As I write this, much digital ink is being spilled on inflationary pressures from Trump’s latest round of tariffs on Mexico, Canada, and China. These are our three biggest trading partners, representing vast amounts of goods over many industries and sectors, affecting both American consumers and American firms alike. Price concerns are legitimate. But we must differentiate between changes in prices and inflation. Tariffs will cause a one-time increase in prices, but all else held equal, prices will not continue to rise. The 2018 tariffs on washing machines present a good example.

In 2018, President Trump imposed tariffs on washing machines. Prices naturally jumped in 2018, both on the consumer side (as measured by the CPI) and the producer side (as measured by the PPI). The full amount of the tariff was passed along to Americans. After this initial jump, however, prices returned to the long-run trends of generally falling. Tariffs did not cause a long-run increase in prices. Once the tariff was fully capitalized into the price, market forces once again took over and the long-run trend returned. This is exactly what we should expect. A tax shifts the curves, causing a one-time jump in the price, but then once the shock passes, the long-run trend resumes.

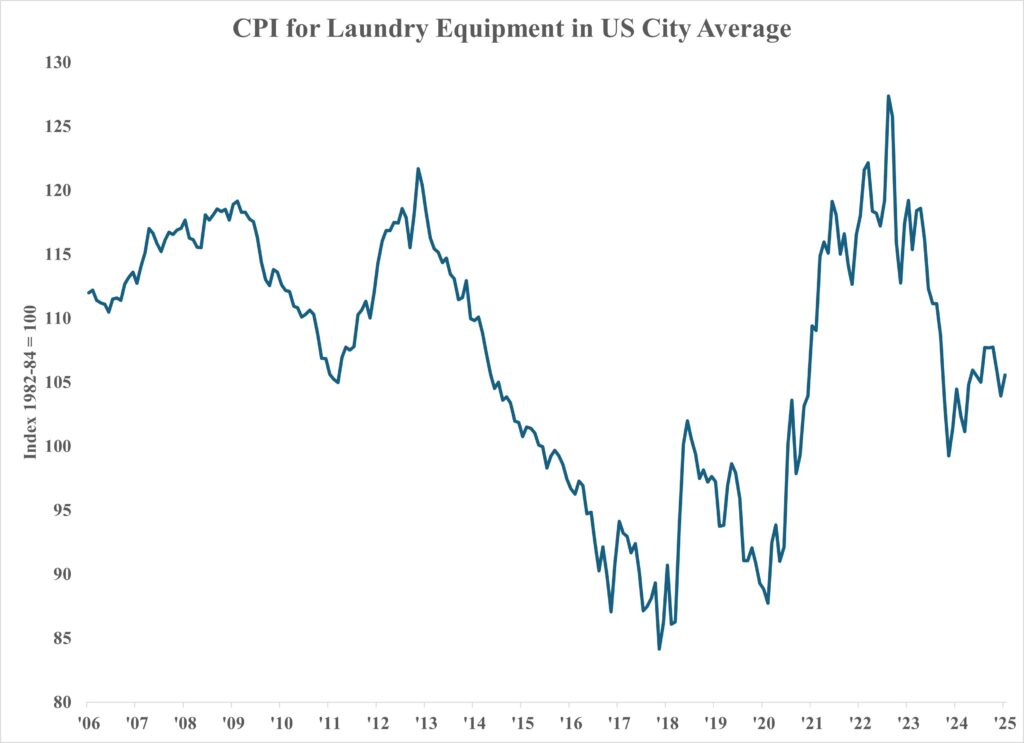

This is a chart I created from the Consumer Price Index of Washing Equipment (source: Bureau of Labor Statistics, series ID: CUSR0000SS30021):

Note that, starting in 2013, washing machine prices started falling, a trend that would be uninterrupted until the tariffs were imposed in 2018. The tariff was imposed and prices jumped. Once the tariffs were fully incorporated in prices by the end of 2018, the trend resumed. Then, of course, 2020 hit and, with inflation, the trend was reversed. It’s quite easy to see with this chart that tariffs didn’t reverse the overall trend, but it did shift the trend upward. Consumers still saw washing machine prices fall, but prices were still higher than they otherwise would have been without the tariff.

Fast forward to 2025. We should expect to see these new broad-based tariffs cause a near-term increase in prices. Given the broad nature of these tariffs, the increase in costs to both consumers and producers will likely even show up in inflation figures temporarily. But it would be a mistake to call these tariffs inflationary. The tariffs will be incidental to any inflationary pressures, not causative. The Federal Reserve’s bloated balance sheet will be a primary cause of inflation.

READER COMMENTS

Thomas L Hutcheson

Mar 21 2025 at 9:30pm

Please explain the exact size of the head of this pin.

Some shock sharply rearranges the pattern of supply and demand. To maintain full employment of resources relative prices have to change. But some prices do not change downward very easily. (The Atlanta Fed even does an index of “sticky ” prices) Therefore to prevent a lot of markets from not clearing the Fed will want to engineer enough over target change in the price level to allow the relative prices to adjust. Maybe this will take 3, 5, 7, 9 quarters — who knows — to run the rate of increase on the price level up and then bring it back down.

Did we have inflation or a one time increase in the price level? How many quarters of a rate of increase greater than the Fed’s target have to go on to be called “inflation?”

Why should we care? Who should do what to whom if this is called “inflation” instead of a one-time change in the trend of the price level?

Jon Murphy

Mar 22 2025 at 8:20am

It seems to me that if we just stick with the typical definition of inflation, of general price rise, then all your questions are answered. I don’t think we should define inflation relative to what some central bank does.

Thomas L Hutcheson

Mar 22 2025 at 3:35pm

??? You are the one who suggested that whether an increase in the price level is “inflation” or not depend on how long it goes on. I just spelled out a scenario of rise and fall in the rate of change of the price level to try to clarify your concept.

But ultimately why do you care? To repeat, “Who does what to whom under one definition of “inflation” or another?”

Jon Murphy

Mar 23 2025 at 11:56am

Oh! I’m sorry, I misread your initial comment. I see your point now.

In the situation you describe, I would say there is inflation. There is a general rise in the price level after all.

My point in this post, unclearly stated, is that a tariff will not cause long-term inflation. There would be a quick jump in prices as the supply (or demand) curve falls, but then (all else held equal) prices won’t change. Any changes in price after the tax has been fully incorporated is due to factors unrelated to the tariff.

A secondary, esoteric point was a response to claims made by some that the washing machine tariffs reduced washing machine costs. They simply look at two points, see one is lower than the other, and conclude that the tariff is the cause. I’m discussing that’s not true because the trend line has shifted upward.

Richard W. Fulmer

Mar 21 2025 at 11:56pm

Left free, actors in the market tend to find increasingly efficient ways to produce goods and services. Raising tariffs restricts freedom, tending to make markets less efficient and resulting in a smaller Q. If P=MV/Q, wouldn’t a smaller Q result in a bigger P?

Jon Murphy

Mar 22 2025 at 9:27am

All else equal, yes. But it’d depend on changes on Aggregate Demand as well

Thomas L Hutcheson

Mar 22 2025 at 6:09pm

Welcome as a regular EconLog blogger!

Mactoul

Mar 23 2025 at 3:48am

Michael Lind in Tablet magazine (7 March 2025)

“The claim that tariffs are inherently misguided and inevitably harmful does not stand up to scrutiny. The verdict of history is clear. No country ever industrialized by pursuing free trade. Britain in the 18th century and the U.S. and Germany in the 19th century went from being agricultural backwaters to industrial great powers thanks to tariffs, while Japan and South Korea and Taiwan and China have developed with functionally equivalent nontariff barriers protecting their own infant industries and reserving their own home markets for their producers.

No less an authority than Adam Smith, the patron saint of free marketeers, supported the use of tariffs to retaliate against foreign trade restrictions:

Decisions about whether to use tariffs as bargaining chips, Smith believed, should not be guided by general rules, and should be left to the discretion of policymakers in the executive branch:

john hare

Mar 23 2025 at 4:28am

History is full of examples of examples of an industry being protected until if fails. Competitive pressure gone, and all too often that group gets “fat and lazy”. Much the same effect as some unions that protect their members to the point that the whole enterprise goes away. To say that tariffs created the industrial state is to confuse correlation with causation.

Mactoul

Mar 23 2025 at 7:15am

History is large and contains multitudes. For any policy pro and contra examples could be found.

But the fact remains, that industrialization went together with protection and tariffs.

Jon Murphy

Mar 23 2025 at 7:55am

Again, the fact is the other way ’round. Industrialization tends to occur when tariffs are falling.

Jon Murphy

Mar 23 2025 at 6:20am

Two quick things:

1) Lind’s history is backward.

2a) Smith’s hypothetical has a huge conditional attached to it. Indeed, you should read the rest of the paragraph where that sentence comes from.

2b) Your second Smith quote is not about the “discretion of the executive branch.”

Mactoul

Mar 23 2025 at 7:11am

More Lind:

The Chinese import threat is why Canada has levied a 100% tariff on imported Chinese EVs, along with a 25% surtax on Chinese steel and Chinese aluminum. The European Union has slapped electric vehicles made in China with tariffs ranging from 7.8% to 35.3%, on top of the standard European tariff of 10% for imported automobiles. India imposes tariffs of 70%-100% on imported electric vehicles from China and other countries.

Jon Murphy

Mar 23 2025 at 7:57am

Do you have a comment on the topic of the post or not?

Richard W Fulmer

Mar 23 2025 at 10:28am

Tariffs weren’t the only things affecting America’s economy in the 19th century: About 30 million people immigrated to the country; in times of peace, the federal government spent less than 2% of GDP, compared to 25% today; the government’s regulatory footprint was much smaller; the country operated on the gold standard, keeping inflation in check; and massive technological advances transformed the economy – steam power, railroads, the telegraph, mechanized farm equipment, the Bessemer process in steel production, petroleum refining, the sewing machine, refrigerated railcars, and electric power and lighting.

Singling out tariffs as the primary cause of the country’s explosive growth during the 1800s is hardly reasonable.

Comments are closed.