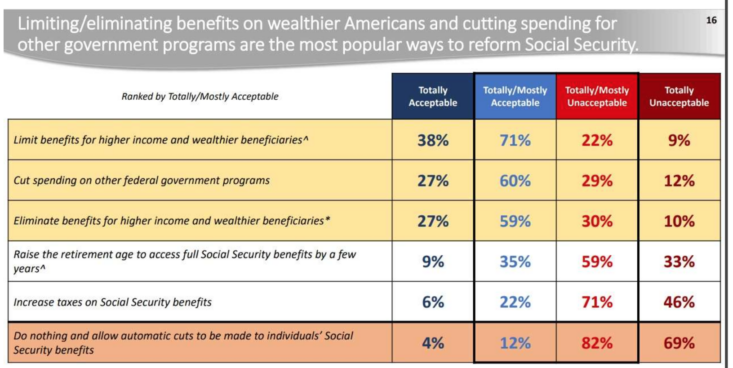

A recent Reason magazine article included a poll on how the public would like to address the Social Security crisis:

In other words, most people don’t want to sacrifice anything; they want someone else to bail out the troubled program. What a surprise!

This reminded me of a famous parable:

In Aesop’s original fable the grasshopper spends the entire summer chilling out, while the ant works to store up food for the winter. Long story short, winter comes, the starving grasshopper begs the ant for food, the ant refuses because the grasshopper was lazy, the grasshopper dies, and we all learn about the value of hard work and long-term planning.

When I see this sort of poll my initial (visceral) reaction is that those spendthrift grasshoppers that didn’t save very much wish to take away the social security benefits of thriftier people (like me.) But I doubt whether these answers can be trusted. I doubt whether people understand that limiting the benefits of wealthy people would only make a dent in the problem if “wealthy” were defined to include “middle class people who were thrifty”. There aren’t many truly wealthy American retirees, but there are a whole lot of middle class retirees with substantial 401k plans (like me.) That’s an influential political bloc, and won’t take kindly to major cuts in their social security. It’s not politically feasible to take away the social security benefits of the top 20% of retirees—they are too powerful. Perhaps you could give then a 10% haircut, but that wouldn’t be enough to solve the problem. We need some combination of more immigration, higher tax rates and/or cuts in other federal programs.

In practice, I suspect that the actual reforms will include a mix of current tax increases and benefits cuts that are pushed well into the future. Young people will pay the price, but as we saw with the 1983 reforms, young people don’t care very much about benefit cuts that won’t take effect for 30 years.

Also keep in mind that many benefit cuts are disguised tax increases. Restricting benefit cuts only to wealthy people is equivalent to a tax on wealth creation. It would represent a rise in the implicit marginal tax rate on income and saving.

READER COMMENTS

robc

Nov 8 2023 at 10:35am

I mentioned on another thread yesterday that I favor raising the benefit age. Keep raising it slowly until SS is effectively eliminated.

I didnt see “End Social Security” as a polled option.

As an aside, since it is top of mind with yesterday being election day, any claims that Polis is some sort of libertarianish democrat ended with his support of Prop HH. Which fortunately went down in flames.

Scott Sumner

Nov 8 2023 at 10:54am

“any claims that Polis is some sort of libertarianish democrat ended with his support of Prop HH.”

Wrong. All governors have hundreds of anti-libertarian positions. To say someone is relatively libertarian is to say it’s in the low hundreds, not the high hundreds.

robc

Nov 8 2023 at 11:47am

Prop HH doesnt just count as one. It would have gutted the entire concept of TABOR (Taxpayer Bill of Rights). It would have ended any reasonable restraint on state spending. If he was some sort of libertarianish democrat, and as leader of the state party, he would have stood up to his party members who forced this onto the ballot at the end of the last legislative session instead of supporting it. He is popular enough, he could have threatened to support primary opponents who aren’t actively trying to gut TABOR every election.

I have seen no evidence of him being anything other than a mainstream democrat on economic issues. He isn’t an insane progressive, but that doesn’t make him remotely libertarianish. He doesn’t get any credit for social issues, that just makes him a mainstream democrat.

robc

Nov 8 2023 at 11:59am

In case anyone thinks this is silly, it really isnt. HH only got a 39% YES vote. It probably barely got a majority among democrats. YES barely carried Denver County. YES dominated in Boulder County, but yeah, the strategy wouldn’t be successful there. YES also won in 3 teeny counties. The rest of the state voted NO. Even Larimer Co was 60% YES.

There would be a lot of democrats in trouble if they had a pro-TABOR but otherwise mainstream democrat opponent who had support from the popular Governor. And there are a lot of pro-TABOR dems, obviously.

Scott Sumner

Nov 8 2023 at 1:09pm

“I have seen no evidence of him being anything other than a mainstream democrat on economic issues.”

No evidence?

Sorry, but that’s just silly:

https://www.denverpost.com/2021/08/30/jared-polis-no-state-income-tax/

https://www.fortmorgantimes.com/2023/05/02/colorado-legislature-zoning-democrats-polis-land-use/

robc

Nov 8 2023 at 4:19pm

The first link sounds good, but then why does he keep supporting tax increases?

Which is it?

And the second link was paywalled so could only get a quick glimpse, but how does the House Democrats agreeing with him make him anything but a mainstream democrat? Unless you think the House Dems are all libertarian too? I mean, yeah, it was a good proposal, but zoning reform doesn’t seem to be a particularly partisan issue in general, it seems its supported and opposed all across the spectrum. And which axis of the Nolan Chart does zoning go on?

Also, last year, during election season, he favored the tax decrease proposal (good!!) and favored sending the TABOR refund evenly instead of as a tax refund (boo!!). On either one (or maybe both), you could argue he was just pandering for votes.

Now that he has been reelected, I think his support for HH speaks volumes.

Scott Sumner

Nov 9 2023 at 1:57pm

So many Democrats opposed him on zoning reform he was unable to get it passed. It’s certainly not a universally accepted Democratic idea.

Ditto for eliminating the income tax. So many Democrats oppose the idea he can’t get it implemented.

Mark Z

Nov 8 2023 at 10:48pm

So young people with jobs can spend the next 40 years paying taxes for a benefit gradually receding away from them that they will never benefit from, while the already old and retired get to coast through with full benefits?

robc

Nov 8 2023 at 11:00pm

Thats pretty much how ponzi schemes work.

steve

Nov 8 2023 at 11:05am

When they set the cap in the 80s 90% of income was taxed for SS. Since then that has dropped to about 80%. I dont think they foresaw that income growth would be so disparate. I think what will happen is that the game of chicken will continue until benefits start getting cut. Then the party holding the bag will have to come up with a solution and the other party will demagogue whatever solution they come up with.

Steve

Luke J

Nov 9 2023 at 12:04am

Unfortunately, I think this is most likely.

MarkW

Nov 8 2023 at 12:05pm

I wonder if there’ll be any benefit to wealthier retirees taking SS at 62 to avoid having SS checks that are ‘too high’ and more tempting to slash? Asking for a friend.

Scott Sumner

Nov 8 2023 at 1:11pm

In addition, you get more benefits before any future cuts. See David Henderson’s recent post:

https://www.econlib.org/when-to-collect-social-security-is-a-tough-problem/

Rajat

Nov 9 2023 at 6:12am

“Restricting benefit cuts only to wealthy people is equivalent to a tax on wealth creation. It would represent a rise in the implicit marginal tax rate on income and saving”

The responses I often see to this sort of claim is that high income-earners will save enough anyway and that high earners’ elasticity of labour supply is very low, so it makes sense to stick it to them. You have made the point in the past that short run elasticities tend to be lower than long run elasticities, but unfortunately, the long run elasticities seem to seldom be estimated. How would you respond?

Scott Sumner

Nov 9 2023 at 2:01pm

Almost everyone underestimates the responsiveness of people to incentives. It’s a long uphill battle to convince them otherwise.

You can also point to the fairness issue. Two people with the same lifetime labor income should not face different tax rates merely because one decides to consume relatively more when young.

johnson85

Nov 9 2023 at 10:09am

I know it will never happen, but it seems like the obviously right move to just let benefits be reduced to match SS tax revenue. Boomers basically promised themselves that younger taxpayers would pay them a bunch of money in retirement, and then they didn’t go and make the taxpayers. Getting 12.4% of the wages of younger workers seems like a reasonably enough compromise, since they paid roughly 12.4% of their wages to older generations. To the extent it’s less than they promised themselves, they also as a whole avoided the cost and effort of raising those extra taxpayers.

Still pretty unfair between the boomers that did the work of raising children and those that did not, but hopefully they ones that raised children will have some of those children help them if needed.

And if this resulted in some of the lowest ss recipients not being able to survive, you could combine it with some minimum benefit below which they aren’t subject to the cap, or probably better, make sure they are eligible for SNAP.

Jim Glass

Nov 9 2023 at 5:59pm

Boomers basically promised themselves that younger taxpayers would pay them a bunch of money in retirement, and then they didn’t go and make the taxpayers.

Not true, not at all. The boomers are scheduled to receive in benefits only about the exact amount they paid in through taxes. The last time I looked at the SSA actuarial data the “break even” cohort was birth year 1953 (hey, that’s me!) right in the middle of the boomer birth years.

The problem is the pre-boomer generation received hugely more in benefits than they paid in. The first SS beneficiary to receive a check, Ida May Fuller, paid total taxes of $24.75 and received $22,888.92 in benefits.

The boomers’ taxes were used to pay the benefits of Ida and her pre-boomer compatriots. Now, who’s going to pay for the boomers (me!!)? The Nobelist Paul Samuelson said not to worry because “Social Security is a Ponzi Scheme That Works“….

That is, social insurance being actuarially unsound was a feature, not a bug — not just for Social Security but also for then-young Medicare. If Paul was still around, he might want that one back.

Interestingly, FDR had a much better handle on this than the great economist. When his SS Act of 1935 passed he proclaimed it “actuarially sound and out of the Treasury forever”, and meant it. It wasn’t going to pay full benefits for a couple decades and then they would be based on the interest rate earned on the federal bonds that workers’ payroll taxes had bought to fund them. He was absolutely insistent that no general revenue ever be called into the system. When he discovered that 30 years later, in the 1960s (!!), his draft program called for some general revenue to top off benefits, he had a famous tantrum and ordered the bill withdrawn from Congress and re-written. Yes, FDR, the creator of the New Deal, was fiscally far more conservative than anyone in politics today. Ponder.

His program lasted all the way until the payroll taxes started coming in. Then, incentives! free cash!! political incentives!!! The Left decried all that tax revenue going into bonds and demanded that it be spent on, er, invested in, their favorite social projects instead (in the 1930s they had quite a list). The Right said, we can’t let the left squander the money like that, and the tax rate is too high, tax cuts for workers! They compromised by increasing and expanding benefits while cutting the payroll tax rate in half.

Arthur Altmeyer, FDR’s head of SS, objected to Congress that by arithmetic this would make SS insolvent in the long run (see 1983), and that giving Ida & Co benefits so much higher than the bond rate would force future benefits to be below the bond rate (see today, and getting worse) which would be unfair to future workers and cripple SS’s future credibility with them. He reported that the Congressional leaders replied, “That will be somebody else’s problem”. Ida voted then!

FDR vetoed Congress’s enactment of the changes. Congress over-rode his veto. It was his only veto ever to be over-ridden. Such is the power of political incentives over fiscal planning. That’s not going to change now.

The details of the story are really educational about politics. The SSA has an excellent history section on its web site, and my favorite book on it all is “The Real Deal” by Schieber & Shoven. It’s out of print now but Schieber was past chairman of the Social Security Advisory Board and is authoritative. It dates back to when politics was sane enough to be bitterly loopy about important issues (“SS reformers want to make grandma eat cat food”) instead of about who uses what bathroom, and covers all the bases.

Floccina

Nov 9 2023 at 7:37pm

It is welfare, which is government forced charity, so I think they should not give cost of living increases to those getting more than $260.00/week in 2023 dollars until every retiree gets the same amount, 260 2023 dollars per week.

Scott Sumner

Nov 11 2023 at 12:55pm

Well that’s also a disguised tax increase, but a far less bad option than basing benefit cuts on income, which really hurts savers.

A. Squaretail

Nov 10 2023 at 7:32am

The risk of reducing benefits to those who saved was my reason for beginning social security at 62. If you can save and reinvest it, its your best chance to get your money back. If you’re lucky you might even get enough to dent the inflationary losses incurred over the past 45 years. I still advise friends with fewer assets to delay social security as insurance against future inflation or bad luck investing.

Jose Pablo

Nov 10 2023 at 6:03pm

You would be amazed by the “contemporary” readings of the grasshopper and the ant parable.

From a passage of “Mondays in the Sun” (a Spanish movie):

Still, frustration broils just beneath the surface. When Santa (one of the movie characters) reads the child to sleep with the fable of the ant and the grasshopper, he can’t help himself; he starts railing against the ant’s capitulation to the system.

So, you get the whole thing wrong Scott, the ant, capitulating to the system, is the villain. The ants are the ones that have to learn their lesson, for instance forcing them to share.

Obviously for their own good: they will discover the happiness of sharing (after all sharing is caring, we teach this to our children, don’t we?)

Jim Glass

Nov 11 2023 at 1:02am

Also keep in mind that many benefit cuts are disguised tax increases.

Well, in the case of Social Security, the income tax increases imposed since 1983 have been an a disguised benefit cut, as the tax collected is sent back to the SSA instead of going into the Treasury’s general revenue. So … a two-fer!

Overall, reading this thread from the top, I’m impressed by all the carping and complaining combined with a total lack of anyone proposing any constructive credible solution to any problem.

It’s really simple: There’s not enough funding to pay for promised benefits. So the only possible options are taxes go up and/or benefits go down. OK, so people here don’t want to increase taxes/cut benefits for the rich, That means you do want to increase taxes/cut benefits for the poorer. QED. Is that really both “better” policy and politically credible? Explain.

The whole problem was spelled out plain 30 years ago. The 1994-1996 Social Security Advisory Council examined the issues in great detail and made several solid proposals to make SS permanently solvent, from fully “statist” to fully free market, and in between. There was a huge amount of public discussion about them in the years that followed, in the general press, on the Internet of the day (such as sci.econ), if I look back in the archives probably in the early days of this site.

Now nobody remembers any of it. Which indicates – by revealed preferences – nobody really cares. When a huge amount of readily available information and informed analysis on a problem are totally ignored by the people complaining about it, well, that shows what they do care about. Social media era “analysis”. Which, amid all the whining about Social Security, doesn’t even recognize that it is MEDICARE that’s going to crash the fisc — comparably, Social Security’s problems are small potatoes.

The late, great, Senator Daniel Patrick Moynihan said back then: ‘Fixing Social Security is easy, it’s just a little cash flow. Fixing Medicare is going to be really hard. So if we can’t fix Social Security, we’re screwed.’ Well…

Bitter old man that I am, I have no sympathy for anybody, on any side of the issue, as to it all now. The problems and solutions have been spelled out and been visible to anyone who looked for the ~25 years since he said that. Nobody has cared. Now what’s coming is coming, no way out.

I don’t blame the politicians. I blame the voters, whom the politicians have to please to survive. Including, especially, the most “educated” and “informed” voters.

“Democracy is the theory that the common people know what they want, and deserve to get it good and hard.”

— Menken

Jose Pablo

Nov 11 2023 at 12:47pm

So the only possible options are taxes go up and/or benefits go down.

Is that your definition of a “credible” solution?

None of the two is “credible”.

If we go for non-credible solutions, putting behind bars all the politicians responsible for this Ponzi scheme would be a much better one (after all, that’s what we do with the people running this kind of schemes).

Jim Glass

Nov 11 2023 at 8:59pm

Congratulations! You are exactly the voter that Congress has obeyed in creating this mess. They’ve followed you in this for 30 years. That’s what good elected representatives do, follow the will of the people.

Enjoy the result!

Scott Sumner

Nov 11 2023 at 12:53pm

“So the only possible options are taxes go up and/or benefits go down. ”

That’s mostly right, but 3 million immigrants a year would help.

Jose Pablo

Nov 11 2023 at 12:58pm

Temporarily … increasing the number of “suckers” entering the system is always a solution for any Ponzi scheme (as it is increasing the contribution of the existing ones or reducing the promised returns to the “investors” exiting the system).

And yet they are never the solutions recommended by the courts. And for very good reasons.

Jim Glass

Nov 11 2023 at 9:10pm

At the margin.

“Net immigration: If there is a larger increase in immigration levels then Social Security income relative to cost would decrease by $1.5 trillion; if there is a smaller increase in immigration levels the shortfall would increase by $1.5 trillion.”

— https://www.fiscal.treasury.gov/files/reports-statements/financial-report/2022/social-insurance.pdf

$1.5t is 6.5% of the base excess cost of $23.3t.

Comments are closed.