Most experts seem to believe that our inflation problem is largely caused by supply bottlenecks in everything from food to oil to computer chips. But what if that isn’t true? What if some other factor is the actual cause of high inflation? And how would we know this to be the case?

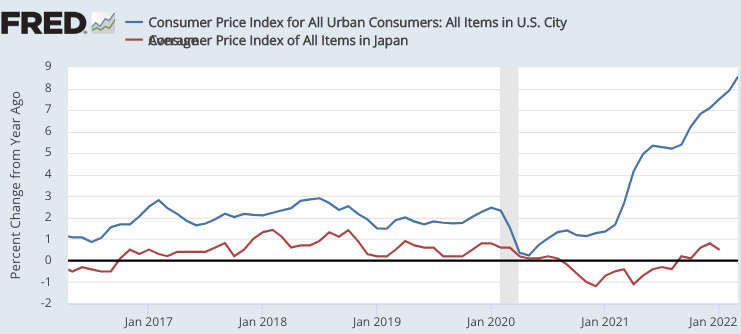

One way of addressing this issue is to look at inflation rates across countries. The following graph shows 12-month inflation in the US and Japan:

Inflation over the past 12 months is running at over 8.5% in the US, vs. about 0.5% in Japan. Admittedly the Japanese data is two months behind, but even their March CPI data is likely to show 12-month inflation at only about 1%. Why is inflation in the US roughly 7.5 percentage points higher than in Japan? Doesn’t Japan also have to pay much higher prices for imported oil?

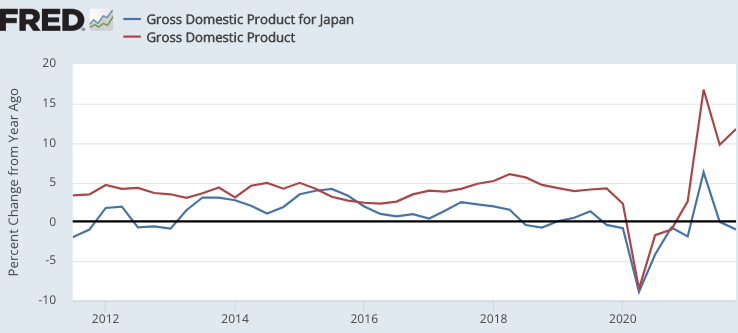

One possible explanation is differences in monetary policy, which is best measured by looking at growth in NGDP. Over the past 4 quarters, NGDP growth is running at about 11.8% in the US versus negative 1% in Japan. Thus looking at monetary policy alone, and completely ignoring supply bottlenecks, one would expect inflation in the US to be about 12.8% higher than in Japan:

Why is US inflation only about 7.5% higher than in Japan, and not 12.8% higher? In an accounting sense the difference is due to greater real GDP growth in the US. That’s not surprising as (in the short run) monetary stimulus doesn’t just boost inflation, it also boosts real GDP. Because the economy in the US has recently overheated, some of that excessive RGDP growth will eventually turn into inflation. Fortunately, a significant portion of the rapid RGDP growth represents recovery from a depressed economy in 2020.

To summarize, the high inflation in the US is mostly due to expansionary monetary policy. Almost any time NGDP grows at 11.8%, you can expect relatively high inflation. That’s not to say that supply bottlenecks have had no impact; even in Japan you can see an uptick in inflation over the past year. But as a first approximation, inflation problems are excessive NGDP growth problems. Stabilize NGDP growth at 4% and the minor blips in inflation we continue to observe will truly be “transitory”.

PS, Strictly speaking, NGDP growth is the sum of RGDP growth and GDP inflation, not CPI inflation. But inflation in the US is much higher than in Japan, however measured.

READER COMMENTS

Thomas Lee Hutcheson

Apr 18 2022 at 2:24pm

“Most experts seem to believe that our inflation problem is largely caused by supply bottlenecks in everything from food to oil to computer chips.”

Summers? Krugman? Furman? DeLong?

Over what time frame would have/would RGDP been/be higher with monetary policy that stabilized NGDP rather than what we have? And if so, which policy instruments should the Fed have moved differently when?

[And the shocks are not just oil prices, the are the whole pandemic induced changes in labor supply and goods/services demand.]

Scott Sumner

Apr 19 2022 at 1:33am

The Fed has several instruments they can use, including quantitative tightening and higher interest on bank reserves. They should have started tightening in the second half of 2021.

I suspect that with sound money the level of RGDP would have been higher in the mid-2020s

marcus nunes

Apr 18 2022 at 4:07pm

You can do a comparison using less extreme examples as Japan. Here´s one:

https://marcusnunes.substack.com/p/the-age-of-inflation-again?s=w

Overall, monetary policy in the US was better. We know that because the recovery was swifter and complete. Alas, nothing is perfect and in mid-21 the Fed “overplayed” its hand, allowing demand to add to the underlying supply side inflation. But there is a “non traumatic” policy available!

marcus nunes

Apr 18 2022 at 8:01pm

The “barking dogs” analogy was made up 10 yrs ago by Nick Rowe when looking at Canada. I illustrated the ides here:

https://thefaintofheart.wordpress.com/2013/09/05/three-dogs-two-didnt-bark/

Jim Glass

Apr 18 2022 at 8:55pm

During the 1973-80 Arab oil embargo years, the surge in inflation here in the USA up through double digits to 13.5% in 1980 was overwhelmingly, near universally, attributed to the quadrupling of the price of oil. What could ya do?

I was converted to monetarism when I saw that during the same period inflation was basically stable in Germany (where the central bank was operating with Weimar memories) and actually fell by 15(!) percentage points in Japan (where the BOJ at the start of the period dedicated itself to slashing 20% inflation).

Matthias

Apr 18 2022 at 9:21pm

That period also has another interesting lesson:

Queues for petrol in the US, including occasionally bouts of violence. And just slightly higher petrol prices in Canada.

Guess which country used price controls?

Lizard Man

Apr 19 2022 at 10:07am

How much of the difference is attributable to the intentions of the respective central banks, and how much to a lack of a swift response when conditions change? Do central banks publish forecasts of NGDP, monetary base, and the velocity of money? It would be nice to know those forecasts, so as to be able to compare the actual numbers to the forecast. That way we could know wha the central bank is doing, instead of merely guessing at it.

Scott Sumner

Apr 19 2022 at 12:32pm

They have forecasts of RGDP and inflation, so it’s possible to roughly infer their NGDP forecasts. (Those forecasts currently suggest excessive NGDP growth over the next year.)

Capt. J Parker

Apr 19 2022 at 10:47am

Great analysis. Of course, it does raise the question of what would the comparison look like with economies not quite as anomalous as Japan always seems to be. Here’s US, Germany, UK and France.

https://fred.stlouisfed.org/graph/?g=Onlq

Dr. Sumner’s conclusion holds up, US inflation can’t be all supply chain interruptions, even if it is a contributor. The interesting thing is that Germany and France are experiencing somewhat different inflation rates. This difference has to be something more than monetary policy given that they are both Euro countries.

The story seems to me to be that in Western economies, the story seems to be that inflation is caused by supply chain bottlenecks, fiscal stimulus and central banks (overly?) cautious about taking any action to offset the the inflationary effects of the first two.

MarkLouis

Apr 19 2022 at 12:47pm

In my opinion, monetary policy needs to be analyzed underneath the political science umbrella going forward. We essentially know what should be targeted and how. But we have no idea how a central bank actually makes its decisions. And those decisions have very large distributional consequences (consider the massive transfer from renters to homeowners over the past few years). Economics as a science has failed to adequately consider the true forces dictating decisions.

There is a clear asymmetry in the Fed’s reaction function. 5y inflation expectations dipped to 1.75% in 2008 and roughly a month later we had our first rate cut and soon thereafter a host of aggressive new policies aimed at fighting “deflation.” This time around, it took over a year for the first rate hike after inflation expectations decisively broke through any reasonable level. And the Fed still talks of “being cautious.” This is not economics – this is politics and favoritism towards certain groups in the distributional game.

Scott Sumner

Apr 19 2022 at 2:22pm

Monetary policy was consistently too tight from 2008 to 2016, so your “true forces” don’t seem very true at all.

MarkLouis

Apr 19 2022 at 3:34pm

There is a big difference between small, gradual undershoots and large, sudden overshoots. We wouldn’t be having this conversation if CPI were 2.3%.

The mystery is not “why can’t the Fed perfectly hit it’s target?” but rather “why is the Fed willing to tolerate an extremely large overshoot and fall further behind each day?” There is a clear asymmetry here, with real repercussions for lots of people, and a paucity of explanations from the “science” of economics.

Scott Sumner

Apr 20 2022 at 12:26pm

There was no small undershoot in 2008-09; Fed policy was way too tight, even further off course than today. NGDP fell 8% below trend.

MarkLouis

Apr 20 2022 at 4:34pm

That pre-supposes we NGDP-target, which I don’t think is the case last time I checked.

Further, CPI is currently ~6% above trend and rapidly rising. That could easily be 20%+ in a few years time, as the Fed falls further behind every day.

MarkLouis

Apr 21 2022 at 9:29am

We wouldn’t be having this chat if inflation were 2.5%. As of now, CPI level is ~6% above trend and rising rapidly. Monetary policy wasn’t perfect 2008+ but they reacted fairly quickly and stayed reasonably close to target the majority of the time. We are in new territory here with the Fed essentially ignoring a very large, and growing, overshoot. Where are the emergency meetings? the aggressive new tools? pushing the boundaries on what the Fed can legally do to get things back to target?

The Fed’s reaction function is asymmetric. Only question is how long it’ll take the economics profession to realize that.

Spencer Bradley Hall

Apr 19 2022 at 1:59pm

If you cut supply, but not demand, then prices rise. But Covid cut supply and its politics raised demand. It’s hard to engineer a worse outcome.

Jose Pablo

Apr 20 2022 at 3:26pm

Where are this “bottlenecks” coming from? If we are talking about “international commerce bottlenecks”, I don’t get the “bottleneck explanation” at all.

Imports amount to just 14% of the GDP (and domestic production should not be subject to international commerce bottlenecks). Canada and Mexico accounts for more than 26% of this total and I guess this two are less subject to this kind of “bottlenecks”.

So around 90% of the products and services consumed in the US, are not subject to “bottlenecks”. On top of that, bottlenecks affecting international trade should also reduce US exports. So, some products should be redirected to the domestic market causing a drop in their prices.

On the other hand, if “products subject to bottlenecks” increase their prices, but the available income remains constant, some other products should see their demand and prices dropping (see Netflix subscriptions).

Can “bottlenecks” really cause any significant inflation (as different from a change in relative prices) at all? What did I get wrong?

derek

Apr 22 2022 at 1:10pm

If you want a specific materials shortage, the stricter covid lockdowns in Asia have had a huge impact on the global supply of chips, creating a specific bottleneck in car manufacturing and keeping supply low.

As far as shipping within North America goes, there have been huge issues with ground transportation, especially trucking.

Jose Pablo

Apr 23 2022 at 9:28am

But all the “globally supplied affected by lockdowns in Asia” items weight less than, let’s say, 7-10% of the GDP.

And the effect should be partially compensated by made in America items “redirected” to the domestic market and by a reduction in the demand of “non subject to lockdowns” products and services (assuming the “available income” remains constant).

Without relaxing this last assumption, it is difficult to see (at least for me) why the impact of lockdowns should drive inflation up by that much.

Comments are closed.