is not that Australia has no business cycle, the claim is that it has a very flat one. Given that the RBA’s target is to maintain inflation “between 2 and 3 per cent on average over the business cycle” and that the average inflation rate has been 2.6%pa since the target was adopted, the achievement of the target has clearly been very successful.

MV = py. Basically, if y is a bit down, push up on p. If p is a bit up, push down on y. That is the policy. It stabilises income expectations, so stopping dramatic collapse in transactions (what we call a recession). I am not sure that requires NGDP to be other than just stable enough.

Lorenzo from Oz

Apr 8 2019 at 6:47pm

Eventually, “they’re just lucky” had to wear thin.

Comments are closed.