In the past, I’ve called for replacing the aggregate demand curve with a curve representing a given level of nominal spending. Under this approach, a positive nominal spending shock occurs when NGDP growth is above target, and vice versa.

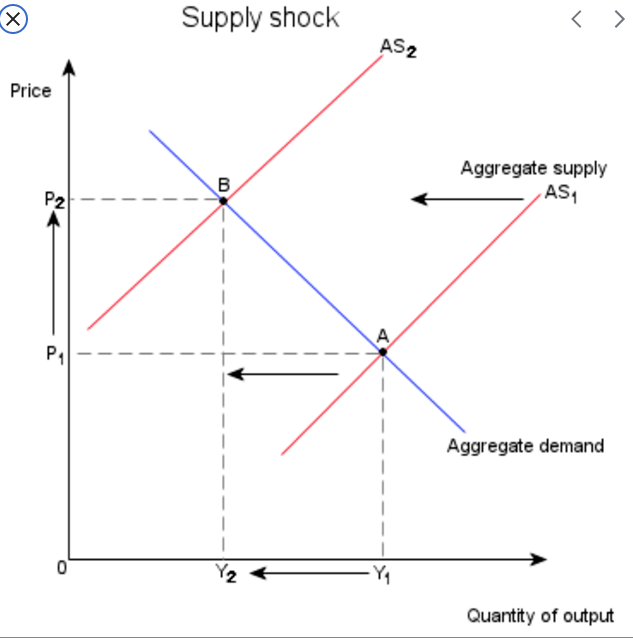

It seems to me that the Covid economy provides a perfect example of why “aggregate demand” is not a useful way to think about the forces shaping the macroeconomy. Over the past two years, prices have risen by more than normal while real GDP growth has been well below trend. In the standard AS/AD model, this looks something like the following:

(To be clear, the drop in output over the past two years is relative to trend; in absolute terms RGDP is up slightly.)

So from an AS/AD perspective it looks like the US was hit by a negative supply shock. But it’s equally true that the inflation is being driven by surge in demand for goods (as opposed to services.) You could say that the increased demand for goods has caused a supply shock, as our economy cannot suddenly turn on a dime and produce far more goods and far fewer services.

You can see how terms like “supply” and “demand” don’t do justice to the complexity of the situation. No matter how many times we say that aggregate demand is not the same thing as industry “demand”, people will continue to confuse the two concepts. Consider the following word salad from Investopedia:

Aggregate Demand Controversy

Aggregate demand definitely declined in 2008 and 2009. However, there is much debate among economists as to whether aggregate demand slowed, leading to lower growth or GDP contracted, leading to less aggregate demand. Whether demand leads to growth or vice versa is economists’ version of the age-old question of what came first—the chicken or the egg.

Boosting aggregate demand also boosts the size of the economy regarding measured GDP. However, this does not prove that an increase in aggregate demand creates economic growth. Since GDP and aggregate demand share the same calculation, it only indicates that they increase concurrently. The equation does not show which is the cause and which is the effect.

I have no idea what any of that means. Surely they can’t be equating AD and real GDP? In fact, it’s even worse. In the previous paragraph they equate AD with real consumer spending (i.e. C/P.) By that definition, a burst of technological progress which shifts the AS curve to the right will cause aggregate demand to increase, even if the aggregate demand curve never shifted.

It’s as if Investopedia was confused as to whether an increase in GDP caused more C+I+G, or whether an increase in C+I+G caused more GDP. At least that’s what I think they are saying here:

Since GDP and aggregate demand share the same calculation

All this confusion could be eliminated if we changed the language of macroeconomics to something like a NS/RO model—nominal spending and real output. Nominal GDP and real GDP most certainly do not “share the same calculation”.

With that framing, the Covid economy is much easier to explain. Over the past two years, nominal spending has grown at a normal rate, whereas real output has been depressed by structural problems. Going forward, nominal spending over the next year is likely to be too high to maintain an average inflation rate of 2%. If I am correct, then by the end of 2022 we will have had a period of elevated inflation associated with both above normal nominal spending and structural problems in production.

READER COMMENTS

Philip George

Nov 29 2021 at 11:32pm

There is no confusion. Aggregate Demand equals NGDP. By the same token supply should be in nominal terms, not real terms.

Thomas Lee Hutcheson

Nov 30 2021 at 6:58am

I am surprised to have to make the same remark about one of your posts as I would about the solecisms of some NYT pundit. It makes no sense to speculate about future inflation without explicitly speculating about what the Fed will do. Maybe the Fed will continue to delay dialing back and revising its QE and you will be right. I think the run up in the TIPS in September was a clear indication that it was time to start getting caught trying to reduce inflation. Personally, I have some hopes that the Fed will do this and that you will be wrong (the sooner the Fed gets inflation back on target, the better for Democrats :)). But right or wrong it depends on what the Fed does.

Philo

Nov 30 2021 at 10:36am

Obviously, Sumner is implicitly speculating about what the Fed will do. There is nothing nonsensical about doing this.

Jon Murphy

Nov 30 2021 at 4:38pm

Philo’s right. Any sort of prediction (or policy suggestion) carries with it implicit assumptions about behavior, even if nothing else than ceteris paribus. That’s a point economists (and other scientists) have been making since Adam Smith in the Theory of Moral Sentiments. Indeed, it’s so common that it’s typically in intro economics textbooks.

Personally, that’s why I like mathematical economics. Mathematics teases out one’s implicit assumptions and makes them explicit.

Scott Sumner

Nov 30 2021 at 10:23pm

I agree that it depends on the Fed; I’m merely describing current market expectations.

Roger Sparks

Nov 30 2021 at 11:17am

The standard AS/AD model gives me fits due to its treatment of time. Here we see the Y2 position (which is later in time) to the left of Y1.

Now it seems to me that demand has stayed high during the course of the pandemic due to the introduction of new demand (which came in the form of a gift of money).

If all players agree as to the cause of steady demand, then we should be able to forecast that there is too much money in the economy to expect normal (without covid) demand going forward, so an increase in prices (to reduce demand) is warranted.

Is the problem this: the standard AS/AD model is a predictive device rather than a reporting device?

Scott Sumner

Nov 30 2021 at 10:28pm

An increase in price doesn’t reduce demand, it affects quantity demanded.

Floccina

Nov 30 2021 at 11:21am

Great post.

JoeMac

Nov 30 2021 at 2:50pm

Hi Scott.

My knowledge of this comes from Mankiw’s macro textbox.

1. He starts with MV=PQ and uses this to form the AD/AS lines on a graph with a vertical Price Level and horizontal Real Income. This is his first model, a quasi-monetarist one, and he shows how the business cycle is fluctuations in these two lines. Then he goes deeper into his model…

2. Then he derives the above AD line using IS/LM to describe fluctuations in AD in more complex ways.

3. Then he derives the above AS line using a model of the labor market with nominal wage rigidity to describe short-run fluctuations in AS in more complex ways.

4. Then he derives the long-run AS line using the Solow model.

5. In each of the above, he is introducing multiple independent but interrelated abstract “markets” (eg. for money, bonds, goods, labor, foreign exchange, capital)

6. All these abstract “markets” are combined at the end into one general equilibrium “uber” model, which is basically the non-DSGE toy model Krugman uses.

You propose replacing this initial MV=PQ graph of the price level and real output with NGDP on the vertical and Real Output on the horizontal. I like that. But I wish to go deeper into your model as Mankiw does after his initial MV=PQ model.

1. Do you view the above representing some kind of abstract “market” too?

2. How do you handle the other markets in your “big” model? eg. for money (to describe inflation), for bonds (to handle liquidity and and fisher effects), for labor (describe why changes in AD cause real output effects), etc….

3. Given #2, how do you combine all these markets into one uber-market? Or do you prefer to reject the GE approach of mankiw in favor of a partial equilibrium approach which keeps all of these markets (money, bonds, labor, etc.) as existing simultaneously but not necessarily explicitly interrelated in some clear mathematical fashion?

Best.

Joe

Scott Sumner

Nov 30 2021 at 10:27pm

I have some earlier posts that answer your questions in more detail.

JoeMac

Dec 6 2021 at 3:07pm

Are you able to point me to them? Or, alternatively any good “keywords” I should search on EconLog and at the MoneyIlluion blogs?

Philip George

Nov 30 2021 at 9:56pm

The error you are making is to assume that all inflation is caused by movements of the aggregate supply and aggregate demand curves.

Consider a country that imports 1,000 barrels of crude at $50 a barrel. Then, OPEC doubles the price of crude to $100 a barrel. If the country required $50,000 to buy crude earlier it will now need $100,000. If the central bank of the country permits the expansion of money supply to that extent then the country will have inflation but no reduction in growth. If the central bank squeezes money supply growth then it will have both inflation and a reduction in GDP growth (or what we would term stagflation). In this case the reduction in growth would be the result of the central bank’s failing to allow money supply to increase to the required extent to permit the purchase of the same amount of crude oil as before.

The inflation is not the result of a relative shift in the demand or supply curves.

The US is not a net importer of oil now. But if OPEC raises the price of crude then domestic producers too would raise the price. The resulting inflation would not be a consequence of a relative shift in supply or demand. Both the demand and supply curves, measured in nominal terms, shift.

Scott Sumner

Nov 30 2021 at 10:26pm

The scenario you describe is easily explained in the AS/AD model, so I have no idea what you are referring to.

Philip George

Dec 1 2021 at 4:33am

OPEC doubles the price of crude oil. What happens to the aggregate supply and demand curves?

Scott Sumner

Dec 1 2021 at 12:08pm

AS shifts left. That example is in all the textbooks.

Sven

Dec 1 2021 at 7:16am

Prof. Sumner,

I think nominal spending (aggregate expenditures, aggregate demand, nominal GDP) are the same things. And real output(real GDP, aggregate supply) are the same things.

Aggregate supply is determined by factors of production not by aggregate demand. Aggregate demand may be below or above the trend in the short term. This is called business cycle fluctuations. It just temporarily affects aggregate supply. Therefore, economic growth is not determined by aggregate demand unless there is no problem in credit mechanism. So long as credit mechanism works the aggregate supply will be at the trend line in the long run. This is a clarification for Investopedia’s word salad.

“With that framing, the Covid economy is much easier to explain. Over the past two years, nominal spending has grown at a normal rate, whereas real output has been depressed by structural problems. Going forward, nominal spending over the next year is likely to be too high to maintain an average inflation rate of 2%. If I am correct, then by the end of 2022 we will have had a period of elevated inflation associated with both above normal nominal spending and structural problems in production.”

When it comes to above reasoning, I think persisting structural problems, uncertainty over covid, and FED’s unpredictable policies it is very ambiguous to make a prediction. 🙂

Scott Sumner

Dec 1 2021 at 12:10pm

“This is a clarification for Investopedia’s word salad.”

Investopedia is saying that AD is equal to real spending. Go to the link and read the whole thing.

rsm

Dec 1 2021 at 7:42pm

《our economy cannot suddenly turn on a dime and produce far more goods and far fewer services.》

《structural problems in production.》

Does capitalism fail to allocate surplus efficiently? Why destroy demand through prices (unless for ethical reasons, like cornering meat and lumber futures to raise their price to Not For Sale)? Can individuals do a better job of self-provisioning than markets? Can we at least test the latter, with an inflation-proofed basic income and more access to commons to practice usufruct upon?

Spencer Bradley Hall

Dec 2 2021 at 9:03am

Contrary to economists, supply and demand schedules are not linear – as the price elasticity of demand clearly demonstrates.

re: “Nominal GDP and real GDP most certainly do not “share the same calculation”.

Contrary to economists, the inflationary gap is perpetrated by the Reserve and commercial banks expanding credit. Whereas non-bank lending is non-inflationary. The solution to secular stagnation, the decline in the velocity of circulation in the circular flow of income, is to drive the banks out of the savings business.

Comments are closed.