As I get older, I become increasingly frustrated with having to repeatedly push back against widely held myths. One of those myths is that a recession occurs when there are two consecutive negative quarters for real GDP growth. That’s not how the NBER determines recessions. (One obvious example is 2001, which saw a recession but did not see two consecutive negative quarters.)

Some people are now making a big deal of the fact that the Atlanta Fed’s GDP tracker is currently predicting a negative 2.1% real GDP growth rate in the second quarter. (Following a negative 1.6% growth rate in Q1.) Even if that forecast pans out, it doesn’t mean the US economy was in recession throughout the first half of 2022—an absurd claim—rather it suggests that six-month changes in RGDP are not a reliable indicator of business cycles.

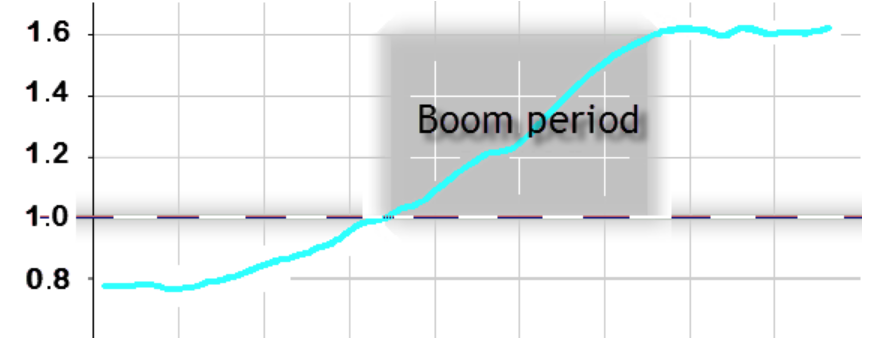

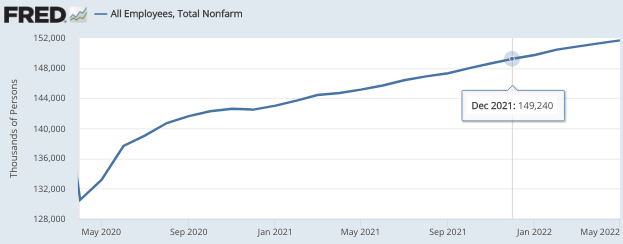

Not only was the economy not in recession in early 2022, it was experiencing the most overheated boom in many decades. Consider that payroll employment soared by roughly 2.5 million during the first 5 months of 2022, roughly three times the normal rate of growth. That’s some of the fastest job growth we’ve ever seen. And companies were still desperately short of workers.

That’s not to say the US economy might not currently be entering a recession. Perhaps the payroll employment data will soon turn down. It’s even possible that a recession began a month ago. But the US economy certainly wasn’t in recession this past winter.

READER COMMENTS

Chris Loukas

Jul 3 2022 at 4:35pm

Very interesting article professor Sumner. Could you do another one to explain what is right definition of inflation. It would be a very interesting follow up.

vince

Jul 3 2022 at 4:46pm

NBERs traditional definition of recession: significant decline in economic activity that is spread across the economy and lasts more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.

Real GDP decline by itself isn’t enough.

artifex

Jul 3 2022 at 6:22pm

The myth is sufficiently widespread to influence the NBER’s committee. I estimate 70% that they’ll determine a recession occurred in 2022 and 60% that, if they do, the determined peak won’t be after April. They say they put more weight on real personal income less transfers and nonfarm payrolls, but I think they actually put more weight on real GDP because they’re not oblivious to what everyone expects them to say.

Scott Sumner

Jul 3 2022 at 6:52pm

Sure, it’s possible that a recession began in May. But I suspect the recession will occur somewhat later (if at all.)

Mark Brady

Jul 3 2022 at 6:40pm

“As I get older, I become increasingly frustrated with having to repeatedly push back against widely held myths. One of those myths is that a recession occurs when there are two consecutive negative quarters for real GDP growth. That’s not how the NBER determines recessions. (One obvious example is 2001, which saw a recession but did not see two consecutive negative quarters.)”

It’s not a myth. The concept of a recession is an economists’ construct, and as such, opinions may differ as to the definition. E.g., the UK Treasury states that “The commonly accepted definition of a recession in the UK is two or more consecutive quarters (a period of three months) of contraction in national GDP.” (Please excuse my poor taste in quoting the UK Treasury on the eve of Independence Day.) I’m happy to go with a different definition, but just because the NBER determines what constitutes a recession doesn’t make their definition definitive (pun intended).

Scott Sumner

Jul 3 2022 at 6:53pm

Did the NBER miss any US recessions? No. Did they call a recession that wasn’t a recession? No. Until either of those happen, I’ll go with the NBER.

Dylan

Jul 4 2022 at 9:21am

Absolutely. The recession from Feb 2020 – April 2020 wasn’t a recession because it didn’t have two quarters of decline in real GDP.

In case it wasn’t obvious, what I’m getting at is you can’t defend a definition on something by relying on that same definition.

Scott Sumner

Jul 4 2022 at 12:39pm

We didn’t have a recession in 2020? That’s certainly a novel view. Unemployment rose to over 14% and output plunged. That’s not a recession?

Dylan

Jul 4 2022 at 2:42pm

Not according to the definition that a recession is two quarters of decline in real GDP. All I was trying to say is, if you tell me that the NBER is the definitive source of what qualifies as a recession, and then you ask me to prove you wrong by finding a time where the NBER was wrong…you’re asking me to prove there is such a thing as a married bachelor. To evaluate the truth of your statement, I need an alternative definition of what constitutes a recession in which we can measure the NBER against. “I know one when I see one” doesn’t count.

Jon Murphy

Jul 4 2022 at 2:21pm

The NBER does have a recession in 2020 (February to April).

Dylan

Jul 4 2022 at 9:31am

Also, as someone who often equates truth to what is useful. The NBER calling something a recession seems particularly not useful. Have they ever called a recession while we were still in it?

https://www.isabelnet.com/nber-recession-dating-vs-market-realization/

Jon Murphy

Jul 4 2022 at 2:22pm

According to your link, all the time.

Dylan

Jul 4 2022 at 2:55pm

You’re right. I was looking at the table and not the chart and misread things. That’s what I get for not being a visual person.

Still, it looks like there is only once they called it in the middle of the recession, and twice when we were basically at the bottom. I agree that NBER isn’t about helping investors, that’s not the mandate. But, in that absence, investors and the rest of us are going to look for shortcuts to being able to call a recession before NBER gets around to it. In that context, I think the rule of thumb two quarters of RGDP decline seems pretty reasonable. In short, I can’t tell what Scott is upset about or why he calls this a “myth” as opposed to a helpful approximation.

Jon Murphy

Jul 4 2022 at 2:30pm

Also, to your link: the news story complains that NBER recession dating isn;t particularly helpful for investors. That’s likely true, but also not what NBER is about. They’re a research outfit. They’re not trying to provide real-time data for investors.

In short, I think the article is holding NBER to an improper standard. They’re complaining that a duck is not useful because it cannot drive a car.

Jon Murphy

Jul 4 2022 at 11:56am

Thanks for this post. I have been teaching this myth for years! I have to correct myself.

vince

Jul 5 2022 at 10:33pm

Maybe you picked up the myth from A Guide to Everyday Economic Statistics by Clayton. He acknowledges both definitions, claiming the two-quarter version “is popular because GDP is reported on a regular basis and it is fairly easy to keep track of.”

MIchael Sandifer

Jul 4 2022 at 6:39pm

I agree completely. If you want to add a requirement that unemployment increase to a period of negative real GDP growth, that makes sense.

robc

Jul 4 2022 at 9:29pm

This may seem off-topic, but the comments made me think of this quote.

“Tragedy is when I stub my toe. Comedy is when you fall into an open manhole and die.” — Mel Brooks

Phil

Jul 7 2022 at 10:55am

If NBER’s definition of recession is not two consecutive quarters of negative real GDP growth, does that make it a myth? Perhaps different definitions may exist without one being a myth.

The “two consecutive quarters” definition has problems, but it has the advantages of being simple and objective. NBER’s definition is subjective. How much is “a significant decline”? What is “normally visible”?

Todd Kreider

Jul 8 2022 at 11:59am

From NBER’s site:

Q: What is a recession? What is an expansion?

A. The NBER’s traditional definition of a recession is that it is a significant decline in economic activity that is spread across the economy and that lasts more than a few months. The committee’s view is that while each of the three criteria—depth, diffusion, and duration—needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another. For example, in the case of the February 2020 peak in economic activity, we concluded that the drop in activity had been so great and so widely diffused throughout the economy that the downturn should be classified as a recession even if it proved to be quite brief. The committee subsequently determined that the trough occurred two months after the peak, in April 2020. …

Peter Gerdes

Jul 17 2022 at 7:13pm

How does it matter? It’s just a definition. I could use the word recession to mean two quarters in which I didn’t splurge on ice cream and, as long as everyone understood that’s what I meant, it wouldn’t be misleading in any way.

In other words as long as enough ppl think that’s what recession means it is (most ppl aren’t making a claim about NBER official designations…hell they don’t even know what NBER is).

Now, I’ll grant there is a better criticism here in that people assume that the 2 quarter statistic coincides with a certain kind of experiences by the public. However, the problem there is that pretty much any definition you choose will only very very loosely relate to those experiences.

Rob

Jul 29 2022 at 3:27pm

I think the more pertinent question is this: How many times in the existence of the NBER have there been two consecutive quarters of negative GDP growth in which the NBER did not ultimately declare that a recession occurred? For this discussion it really doesn’t matter whether the NBER also has declared a recession even though two consecutive quarters of negative GDP growth did not occur. What we really want to know is if there are two consecutive quarters of GDP growth, how likely is it that we are in a recession. I have read that since 1948 the correlation is 100% (I don’t actually know if that is accurate).

Comments are closed.