Josh Hendrickson has a new Substack post that discusses the implications of the US dollar’s role as an international reserve currency. This caught my eye:

When you are taught a typical model of international trade with flexible exchange rates, discussion of the balance of trade goes something like this. If a country runs persistent trade deficits, its currency will begin to depreciate. The depreciation of the currency makes foreign goods more expensive. This tends to reduce imports and push the country toward balanced trade. The basic point here is that a typical textbook argument is that flexible exchange rates adjust to the balance of trade and these adjustments tend to reduce the trade deficit and push the country towards balanced trade.

By contrast, the U.S. runs persistent trade deficits that do not self-correct. In fact, many times, the dollar appreciates while the U.S. is running trade deficits. How can we explain this phenomenon?

The reason that the U.S. is different is that the dollar is the primary currency used in global trade.

Two comments:

- The US isn’t different.

- Josh Hendrickson should get a new textbook.

Here’s the US current account as a share of GDP:

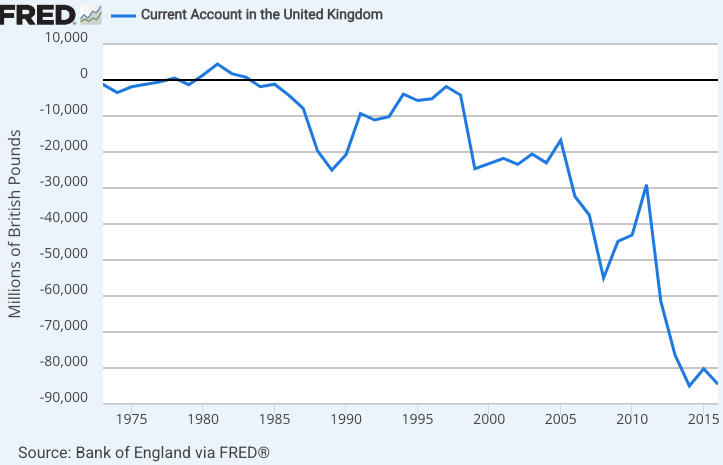

Now let’s look at Great Britain:

Unfortunately, the British FRED series ends in 2016 and is in money terms, not share of GDP. However, another source confirms the UK current account deficits have continued at roughly 3% of GDP.

And here’s New Zealand:

And here’s Australia:

In fairness, a more recent Fred series shows a brief period of surplus, before returning to deficit in 2024:

In fact, the US is fairly typical of English-speaking countries that draw a lot of immigration—it runs fairly persistent deficits. The outlier is Canada, which ran current account surpluses from 1999-2008, but even they have seen current account deficits for the past 16 years, and 52 of the past 65 years.

A current account balance merely reflects the difference between saving and investment; there’s no reason why it cannot continue indefinitely. It may be associated with excessive borrowing, especially excessive government borrowing, but that is not always the case. (Australia tends to have small budget deficits.)

The US current account deficits are probably caused by the same sort of factors that explain current account deficits in other English-speaking countries: low saving rates, highly productive capital investments and high rates of immigration. I see no evidence that the dollar’s role as a reserve currency plays much of a role, unless you believe that the New Zealand dollar is also an important reserve currency.

Hendrickson continues:

The short answer is that other countries have to be net importers of dollars and therefore net exporters to the U.S.

What this implies is that the U.S. must run persistent trade deficits with the rest of the world in order to provide the world with dollars.

This is not accurate. A current account deficit is not a net flow of dollars; it is a net flow of assets. We could pay for imports by selling real estate or equities or junk bonds. A foreign country could accumulate US dollar reserves (Treasuries) by selling assets like stocks or real estate or foreign government bonds.

The US current account deficit reflects the discrepancy between domestic saving and domestic investment. The US is not “forced” to run a deficit, even with the dollar serving as an international reserve currency.

I don’t worry about current account deficits, but if the Trump administration wishes to address the issue then they should consider reducing the government budget deficit (which is negative saving.) Instead, they are planning to enact a giant tax cut. A recession might also reduce the current account deficit, by reducing domestic investment.

PS. I’m not certain why Australia’s current account has recently become more positive; perhaps it reflects a cultural change associated with extensive immigration from (high saving) Asian nations. But that doesn’t explain Canada.

READER COMMENTS

Jon Murphy

Apr 17 2025 at 3:17pm

I, too, was surprised when he wrote that. The textbooks I use for both my Principles courses and my upper-level international trade course explicitly warn against making the argument Hendrickson makes.

steve

Apr 17 2025 at 4:03pm

Thanks Scott. I have found it fairly easy to explain to people why a trade deficit between 2 countries doesnt mean what many people, especially those supporting tariffs think it means. But, I think I have not put into words as well as I wanted why persistent total trade deficits were not a concern to approach with tariffs. Will be stealing your explanation.

Steve

Andrew_FL

Apr 17 2025 at 5:05pm

You can get the series you want for the UK by taking FRED series: GBREXPORTQDSMEI And subtracting GBRIMPORTQDSMEI Then dividing by GBRGDPNQDSMEI.

Scott Sumner

Apr 18 2025 at 12:42pm

Thanks for that info.

Warren Platts

Apr 17 2025 at 8:09pm

I want to push back, respectfully, on this. I agree that the US is not forced to run a trade deficit because of some sort of Triffin dilemma in order to supply the world with USD. For years, the US ran a trade surplus, yet the USD was still the main reserve currency. However, the US and most other English speaking nations are indeed forced to run a trade deficit because S = I in a closed economy and Planet Earth is a closed economy. Therefore, if certain mercantilist countries insist on running trade surpluses by forcing up their own savings (usually by suppressing wages of their own workers), then other countries MUST run trade deficits to balance the equation. Since most English-speaking countries are fanatical believers in free trade including free capital flows, then they are the ones that wind up running the trade deficits simply because they allow the free capital inflows. Whether this is something to worry about is debatable. But if the government were to somehow magically able to reduce the government budget deficit tomorrow, that in itself would not reduce the current account deficit. The capital inflows would simply shift to the private sector. Why? Because S = I in a closed economy and Planet Earth is a closed economy. Therefore, if mercantilist countries insist on running trade surpluses by forcing up their own savings, other countries MUST run trade deficits to balance the equation. And if USA balances the government budget, unless the capital flows are managed, then they will keep flowing in. Yes, I am channeling Michael Pettis.

Jon Murphy

Apr 17 2025 at 8:48pm

Odd. You said just yesterday it would.

Warren Platts

Apr 17 2025 at 11:44pm

No I did not. Read more carefully please!

Jon Murphy

Apr 18 2025 at 9:14am

You did. The implication of your comments are that reducing government debt would reduce the trade deficit. I doubt you meant it, but that was the implication on your comments.

Warren Platts

Apr 19 2025 at 3:42am

Jon, I just explicitly said, “if the government were to somehow magically able to reduce the government budget deficit tomorrow, that in itself would not reduce the current account deficit.” If I said something different, please provide that quotation because otherwise I have no idea what you are talking about.

Scott Sumner

Apr 17 2025 at 10:54pm

I disagree with the claim that foreign CA surpluses are due to mercantilist policies. For instance, northern European countries tend to run large surpluses, and they don’t have mercantilist policies. Those countries also have strong labor unions and high social benefits, and relatively high wages.

Warren Platts

Apr 17 2025 at 11:43pm

Places like Norway or Qatar or Saudi Arabia that are major oil & gas exporters run surpluses because, well, what else can they do? Lots of countries need energy that they geologically just do not have. That sort of trade, I agree, should not be considered mercantilist.

But there are other countries that are straight up, self-avowed mercantilists, of the kind that Adam Smith railed against. China is the worst offender in absolute terms, but Germany is even worse in terms of its surplus to GDP ratio. Their CA surpluses are most certainly due to their mercantilist, industrial policies.

Scott Sumner

Apr 18 2025 at 12:47pm

That’s just flat out false. Norway is just one of many northern European countries. None of them are particularly mercantilist, and certainly not Germany, Denmark, the Netherlands, Sweden, Finland, Belgium, Switzerland or Austria.

Having a trade surplus is not a definition of mercantilist, rather it is generally defined as high trade barriers and export subsidies. The northern European countries are relatively free trade oriented.

Your comments about China are also false. Many countries have much higher trade barriers than China, which is about average in global terms.

Warren Platts

Apr 19 2025 at 4:39am

No no no no! Respectfully, if you want to be a mercantilist, you don’t need trade barriers and export subsidies. All you have to do is force up savings. The way you do that is by ensuring that most of the national income flows to the owners of capital and the businesses they control. After all, it is wealthy people that do most of the savings: poor people cannot save much just because they’re poor. In Germany, the average German is twice as wealthy as the average Spaniard, but the median German is much less wealthy than the median Spaniard and about as wealthy as the median Greek household. The reason Germans save so much is not because they are in general super-thrifty; it’s because of the extreme wealth and income inequality. (cf. Klein & Pettis, Trade Wars are Class Wars, 2020)

As for China, they have the lowest consumption share of GDP on the Planet. Of course the CCP runs that place. But it’s basically the same story: it is not a billion super-thrifty peasants living in the countryside that account for China’s high savings rate: it is the CCP and their minions that ensure that most of the national income flows into their coffers.

As for Norway, it really is in a class by itself because it is the 4th largest exporter of natural gas on the planet. Their natural gas exports dwarf anything else they export. None of the other European countries you listed come close. In this case, I’m guessing the government is doing most of the savings as they have a huge sovereign wealth fund.

The real question is what the Americans should do about it. We could force up savings by forcing down wages. But I don’t think that’s a good idea. We want to preserve high wages because workers with money in their pockets is what drives the consumption that is 70% of the GDP here. So we are ones who should probably be implementing trade barriers and capital controls. Not in order to run a trade surplus, but just to stop being the world’s chump. What we want is protectionism, not mercantilism.

Thomas L Hutcheson

Apr 18 2025 at 12:04am

“insist on running trade surpluses”

But a country cannot do this unilaterally. Policies interact.

Warren Platts

Apr 19 2025 at 4:45am

You are correct in the sense that we run a trade deficit because we passively accept running trade deficits. Because of that, the mercantilist countries can indeed insist on running trade surpluses unilaterally just because we let them.

Luis

Apr 17 2025 at 11:31pm

What textbook do you recommend?

Scott Sumner

Apr 18 2025 at 12:49pm

https://www.amazon.com/Economic-Principles-Perspective-Stephen-Rubb/dp/1464182493

Thomas L Hutcheson

Apr 17 2025 at 11:55pm

“country runs persistent trade deficits”

That is not am exogenous variable that can be analyzed.

Arqiduka

Apr 18 2025 at 6:38am

Re Australia, I suppose at some point remittances to abroad really do overtake foreign investment.

bill

Apr 18 2025 at 1:38pm

To some extent, our focus on the surpluses and deficits of countries is a distraction. Individuals make purchase and sale decisions. Investment and savings decisions. The freedom of Individuals to buy, sell, invest, save, etc should take priority over the cumulative amounts of such decisions within various boundaries. I wonder what percentage of the US trade deficit is accounted for by NYC? Yet in the end that should have no bearing on these national discussions.

Justin Pyvis

Apr 18 2025 at 9:21pm

Scott,

Australia’s recent trade surplus is the culmination of the mining investment boom of the 2000s. High prices for commodities like iron ore, LNG, and coal combined with large volumes (enabled by prior capital inflows i.e. CA deficits) to swing the balance into surplus.

Portfolio outflows from Australia’s large superannuation (retirement) funds have also contributed in recent years.

Rajat

Apr 20 2025 at 12:45am

Great post, Scott, and it’s disappointing that someone as clever as Josh made a silly claim like that. Australians had our epiphany about the meaning of the current account deficit back in the early 1990s, when an elite preoccupation with the CAD pushed us into a much more severe recession than other countries. Since then, our macroeconomic elite has largely – rightly – ignored the CAD as a factor relevant to monetary policy. As for the recent switch in Australia’s trade position, Stephen Kirchner had an excellent Substack post on this in September 2022. (BTW, anyone interested in Australian or global macro should sign up for it!) Stephen said:

Travis Allison

Apr 21 2025 at 2:30pm

Does immigration cause a current account deficit because immigrants purchase assets in the US?

Larry Stevens

Apr 23 2025 at 12:44am

We do well with a current account deficit. China does well with a current account surplus. It would be great to leave the Anglosphere out of the discussion.

Comments are closed.