A recent Bloomberg article suggested that the Fed should declare victory over inflation:

Granted, it may feel premature, if not foolhardy, to declare “mission accomplished” on inflation. It’s not just the rise in tariffs and the fall in immigration; there are a lot of structural factors in the economy pointing to more inflation: more debt, an aging work force, slower productivity growth, and a world that trades less and is less reliant on the dollar. Still, declaring victory now will make it easier for the Fed to make policy in the future.

First, the days of an inflation rate below 2% may be behind us. If so, the Fed will need to internalize this truth in its communications and policies — or risk becoming too contractionary for too long in the future. When it undertakes its next framework review, it may need to increase its target rate from 2%. It can credibly do so now that inflation has been licked.

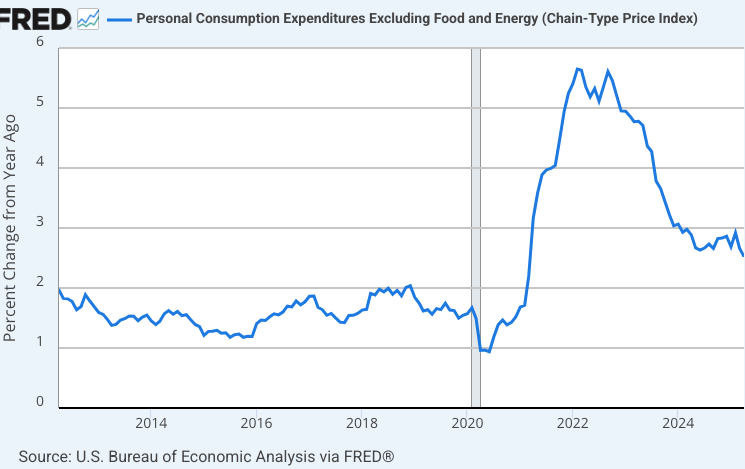

I’m not convinced that victory has been achieved, nor do I believe it would be a good time to raise the inflation target. Here’s the 12-month rate of inflation using the core PCE indicator:

Core inflation has recently fallen to 2.5%, but that’s still above the Fed’s 2% target. Furthermore, the Fed has a flexible inflation target. Under that sort of policy regime, inflation should run a bit below 2% during booms and a bit above 2% during recessions. We are clearly in an economic boom.

I do not see any good economic arguments for raising the inflation target above 2%. More importantly, even if a higher inflation target were a good idea, the optimal time to raise the target would be during the next period of near-zero interest rates, not when short-term interest rates are above 4%. The adoption of a higher inflation target can be a powerful tool for stimulating an economy stuck at the zero lower bound.

In general, I am skeptical of calls for raising the inflation target. Doing so would reduce the credibility of the Fed, as investors would begin to doubt its commitment to low inflation. This might make it even more difficult to bring inflation back down after it overshoots the target rate for an extended period of time.

READER COMMENTS

Kevin Erdmann

Jun 16 2025 at 8:08pm

I’m not sure if you’ve seen the post where I collected all my thoughts on why rents should not be included in the inflation measure that the Fed tracks. If you exclude rent from the CPI measure, it dropped sharply to 2% in July 2022 and has tracked very tightly around 2% since then. Trailing 12 month CPI excluding shelter is currently 1.4% and core CPI excluding shelter is 1.8%.

Here’s the post:

https://kevinerdmann.substack.com/p/rents-shouldnt-influence-monetary

Scott Sumner

Jun 16 2025 at 8:28pm

Yes, I’ve seen those posts. I’m not really a fan of removing certain items from the CPI. If we are going to do that then we should just look at NGDP, which is still growing too rapidly.

Kevin Erdmann

Jun 16 2025 at 8:38pm

I made additional arguments in that post that I haven’t made elsewhere. The long and short of the additional arguments is that land rents are different than rents on structures. They are economically like other things that are excluded from production and price statistics, like gifts, theft, etc.

Scott Sumner

Jun 17 2025 at 10:07am

There are many problems with the CPI. But I don’t believe they get fixed by looking at measures that remove a few items. I would favor either looking at what the Fed is actually targeting, or else looking at entirely different (and better) measures such as wage inflation and NGDP growth, which are still too high.

Kevin Erdmann

Jun 17 2025 at 11:10am

The wage measure would probably avoid this problem. The rent problem biases nominal GDP growth higher too, though. All else equal, if 1% of the American housing stock was destroyed this year, NGDP, as measured, would be higher by a tenth of a point or two next year.

Craig

Jun 16 2025 at 10:00pm

Wait at least two months because the Y/Y CPI based off last 12 months and month 11 and 12 are .1 for July 24 and a 0 for Jun 24 so right now difficult for the Y/Y to move down.

Brent Buckner

Jun 17 2025 at 9:17am

Your point about the Fed’s regime and the desirability of running somewhat below 2% for a time would have been even more clear if you’d given the regime’s full designation – flexible *average* inflation target.

Scott Sumner

Jun 17 2025 at 10:04am

Yes, but the Fed has since made clear that the term “average” is misleading, they never had any intention of targeting average inflation, otherwise policy would have been far tighter.