I’m not the person you’d want writing an obituary. In my view, the “Great Man” view of history is mostly inaccurate, and at a more personal level I’m skeptical of the entire notion of personal identity. Thus what we think of as “Paul Volcker” may have little correlation with Volcker’s actual lived experience, or his impact on society.

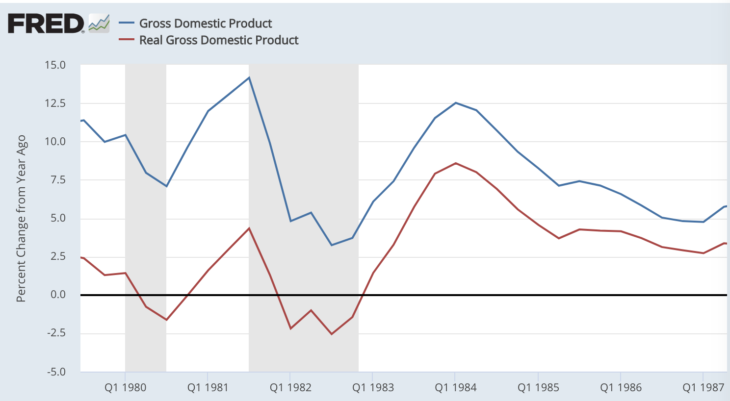

Nonetheless, by conventional standards Paul Volcker was unquestionably a Great Man, and one with positive influence on society. Here is nominal and real GDP growth (12-month rates) during his years as head of the Federal Reserve:

The period almost perfectly illustrates Milton Friedman’s view of macroeconomics. Consider:

The period almost perfectly illustrates Milton Friedman’s view of macroeconomics. Consider:

1. Friedman said that nominal shocks drive the business cycle, but have almost no long run impact on real variables. Here you see a strong short run correlation, but longer term you see stronger real growth in Volcker’s last 4 years, despite weaker nominal growth. The gap between the two lines is inflation. When Volcker brought down inflation, unemployment initially increased and then fell back to the natural rate. Real GDP initially declined, and then recovered strongly as the labor market adjusted to lower inflation, to lower NGDP growth. This is Friedman’s Natural Rate Hypothesis.

2. Inflation fell sharply during the 1980s despite fiscal policy becoming far more expansionary. This confirmed Friedman’s view that monetary policy drives inflation, not fiscal policy. It led to the New Keynesian revolution, which gave the Fed responsibility for determining the path of demand.

3. Volcker’s tight money policy caused interest rates to rise for a few months in late 1979-80, and then again in early 1981. In both cases, interest rates subsequently fell sharply. Recall that Friedman argued that low interest rates were a sign that money had been tight. (Emphasis on past tense.)

4. Money velocity fell sharply as inflation declined, just as Friedman predicted.

Of course most of these insights are now in the process of being lost. I recently spoke with a student who took an intermediate macro class at an elite university. None of these Friedman insights were covered. The course was almost 100% vulgar Keynesianism—one expenditure “multiplier” after another, with virtually no discussion of monetary policy. I was told that the professor didn’t “believe in” monetary policy. Students weren’t even told how central banks target inflation.

As the lessons of the Volcker era are being forgotten, we are entering a new Dark Age. Here’s the WSJ:

In the Next Downturn, Fiscal Policy May Have to Step Up

Sigh . . .

READER COMMENTS

Dylan

Dec 9 2019 at 12:14pm

If it is any consolidation, I don’t think that is a new phenomenon. I wasn’t at an elite school, but I don’t recall any sort of monetarist curriculum in my intermediate macro class from 15 years ago. And that wasn’t driven by the ideology of the professor, who was definitely more conservative than most. There were hints that he wasn’t a Keynesian in his answers to some questions, but the course itself was pretty much entirely Keynes, and we only looked at fiscal levers. I had a separate Money and Banking class where we talked about the Fed, but not really from a macro perspective if I recall correctly.

Dylan

Dec 9 2019 at 3:01pm

Yikes! That should of course read consolation. I don’t think I can even blame autocorrect for that mistake. Just too much M&A on the brain.

Brett

Dec 9 2019 at 12:25pm

Volcker may have had a significant role in bringing down Communism at the end of the 1980s. It gets less attention than the Third World Debt Crisis of 1982, but the Warsaw Pact countries had also borrowed heavily in the 1970s and found themselves in deep trouble in the early 1980s once they could no longer borrow for imports.

Scott Sumner

Dec 9 2019 at 2:39pm

Dylan and Brett, Good points.

Thomas Hutcheson

Dec 10 2019 at 6:40am

Congress gave the Fed a mandate to determine the path of demand by creating a dual mandate of stable prices and low unemployment.

Scott Sumner

Dec 10 2019 at 8:41am

Yes, that was a part of the New Keynesian revolution.

Lorenzo from Oz

Dec 10 2019 at 4:19pm

That is great use of clear data to teach points in a transparent way.

Mark Bahner

Dec 10 2019 at 10:40pm

What do you reckon that means, deficit-wise? $1.5 trillion per year? $2 trillion per year? More?

Scott Sumner

Dec 11 2019 at 11:19am

I am quite confident that fiscal policy will NOT be effective in the next downturn. Even a deficit of $2 trillion would not significantly move the needle. Nonetheless, I imagine they will try some fiscal stimulus, and the economics profession will simply assume that it worked, regardless of the outcome (much like in 2009.)

Matthias Görgens

Dec 12 2019 at 1:22am

Scott, how does ‘low interest rate are a sign that monetary policy had been tight’ gel with everything being about expectations and anticipation in the financial markets?

Does past tight policy just change what we can rationally expect? Or is the interest rate sticky?

Scott Sumner

Dec 12 2019 at 1:15pm

Matthias, Low rates usually reflect low NGDP growth, which results from a previous policy of tight money.

Comments are closed.