Matt Yglesias had a post discussing the fact that people are reluctant to admit when they’ve been wrong:

My two least-favorite moments in the 2022 discourse were 1) left-wing people confidently asserting that Joe Manchin’s objections to Build Back Better were offered in bad faith due to his fealty to the coal industry and 2) right-wing people confidently asserting that Sam Bankman-Fried would be immune from legal consequences due to his campaign contributions to Democratic Party elected officials.

Those assertions rankled in my view not because being wrong is such a terrible sin, but because when those assertions were proven wrong, I saw almost no effort by the people who’d made them to grapple with their own wrongness.

Back in the 2010s, monetary hawks were reluctant to admit that they were wrong about monetary policy. They argued that Bernanke’s policies were too inflationary. In fact, the Fed mostly undershot its target for inflation and even more so for the dual mandate. Have the hawks admitted their error?

A year ago, it had become obvious that the Fed had erred in implementing an excessively expansionary monetary policy. Policy doves warned against tightening too much and thus pushing the economy into recession. With the 4th quarter NGDP figures released today, it’s 100% clear that the doves were wrong. NGDP growth came it at 6.5% and 7.3% over the past four quarters. I estimate that NGDP growth needs to average about 3.5% if the Fed is serious about its inflation target, but even if you use the figure of 4%, growth has been way too strong in 2022.

We also know that the people arguing that inflation was a supply side problem were completely wrong. While a few of the monthly figures were affected by supply shocks, over the past three years all of the inflation has been demand side. Here are the relevant figures:

Total NGDP growth from 2019:Q4 to 2022:Q4: 20.4%

Total trend NGDP growth assuming 1.5% trend RGDP and 2% inflation = 10.9%

Total trend NGDP growth assuming 2.0% trend RGDP and 2% inflation = 12.4%

Thus excess NGDP growth equals 9.5% assuming trend NGDP is 3.5%/year, and excess NGDP growth equals 8% assuming trend NGDP is 4%/year.

This means that if there had been no supply shocks at all, then we should have expected somewhere between 8% and 9.5% excess inflation over three years. That is the price level over the past three years should have risen by between 8% and 9.5% more than it would have under 2% inflation targeting.

The actual rise in the price level (PCE) over the past three years has been 12.9%. That’s an excess of 6.8% inflation over the 6.1% you would have gotten with prices rising at 2%/year for three years (with compounding.) This suggests that more than 100% of the inflation has been demand side; the effect of the supply side has been to reduce the price level. (If you use the implicit price deflator, total inflation has been 14.5%, and roughly 100% of the excess inflation is due to demand increases. RGDP has risen at trend.)

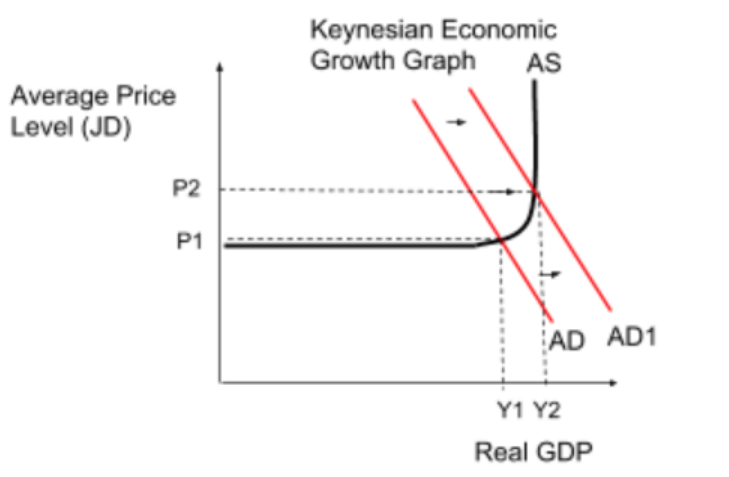

This outcome is perfectly in accord with standard AS/AD models. In those models, the SRAS curve slopes upward. Thus if aggregate demand (NGDP) rises by an extra 8% or 9% over three years, much of that will show up in excess inflation, but a portion will show up in rising RGDP. Output will rise to above the “natural rate.” In my entire life, I’ve never seen output so far above the natural rate as it is today. When I travel, I find service to be almost laughably bad, due to severe labor shortages. In my view, trend RGDP actually fell during COVID, and RGDP is a couple points above the new and lower natural rate.

Unfortunately, it’s hard to find decent graphs for demand shocks on the Internet. (And what does that tell us?) For the graph below, assume Y1 is the natural rate of output and Y2 is our current level of output. Also assume that AD (i.e., NGDP) shifted to the right by 9% (relative to trend), the price level rose by 7% more than target, and real GDP rose to 2% above the natural rate. That’s a graphical presentation of where we are today:

At the beginning of 2022, the Fed should have adopted a much tighter monetary policy. The doves were wrong. How much tighter is debatable. Would 6.0% NGDP growth have been optimal? How about 5.0% growth? How about 4.0%? I don’t know, but 7.3% was clearly way too high. Not only did we not get a soft landing, we didn’t even come close to getting any kind of landing at all. It’s like a skittish rookie fighter pilot who’s so timid he remains 100 yards above the flight deck when trying to land on an aircraft carrier. Yes, you don’t want to crash land, but if you don’t try harder to land the plane then you’ll run out of fuel and the consequences will be far worse.

The Fed didn’t want to suddenly bring NGDP growth down to 2.0% in 2022. But 7.3% was wildly excessive. Not only did we not impose too much pain on the labor market, we didn’t impose any pain at all. Indeed we imposed negative pain, akin to the euphoria induced by heroin addiction. Nominal wages are still rising way too fast. The 3.5% unemployment rate today represents an even more overheated labor market than the 3.5% unemployment of late 2019. There’s a severe shortage of workers.

The Fed is missing both sides of its dual mandate in the same direction—too much inflation and an extreme labor shortage.

For America’s doves, it’s a time for some soul searching. (Larry Summers was right.)

PS. This post is about the mistakes of 2022. It’s entirely possible that the Fed will make the opposite mistake in 2023. It’s too soon to say. But the mistakes of 2022 will make their job this year that much harder. If they had not overheated the economy to such a large extent in 2022, a soft landing would have been easier to achieve in 2023.

PPS. The media keeps referring to growth in real consumption as “demand.” Sigh . . .

If aggregate demand is to mean anything, it must be a nominal variable.

PPPS. And no, monetary policy does not affect the economy with long and variable lags. Interest rates affect monetary policy with long and unpredictable leads and lags. But interest rates are not monetary policy.

READER COMMENTS

Art G

Jan 26 2023 at 8:12pm

There are arguments on both sides. The below articles state things are under control now and have been for a few months. People see the same information and have different takes.

https://ritholtz.com/2023/01/for-lower-inflation-stop-raising-rates/

https://econbrowser.com/archives/2023/01/instantaneous-inflation

Scott Sumner

Jan 26 2023 at 8:39pm

Those links don’t have any bearing on the question of whether policy was too expansionary in 2022.

Art G

Jan 27 2023 at 10:39am

“We also know that the people arguing that inflation was a supply side problem were completely wrong. While a few of the monthly figures were affected by supply shocks, over the past three years all of the inflation has been demand side.”

“The Fed is missing both sides of its dual mandate in the same direction—too much inflation and an extreme labor shortage.”

The articles argue that inflation is a supply side problem and inflation has been under control for a little while now. The opposite position of this post.

Scott Sumner

Jan 27 2023 at 12:43pm

You mean this:

“The narrative I have been spinning is that the pandemic-related surge in demand overwhelmed supply constraints and that lead to price spikes.”

Thomas Lee Hutcheson

Jan 28 2023 at 5:21pm

It s impossible to over do “maximum employment.”

Scott Sumner

Jan 29 2023 at 7:54pm

Worker shortages are bad. People suffer from bad service. My 96-year old mom is suffering.

Todd Ramsey

Jan 27 2023 at 10:49am

If you are soul-searching…

“That’s not to say that monetary policy is perfect; the distortions caused by Covid make it much harder than usual to “read the tea leaves”. But we are not far off course.” 10/8/21

I think you would explain this by a misunderstanding of FAIT as viewed by the Fed, and true symmetrical FAIT?

A clear explanation of your 10/8/21 views would enhance your high credibility (honest comment, not sarcastic).

Scott Sumner

Jan 27 2023 at 12:47pm

Yes, that was assuming the Fed had a symmetrical FAIT. I have stated many times that I was naive in assuming the Fed was serious about average inflation targeting. If they had been serious, we would not have had the huge demand overshoot in late 2021 and 2022. I still believe FAIT would have been a good policy—pity the Fed never tried it.

Even today, I don’t believe policy was far off course on 10/8/21, if the Fed had applied FAIT in a symmetrical fashion. NGDP was roughly on trend at that time.

Spencer

Jan 27 2023 at 11:11am

“At the Dec. 27–29, 1971, American Economic Association meetings, Milton Friedman (1972) presented a revision of his prior work on the lag in effect of monetary policy (e.g. Friedman 1961). His new conclusion was that ‘monetary changes take much longer to affect prices than to affect output’; estimates of the money growth/CPI inflation relationship gave ‘the highest correlation… [with] money leading twenty months for M1, and twenty-three months for M2’ (p. 15)”

Mark Brophy

Jan 27 2023 at 1:58pm

Bernanke’s policies were too inflationary in the 2010’s. They caused stock prices to inflate, transferring wealth to the rich from people with low and middle incomes. Inflation comes in two forms, consumer and asset inflation.

Scott Sumner

Jan 27 2023 at 2:46pm

The term “inflation” refers to a rise in the price of goods and services. Asset inflation is a made up concept that is not part of the Fed’s mandate (fortunately), and doesn’t have the impact that its proponents think it has. It’s a silly idea that is best discarded. It’s not important — at all.

In addition, the Fed did not cause asset inflation in the 2010s, because its policies were not at all inflationary.

You might just as well blame the Fed for “grade inflation”.

Spencer

Jan 28 2023 at 12:54pm

re: “Asset inflation … doesn’t have the impact that its proponents think it has.

…

Asset valuation prices are driven from the appraisal of loan collateral, and loanable funds, which depends upon Gresham’s law: “a statement of the least cost “principle of substitution” as applied to money: that a commodity (or service) will be devoted to those uses which are the most profitable (most widely viewed as promising), that a statement of the principle of substitution: “the bad money drives out good”.

…

Link: “HOUSING IS THE BUSINESS CYCLE” Edward E. Leamer

https://www.nber.org/system/files/working_papers/w13428/w13428.pdf

Thomas Lee Hutcheson

Jan 28 2023 at 5:25pm

Summers in 2021 was warning that budget deficits could cause inflation. That is not right without an additional assumption that the fed will change its inflation target to accommodate the deficit

Scott Sumner

Jan 29 2023 at 7:55pm

That’s right.

Peter Gerdes

Jan 29 2023 at 3:04pm

Could you explain that bit at the end about how demand has to be a nominal variable?

Why? And what kind of error does conflating real consumption with demand cause? Like I’m trying to understand how you see the media as leading ppl astray here.

Scott Sumner

Jan 29 2023 at 7:53pm

EC101 says that a change in quantity tells us absolutely nothing about whether the change was caused by the supply side or the demand side. Take an AS/AD diagram and shift the AS curve to the right. Hold AD constant. Real consumption will rise even though demand hasn’t increased at all (by assumption.)

Comments are closed.