Academics like me are often accused of being out of touch with the real world, relying on unrealistic theories of an idealized world of free trade. So let’s imagine a discussion between me and a “trade realist” (TR).

TR: Let’s face it; a high wage country like the US can’t possible compete with low wage countries in Latin America and Asia. We need trade barriers.

Me: What exactly do you mean by “can’t compete”?

TR: I mean we’ll end up with big trade deficits, and a loss of jobs.

Me: OK, so does this inability to compete apply to other high wage economies?

TR: I assume so.

Me: But the Eurozone is currently running a $465 billion current account (CA) surplus, seven times larger than China’s surplus, and they have high wages. Indeed the really big surpluses occur throughout northern Europe, where the wages are highest.

TR: Well the Europeans use clever tricks to favor their industries; the US tries to play fair. The bottom line is that the US has a $443 billion CA deficit, and it’s costing jobs.

Me: Yes, I forgot about those devious Nordics. But the unemployment rate in the Eurozone is currently 8.2%, while the US has a 3.7% unemployment rate, despite huge CA deficits.

TR: Europe has lots of socialist policies; you can’t compare their unemployment rate to ours. In any case, you can’t deny that persistent CA deficits are a drain on our economy, a ticking debt bomb.

Me: Can you be more specific?

TR: These current account deficits mean that we are borrowing money from the rest of the world to pay for imported goods. This can’t go on forever.

Me: Why not?

TR: Because eventually the interest burden on that debt would become too large to handle.

Me: So you are saying that huge current account surpluses result in a net indebtedness position, which leads to a net outflow of interest income?

TR: That’s right.

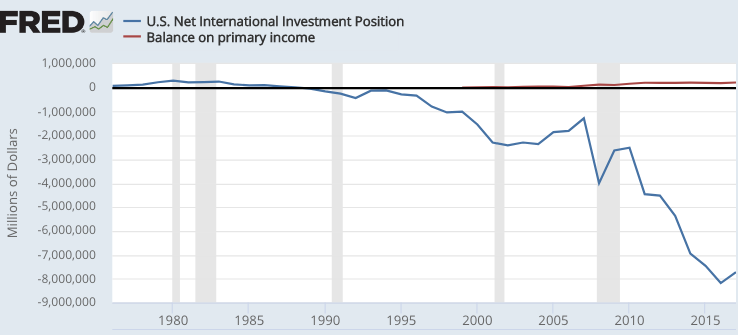

Me: But when I check the international accounts, I see our net international investment position has plunged to a balance of negative $7.7 trillion (as you say), but the net flow of investment income is a positive $221 billion/year (red line), and rising.

TR: How is that possible?

Me: Imagine you borrowed $15 trillion from your neighbor, at 2% interest, and simultaneously loaned him $7.5 trillion at 7% interest. Then you’d receive $225 billion more in interest each year than you had to pay him for your much bigger loan.

TR: But why would he do this?

Me: Search me. The point is that the US basically took $15 trillion in Treasury and corporate debt, and used it to buy roughly $7.7 trillion in goods and services from the rest of the world, and also $7.3 trillion in high earning assets. Those high earning assets spin off more than enough investment income each year to service our much larger foreign debt.

TR: This seems much too good to be true.

Me: There is a potential risk here. At some point in the future, foreigners my not be willing to lend us money at much lower rates than what we earn on our investments in their countries. At that point, the net investment imbalance could become a big problem for the US. Something very bad might happen.

TR: I though so! What is the specific bad thing that you are worried about?

Me: If that day of reckoning ever came (and I won’t live to see it, so it’s hard to know for sure), then the US would have to sharply boost its exports of goods and services to the rest of the world, to service our debts.

TR: More exports? Umm, why would that be so bad?

Me: It’s obvious; producing more exports requires labor, it means more jobs.

TR: Having more jobs is bad?

Me: Of course it’s bad! Work is hard, that’s why they call it work. Work is so undesirable that you have to pay people to work. Visiting Disney World or going to a movie is fun; people must pay money to do fun things. Work is just the opposite; you must pay people to work. We’d have to work harder without getting to consume more.

TR: But you said the US already has a very low unemployment rate, so is it really likely that it can go much lower?

Me: Perhaps not, but in that case we’ll need to tighten our belt. It won’t be so much that we are having to work hard (we already work harder that the Europeans), rather a share of our income will be “garnished” by consumers in East Asia and Northern Europe. They will get to consume a part of our labor. They’ll be paid for our hard work.

TR: Is there any way to reduce the risk of this happening?

Me: Let’s begin by stop running $1 trillion budget deficits, which just add fuel to the fire. We’d have to slightly tighten our belts today, but it would impose less of a debt burden on future generations. In addition, it will make the future tax system less oppressive. Other Singapore-style, pro-saving tax reforms would also help.

PS. I have another piece on trade over at MoneyIllusion.

READER COMMENTS

Jon Murphy

Oct 9 2018 at 3:35pm

I suspect its unlikely that exports rise to meet imports in your scenario. It’s more likely, i think, that imports fall to meet exports (that is, a recession)

Scott Sumner

Oct 9 2018 at 6:13pm

Jon, You are right that imports might fall instead. But that’s not a recession (imports are not a part of GDP.)

In either case, it’s still true that we pay off these debts by working and not getting paid for that work (in consumption).

Jon Murphy

Oct 9 2018 at 6:26pm

You’re absolutely right. Forgive my imprecision. I merely meant a recession characterized by falling consumption, not necessarily the GDP conditions.

Scott Sumner

Oct 9 2018 at 7:48pm

Agreed, that’s perhaps called “tightening one’s belt”.

Benjamin Cole

Oct 9 2018 at 8:18pm

Well. Maybe there is a bit of straw in this Sumnerian version of Mr. TR.

Anyway, I suspect the reduction in wealth and income due to property zoning dwarfs that of Trump’s tariffs, which might accurately be called “Trump’s Tariff Tiffs.”

So why is the Libertarian and free-market crowd obsessed with global trade?

robc

Oct 11 2018 at 12:31pm

I have been writing about zoning all over the place, but you never comment on my posts.

Matthias Goergens

Oct 12 2018 at 5:58am

It’s easier to write comments complaining about stuff.

Don Boudreaux

Oct 10 2018 at 7:25am

Scott: Great post. But, Captain Ahab-like, I here again try to harpoon my personal white whale: not all of the U.S. current-account deficit is debt. Some of it becomes debt – as when non-Americans lend dollars to Uncle Sam. But there is no debt created when, for example, foreigners use dollars to acquire equity shares in American businesses, or when they simply hold dollars into future periods. (And, by the way, when foreigners acquire equity or real-estate in the United States, there is no necessary net reduction in Americans’ ownership of capital. There can be, but there need not be. It depends on the kinds of assets acquired or created here by foreigners, as well as on what American sellers of assets do with the proceeds of those sales.)

I justify my obsession with insisting that not all of the current-account deficit is debt because debt frightens people (often justifiably; often unjustifiably). One simple step that we can take to help to alleviate the vastly overblown fears of U.S. current-account deficits is to stop describing those deficits as increased American indebtedness.

art andreassen

Oct 10 2018 at 11:49am

Scott: GDP is net of total imports, consumption, investment , government and exports are not net of imports, that is why their sum is greater than GDP. If tomorrow consumption imported 100% of its spending rather than the 14% it now does PCE would not decline one cent but GDP would decline by 56%.

Scott Sumner

Oct 10 2018 at 12:07pm

Don, You are exactly right, and indeed I’ve made that point in other posts. Here I was trying to simplify the math to make a specific point, but that distinction is also quite important, and I should have pointed pointed it out.

Art, I’m not sure what point you are trying to make. Are you talking about sudden shocks, or long term processes that play out over decades?

Philo

Oct 11 2018 at 2:44am

“Visiting Disney World or going to a movie is fun,” as is reading a post like this one. “[P]eople must pay money to do fun things” usually, but mot always: thanks for not charging me!

Philo

Oct 11 2018 at 11:19am

‘mot’ => ‘not’

Warren Platts

Oct 12 2018 at 3:08pm

Scott, thanks for the post. I cannot recall a blog post by a free trader that has discussed the NIIP before.

Regarding eurozone unemployment rates, those nordic countries actually have very low rates:

Denmark 4.8%

Norway 4.0%

Germany 3.4%

Iceland 2.7%

The relatively high average unemployment rate is because of countries like:

Italy 10.9%

Spain 16.1%

Greece 20.8%

Which gets back to NIIP. It is the latter group of countries that are preview of what is in store for the United States if we not get the trade deficit under control. As you note, despite the NIIP of minus $8 trillion+ (which is basically the sum total of all our past trade deficits, adjusted for value), we nonetheless run a balance on primary income (the income we get our foreign investments minus the U.S. income foreigners get from their U.S. investments) is positive on the order of $200 billion.

However, as measured by % GDP, the NIIP/GDP has deteriorated badly in recent years. Pre-Great recession, it was like minus 10%; now it is minus 45% of GDP. The thing is, the NIIP/GDP ratio is basically a country’s credit rating. And when it gets past minus 60% GDP, it is like your credit rating falling to 400. No lender will touch you with a 10-foot pole. And even assuming the rate of growth of NIIP/GDP is linear, and not exponential, then, if you are not diagnosed with stage-4 cancer this year, you will likely live to see the crisis when it happens.

At that point, foreign “investors” will lose confidence in USA. They will pull their $$$, and the trade deficit will end, whether we like it or not, or whether you think it matters or not. And for once, Murphy above is actually right. There will be a financial crisis and a corresponding recession big enough to warrant the name GRII.

So this is basically the choice we have: we can do it the easy way or the hard way. That is, we can choose to end the trade deficit now on our own terms and manage it ourselves. Or we can simply wait, and let nature take its course: in the (near) future, we will simply let our foreign creditors manage the great unwinding for us. If the latter, however, it is not gonna be fun. Plenty of belt-tightening, yes, aka austerity, followed by another lost decade (or two or three).

Thus, it would be nice to get a little better economic advice other than saying we must cut Grandma’s $800 a month social security payment.

Jon Murphy

Oct 13 2018 at 8:58am

Two factual issues here:

With the exception of Germany, none of those countries are in the Eurozone

Germany is not a Nordic country

Comments are closed.