Scott Sumner’s post Tariffs and the Economy observes that the most important effects of tariffs are not big, dramatic, or immediate ones. They’re the hits to long-term growth as arrangements gradually become less efficient and lower growth rates compound.

The lack of an immediate, catastrophic outcome could be used as an excuse to dismiss tariffs as not that big a deal. Even at the point of the biggest market losses after the Rose Garden tariff announcements, the S&P 500 was at far higher levels than it had been five years prior. A year’s lost wealth is a tragedy. Increasing wealth increases our potential to save and improve lives. But it’s true that the United States was quite rich five years ago and remains quite rich now.

This called to mind the ‘Brexit: Five Years Later’ takes in 2024. Brexit was the withdrawal of a smaller economy from integration with a large common market—essentially, introducing trade barriers.

In spring 2016, the UK Treasury forecast an “immediate and profound” recession if Brexit passed. When this didn’t happen, supporters of Leave started mocking “Brexit doom”, dismissing concerns that there would be a dramatic economic cost of leaving the EU. Aside from the general rule that shrinking the market makes us poorer (or we know almost nothing about economics), those dismissing the cost would have benefited from the more specific lesson in point three of Scott’s post:

And then, from points four and five:

4. The most important economic impact of tariffs is on long run economic growth. (There are other non-economic impacts, such as increased risk of war.

5. Most economists do not overestimate the impact of tariffs on long run growth.

Finally, the reminder that “A 0.2% decline in long run growth is far worse than a 2% fall in GDP for a single year.” (Read the whole post for more on the effects of monetary policy.)

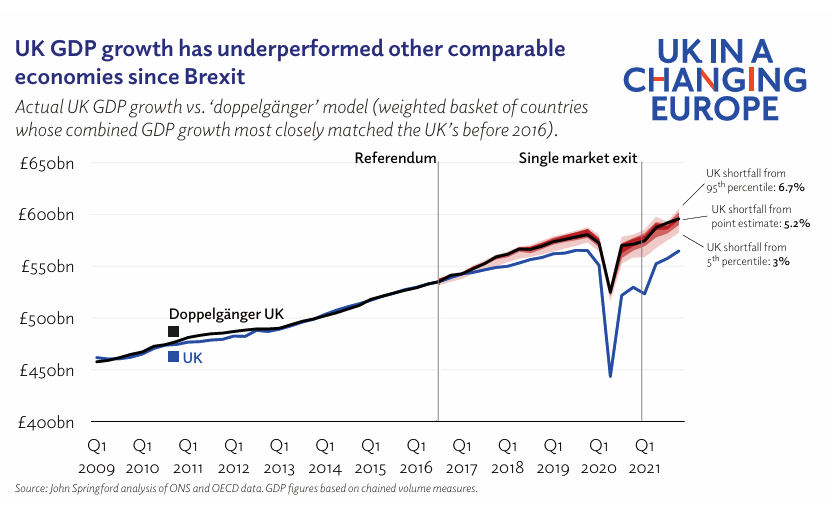

In longer run forecasts of the cost of Brexit, economists seem to have been closer to the mark. By January 2020, GDP was 1–3% lower than it would have been if the UK had not voted to leave the EU. By 2025, productivity is falling, and the UK economy seems to be underperforming in this ‘doppelgangar’ model (which takes the pandemic into account and is the model with the most fun name).

The Brexit Files: from referendum to reset, 28 Jan. 2025

The Brexit Files: from referendum to reset, 28 Jan. 2025

There are obvious differences between the United States and the UK. Probably most significant is the size of their populations and economies—the extent of the U.S. market is bigger to begin with. Brexit is also a harder policy to reverse than tariffs the U.S. president seems able to change on a whim. But the basic principle, the most basic in economics—that the division of labour, limited by the extent of the market, makes us richer—is still the one at play.

Either way, the important thing to remember is that no matter how dramatic the stock market tickers are, they’re not the most important part of the story. Even if all the tariffs were to be called off tomorrow, it’s hard to imagine how the U.S. could restore international trade given the economic uncertainty and political animosity they’ve permanently introduced.

READER COMMENTS

Scott Sumner

May 8 2025 at 4:22pm

Excellent post. Brexit affected both trade and the immigration of skilled labor from the EU to Britain.

Matthias

May 10 2025 at 5:40am

And the Brexit referendum didn’t lead to a recession, because the Bank of England was competent enough to let the exchange rate (and thus in the longer run the price level) take the hit, rather than let NGDP deviate from its trend.

The actual Brexit itself wouldn’t have ’caused’ a recession, because it was long anticipated. (I put ’cause’ in scare quotes, because the hypothesical recession after the referendum result would have been retro-actively caused by the actual exit from the EU. Causality in systems with intelligent actors who can anticipate is weird.)

Monte

May 8 2025 at 5:36pm

While Trump’s tariffs mark a clear turning point in US trade policy, I think it’s overly pessimistic to suggest the damage is irreparable. The way back has been made more narrow, but mutual economic interests remain. Once we get past the negotiating stage, I’m betting markets will stabilize, become more predictable, and good will between the US and our trading partners will be restored.

steve

May 8 2025 at 8:04pm

We can hope so, but did you ever run a business? How many times did you tolerate someone screwing you over before you found someone else to do business with? It’s not really going to be Canada or Mexico that is going to decide if they want to continue to trade with businesses in the US. It’s going to be lots of individual businesses. If the US has a unique market they cant replicate elsewhere they will get over it and trade with us, but if they have other options they wont want to trade with such unreliable partners.

Steve

Monte

May 8 2025 at 9:17pm

No disagreement. Like you say, we can hope to get to the point that these tariffs are lifted and convince our trading partners that we’ll abide in good faith by any future trade deals. The US already has a unique market in that the rest of the world is heavily dependent on us. We have leverage, but risk losing it if we become too isolated or protectionist.

john hare

May 9 2025 at 4:12am

A large part of running my own business is having the ability to fire both customers and suppliers without losing my source of income. I hardly ever burn the bridges, but simply deal with others. A few contactors have tried to dictate my technical methods and now have to use other subs as I walked away. Rumor is that it hurt them a bit. Some suppliers I have dealt with for decades have changed business practices to become less user friendly so I take my business elsewhere, though I do leave those accounts in place if I need them.

I have choices, and millions of other businesses and individuals do as well.

Mactoul

May 9 2025 at 6:09am

Imposing a tariff is a prerogative all countries retain. How is it “screwing you over”?

EU has imposed green import tariffs, known as the Carbon Border Adjustment Mechanism (CBAM), which are designed to ensure that imported goods, particularly those from carbon-intensive industries like steel and cement, are subject to a carbon price equivalent to what EU producers face.

From January 2026, the EU will begin collecting CBAM as an import tariff on these goods.