This caught my eye:

Taiwan kept borrowing costs unchanged and raised its growth forecast for the year in a rare display of optimism in a world grappling with the economic effects of the pandemic.

The central bank’s decision to hold the interest rate reflects confidence in an economy where the stock market is near a record high, exports are booming and the Covid-19 pandemic is being held at bay.

The economy is now expected to grow by 1.6% this year — up from June’s 1.5% forecast — driven by government spending and private investment as supply chains get relocated from China, central bank Governor Yang Chin-long told reporters Thursday.

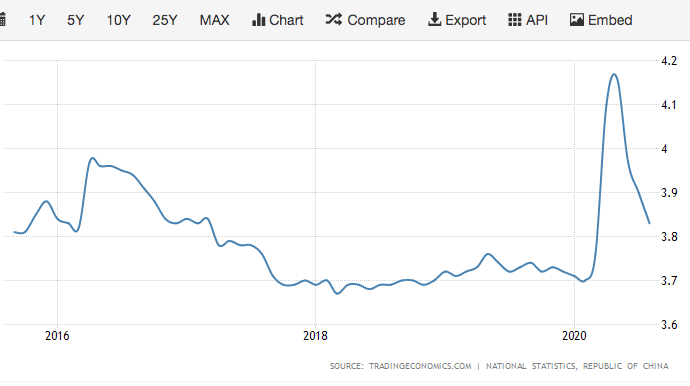

You might argue that 1.6% RGDP growth is not a boom. But consider that Taiwan’s population growth rate is only 0.2%. A growth rate of 1.4% in per capita terms is fairly normal for a rich economy like Taiwan. And notice that while the unemployment rate briefly spiked during the Covid crisis, it’s rapidly plunging back toward the 3.7% level of the 2018-19 boom.

Meanwhile, China’s export machine is reaching new all-time highs:

Note that while the graph title says “imports”, the graph actually shows China’s share of global exports.

The WSJ reports that China’s domestic economy is also doing well:

China’s economic recovery accelerated in August, with retail sales, the last holdout among the economy’s major components, returning to pre-coronavirus levels by showing their first month of growth this year.

Other major indicators, including factory production, investment and property activity, all gathered pace, China’s state-run statistics bureau said Tuesday, signaling a robust rebound for the world’s second-largest economy. The main official measure of joblessness, the urban surveyed unemployment rate, edged down to 5.6%, the lowest since it stood at 5.3% in January, when the coronavirus began to affect hiring. That is comfortably below the government’s targeted ceiling of around 6% for the year and down from the record high of 6.2% in February.

What lessons can we draw from this information?

Lesson #1: Early in the crisis, we were told of a “trade off” between health and the economy. Taiwan has done better than almost any other place on earth in terms of containing Covid-19, and its economy is outperforming almost all other developed economies. It turns out that controlling the epidemic is a good way to avoid an economic disaster.

Lesson #2: Early in the crisis, especially before Covid-19 spread to other countries, we were told that Covid was a huge blow to the Chinese economy and that the economic center of gravity would shift a bit toward other Asian economies like India and Vietnam. Very few people, if any, predicted that China’s share of global exports would rise sharply in 2020. One should always be suspicious of predictions of the end of the Chinese boom, which have been consistently wrong for nearly 40 years.

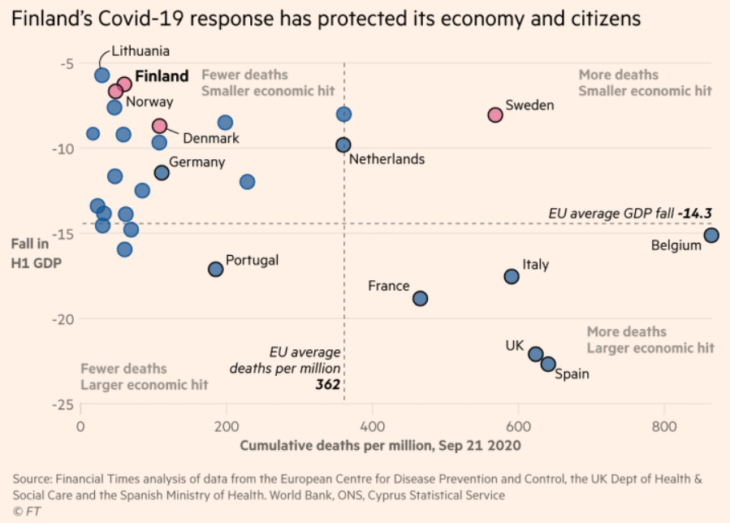

Of course it’s possible that these two countries are outliers. But this graph in the FT suggests that if anything there’s a slight negative correlation between economic growth and fatality rates. Growth is a bit higher, on average, in countries with fewer deaths:

Sweden gets a lot of attention, but it’s something of an outlier.

READER COMMENTS

stoneybatter

Sep 24 2020 at 4:58pm

I am struck by the fact that the bottom half of that final chart, i.e. the countries with the worst growth performance this year, is dominated almost entirely by euro area countries (the UK is the only exception). Can’t we just apply Occam’s Razor: countries that have fixed exchange rates suffer from a lack of control over domestic macroeconomic outcomes.

ECB policy is too tight for those countries and they are seeing deeper contractions. There’s no mystery, and no need to include covid deaths in the analysis.

If those dots were a few percentage points higher, then maybe the relationship between growth and covid deaths would look positive and upward-sloping. Your reasoning for why there shouldn’t be a tradeoff between the two is compelling though, so I don’t really know what to make of that counterfactual.

Scott Sumner

Sep 24 2020 at 7:58pm

That’s a good point, although I suspect that even if you restricted the analysis to only eurozone countries you’d still have a mildly negative relationship. Germany and Finland are also in the Eurozone, for instance.

But yes, I wouldn’t put too much weight on that graph, as there are a very limited number of independent observations.

Tom S

Sep 24 2020 at 7:47pm

The chart is misleading and confuses correlation with causation. Its the lockdowns that caused the majority of economic downturn, not the virus per se. Hence what we see is a chart tracking how much of a lockdown was enforced by the local government. Spain, UK, France and Italy all had an insanely strict lockdown. Germany’s was quite lax and Sweden only enacted restrictions on large gatherings.

Plus even countries like Sweden have suffered due to restrictions that their neighbors enacted, as the economies are heavily intertwined. And finally – COVID death rates are not final yet. The vaccine is at least 6 months away from mass deployment and winter is coming.

Phil H

Sep 25 2020 at 3:04am

“Early in the crisis, we were told of a “trade off” between health and the economy.”

I’m afraid that message came mostly from places like this website. Most politicians didn’t spread that message. Even most economists quickly did calculations that demonstrated stopping the epidemic would be by far the least costly option, even if it required a major lockdown. It was only a few ideologues like our very own David Henderson here who relentlessly pushed the idea that lockdowns were bad for the economy.

I think outside of this little bubble, it was obvious to everyone that a short, effective lockdown would be a good solution. Obviously the Taiwan and New Zealand solutions were even better, but perhaps not feasible for countries with more international through-traffic.

That aside, I agree with everything else in this post.

robc

Sep 25 2020 at 11:04am

I haven’t seen a single calculation that demonstrates that. Every one I have seen has demonstrated that based on value of life calculations the number of lives that would need to be saved would have to be astronomically unlikely to make a lockdown worth doing.

Phil H

Sep 25 2020 at 9:43pm

Here’s one

https://promarket.org/2020/03/13/captured-western-governments-are-failing-the-coronavirus-test/

And here’s Henderson criticizing it

https://www.econlib.org/end-the-lockdowns-now/

robc

Sep 26 2020 at 8:05am

You can see my comment on the Henderson thread critical of the dollar choice in the original article.

Scott Sumner

Sep 25 2020 at 2:12pm

My view is that too much weight is put on the lockdown issue (Taiwan did not do a lockdown), and too little on issues like masks and testing.

Unless I’m mistaken Germany did much better than the other big European countries because it tested more effectively, not because it had a stricter lockdown.

Michael S.

Sep 25 2020 at 5:10pm

we didn’t have a formal lockdown, but streets were empty and everyone who could worked from home. Gatherings of people were not permitted.

Can’t say I noticed that much testing, but it certainly wasn’t a problem to get tested.

On the whole, I’d say a mix of luck and state capacity

Scott Sumner

Sep 28 2020 at 12:59pm

You said:

“but it certainly wasn’t a problem to get tested.”

I read dozens of articles suggesting that there was a shortage of tests during the crucial period when pandemic was spreading rapidly. So I don’t believe that is accurate.

Tomas

Sep 25 2020 at 4:46am

I looked at lockdown stringency in ourworldindata for the European countries above. It seems like there is a negative correlation between lockdown stringency and economic growth and then Sweden is not much of an outlier. Taiwan, incidentally has lower lockdown stringency than Sweden.

robc

Sep 25 2020 at 7:35am

Sweden was something of an outlier because they were something of an outlier.

The counterfactual question is, if Sweden had adopted the standard policies that the rest of Europe did, would they have been grouped with Norway/Finland/Denmark or with UK/Spain/Italy? Or somewhere else?

The standard argument is between those who think they would have shifted hard left and those who think they would have shifted hard down. I think Portugal is another legit answer. Maybe Belgium too, but not sure I could explain that one in any logical way. Then again, I have yet to hear anyone comment on Belgium’s number is any kind of rational way.

Scott Sumner

Sep 28 2020 at 1:00pm

There are news reports that Belgium uses a more expansive definition of Covid deaths, which explains their high death rate.

Lizard Man

Sep 25 2020 at 2:22pm

Doesn’t China’s urban unemployment rate exclude from calculation citizens who don’t hold urban hukou’s? I guess Taiwan’s data does bolster the case that China’s economy is returning to its pre-Covid conditions, but China’s unemployment numbers aren’t really comparable to those of other nations. And I am not sure if workers in China who don’t have urban hukous have enough purchasing power to move retail sales around that much. They likely should, even with relatively low wages, but I haven’t seen the tabulation.

Scott Sumner

Sep 26 2020 at 12:05pm

Yes, the unemployment data is questionable. But there is evidence from things like traffic congestion that things are back to normal. My wife’s in China right now, and says things seem as busy as ever—no sign of social distancing.

Comments are closed.