Why are people choosing Medicare Advantage plans? The main reasons are that the insurance plan is required to cover everything in Medicare Part A and B, but it is also allowed to provide additional services–at no additional cost to the patient. Some common add-ons include certain vision, hearing, and dental services, and sometimes services like transportation to the doctor and subsidies for joining a health club. In addition, Medicare Advantage plans can be customized, so that they provide more coverage (say, lower co-pays) for the services you know you are more likely to use. In some areas, you can even make a fairly seamless transition from health insurance provided through your employer, by a certain company, to health insurance provided by Medicare, through the same insurance company.

This is from “Medicare: Becoming a Channel for Private-Sector Insurance,” Conversable Economist, August 30, 2022. The whole thing is well worth reading. It makes me wonder whether, when I retired at age 66, I should have taken Medicare Advantage. I didn’t. I had great insurance as a federal employee and the feds pay the same towards my and my wife’s insurance that they would have paid if I had remained employed. Still, I’m paying $7,000 a year for my health insurance. And of course that doesn’t include co-pays and deductibles.

I also found this part particularly interesting:

For example, various versions of “Medicare for All” legislation have been proposed. In some versions, this would be a universal national health insurance plan run by the government. Whatever the merits or demerits of such a proposal, actual real-world Medicare is shifting to a choice of plans run by insurance companies, and only funded by the government. The elderly have a choice between having their health insurance administered by the US government or by a private insurance firm–and they are choosing the private firm.

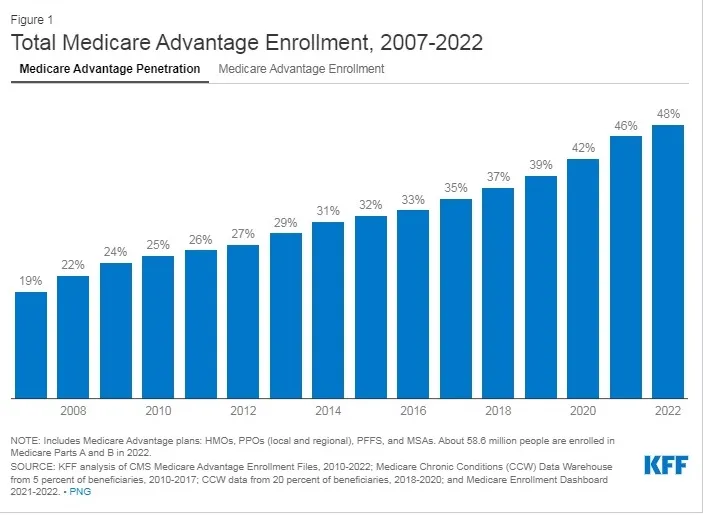

Since 48% of Medicare beneficiaries are in Medicare Advantage, up from just 19% in 2007, that means that one of the biggest lobbies against Medicare for All, if run by government, will be participants in Medicare Advantage.

I had heard that Medicare Advantage costs the government more than it pays for people in Medicare Parts A (hospital) and B (doctors.) That’s true. But here’s what Tim Taylor writes about that:

I do not have a fully convincing answer here. It’s true that the government pays a little more for Medicare Part C [that’s the name for Medicare Advantage], on average, than for Parts A and B, but it’s only about $300 per person per year, so that’s unlikely to be the main driver. My guess is that big insurance companies are better at managing health care costs, and perhaps no worse at managing paperwork and administrative costs. After all, the insurance companies are paid a flat amount per patient, rather than being reimbursed on a fee-for-service basis like traditional Medicare A and B. One can, of course, raise concerns about just how private insurance might seek to control health care costs. But again, the key point is that the elderly are increasingly showing by their actions that they prefer the Medicare Advantage plans, funded by the federal government, but run by private insurance companies.

$300 per person is way less than I had thought. It’s close to rounding error.

READER COMMENTS

Jim Glass

Aug 30 2022 at 7:13pm

I have Medicare Advantage, am very pleased with it, the dental benefits alone have made it a deal for me. (Happily I’ve been quite healthy so far, so no stress tests yet.)

As a NYC kid way back we when I was a big Joe Namath fan. He talked me into it!

Various

Aug 31 2022 at 11:32am

John C Goodman

Aug 31 2022 at 5:42pm

Medicare Advantage plans have been under attack recently by the DC health bureaucracy.

Here is my answer to them: https://www.goodmaninstitute.org/2022/07/17/the-attack-on-americas-best-health-plans/

David Henderson

Aug 31 2022 at 6:53pm

Just read your response. Excellent. Thanks, John.

I think if my wife and I switched now, we would pay a huge penalty because we wouldn’t be switching from Medicare but to Medicare.

Matthew

Aug 31 2022 at 8:46pm

Obviously you missed the two Inspector General reports over the past four years discussing the rampant denial of service along with delayed service from pre-authorizations. Or the letters complaining of the same from major hospital associations.

Coupled with the headlines showing growth in Medicare Advantage plans are the headlines about the abusive misleading sales practices from third party lead generators. Kinda funny, huh?

Why are more people enrolling in Medicare Advantage? Two reasons. 1. Group Advantage Plans. More large employers are moving their retiree health plans to customized Advantage plans because they get a bonus from the insurance company to do so. 2.Money. The US Government pays so much money to these insurance companies that they can pay commissions to agents that are two to five times that of a supplement. They pay bonuses to doctors to be the PCP on HMOs. They pay a lot and money talks.

It has nothing to do with quality of care.

David Henderson

Sep 1 2022 at 6:39pm

Interesting thoughts. Thank you, Matthew.

I wonder how you would respond to the points John C. Goodman made in his piece that he linked to in his comment above.

Comments are closed.