Falling stock prices have recently been in the news. You see headlines about stock investors being worried about “the Fed”. But when you read the actual articles there is often little or no discussion of how Fed policy might be depressing stock prices. More often, the claim is that markets are worried about rising interest rates.

I have two problems with this sort of claim. First, there’s actually no reliable correlation between interest rates and stock prices. Interest rates generally fall sharply during recessions, and yet stocks often do poorly.

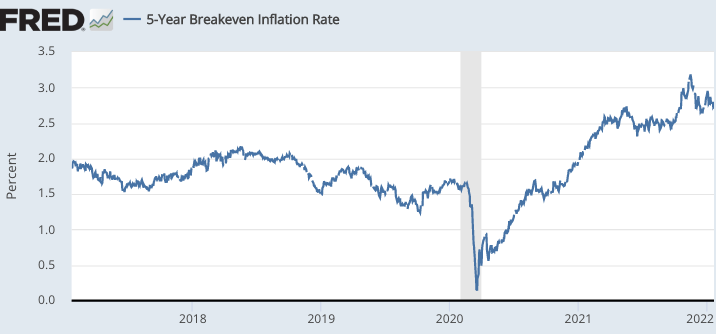

More importantly, interest rates are not monetary policy. To suggest they are is to “reason from a price change.” There are occasions when a much tighter monetary policy will be associated with higher interest rates, but this doesn’t seem to be one of them. The 5-year TIPS spread has fallen a bit, but remains well above the Fed’s target. Money is certainly not tightening in any dramatic fashion. Indeed, it should probably be even tighter.

I have no idea why market interest rates have recently crept up a bit (albeit remaining at extremely low levels.) Perhaps it is due to fear of an overheating economy. But expectations of tighter money is not the primary factor.

READER COMMENTS

Roger Sparks

Jan 24 2022 at 2:26pm

I think the problem with stock prices stems from the “Where else can they put their money?” issue.

More fundamentally, fiat money has the same issue with “What’s it worth?” that crypto has. The advantage that fiat enjoys is that new fiat is issued into a functioning economy as a fungible addition. The fiat problem encountered is that money supply is increased.

Because new money is an addition to the money supply, I wrote my article “Money is Not an IOU, It’s more Like a Ticket“, wherein I argue that money should be a considered as being a valuable, reusable ticket into the marketplace.

MIchael Sandifer

Jan 24 2022 at 4:05pm

I very much disagree. Coming into today, the 10 year breakeven had fallen 27 basis points, while the 10 year Treasury yield climbed 11 basis points, and the S&P 500 had fallen 8.25%, which I translate into a roughly 33 basis point drop. The 5 year breakeven rate fell 25 basis points, as the 5 year Treasury yield rose 25 basis points.

Also, the date of expected rate increases moved up in the calendar over this period, as well as the total number of expected rate increases for 2022, which now stands at about 4.

I do agree that the there are some real factors at play as well, including some related to Omicron and geopolitical tensions, but there’s not much doubt in my mind that the Fed has tightened monetary policy and caused some nominal shocks, with comments indicating adjustments to forward guidance.

I think the media’s straightforward interpretation is correct. The rising Treasury yields indicate that the market expects the Fed to tolerate less inflation than originally believed.

Scott Sumner

Jan 24 2022 at 8:42pm

The dip in TIPS spreads is quite small.

MIchael Sandifer

Jan 24 2022 at 11:50pm

26 basis points on the 10 year spread since January 3rd is small? Small, in what sense?

If 1-for-1 with changes in the expected mean NGDP growth path, with the baseline at 4%, that would represent a 6.5% decline in the S&P 500. We witnessed an 8.31% decline in the S&P 500 over the same that period. Some of the drop in the index was likely due to real factors, so these numbers seem pretty reasonable in the context of tightening monetary policy.

MIchael Sandifer

Jan 26 2022 at 4:27pm

Here’s the simplest, most straightforward way to look at it: Percent changes in the S&P 5oo index usually reflect percent changes in the mean expected NGDP growth path, 1-for-1.

Why do I say this? For one, since 1962, the mean NGDP growth rate and the mean S&P 500 discount rate have differ by only 20 basis points. Theoretically, this all makes sense for reasons I’ve offered in the past.

And, the changes we see in interest rates, in situations such as we’re in now, seem very much consistent with this model. I find it very compelling theoretically and empirically.

Lastly, the implications, if this perspective makes sense, are huge. Just consider what changes in the S&P 500 imply about the NGDP growth path after the 2001 and 2007-2009 recessions, for example.

Mark Louis

Jan 24 2022 at 4:58pm

Index dividend futures trade and can be a good cross-reference on this sort of analysis. 2025 SPX dividends closed today at 67.40, which is a bit off the high but basically in-line with a rolling 2 month average.

People forget what enormous swings stock prices can have around “fundamentals.” The dividend contracts are not nearly as volatile as the market, suggesting that the majority of the volatility is coming from valuation.

James

Jan 24 2022 at 5:03pm

If interest rates do not reliably affect market moves but most market participants believe low rates predict higher returns, those participants will create mispricings in the time series of stock market returns. An arbitrageur would be able to turn that into a source of excess return by varying your equity exposure against the crowd.

Scott Sumner

Jan 24 2022 at 8:43pm

But do most participants believe that lower rates predict higher returns? In that how they felt in late 2008?

Rajat

Jan 24 2022 at 7:42pm

Taking market signals at their face, it seems the market is concerned that equilibrium real rates are rising and that the drop during Covid was partly just a lull rather than entirely enduring. This would explain why shares of high growth companies like those like the Nasdaq have fallen the most.

Scott Sumner

Jan 24 2022 at 8:44pm

Yes, I agree that rising real rates may be having some effect on tech stocks. I’m not sure why they originally fell so low.

Jose Pablo

Jan 24 2022 at 9:58pm

Markets should be worried about the FED. In particular about the FED ability (or its lack thereof), under current circumstances, to maintain the “put option” (= the use of monetary policy and other tools to “sustain” the market) that have been in place (or so “the market” believes) since Greenspan.

Fran

Jan 24 2022 at 10:21pm

Question: Another market measure of expected inflation is the 5 year 5year forward expected inflation rate (https://fred.stlouisfed.org/series/T5YIFR). Why do you favour the breakeven rate? These two series seem to imply different things about monetary policy: while one suggests policy to be too loose, the other that monetary policy is about right as future inflation risk is not higher than before the pandemic.

Greg G

Jan 25 2022 at 8:09am

Scott, I understand why you always emphasize that it is wrong to reason from a price change and I want to thank you for teaching me that.

But, since you always ALSO emphasize that this is an extremely common mistake, I don’t understand why you are skeptical that investors making such an extremely common mistake couldn’t be driving the recent market decline in stocks, at least in the short term.

milljas

Jan 25 2022 at 9:55am

They have clearly communicated a certain number of increases, perhaps the market is worried the Fed will make a mistake in either direction, not that it’s concerned policy is too tight. Russia and Omicron also are issues, so the P(of recession) is perhaps increasing. Or it’s just a risk off move of some sort, the sell-off is clearly oriented towards certain types of sectors and companies. It’s not hitting banks and autos.

I also think that policy has (tried to be ) tightened as the one commenter explains, even by your own logic, it would seem they are at making attempts via communications. It may be too little relative to what is required as you point out, but they are trying. Why they wait for March and not just do 25 bps now. Then again a few days later. The credibility call-outs must start to hurt at some point, I doubt hedge funds did the same with Greenspan.

In any case, if we actually knew, we wouldn’t be typing here, we’d be trading futures to make the market more efficient!

Monetary policy was boring for a while, certainly seems (a little) less so today.

Thomas Lee Hutcheson

Jan 25 2022 at 12:47pm

I disagree that the TIPS spread is “well above” the Fed’s target. The Fed’s 2.0% p.a. target for PCE is the equivalent of about a 2.3% p.a. increase in the CPI. the rate to which TIPS applies. As of Monday, the 10 year TIPS was for inflation to average 2.38% over the next 10 years, and the 5 year TIPS to average 2.74%. These are definitely above target. The Fed still has work to do to bring expectations down to its target but the actual margins are quite modest. The 10 year TIPS expectation is that the Fed will overshoot its target by a cumulative 0.78%. Not “well above.”

Comments are closed.