David Beckworth recently interviewed Chris Hughes, who wrote a paper entitled: “Rethinking Arthur Burns, the “Worst” Fed Chair in History.”

This is from the podcast:

There is demand-driven inflation headed into the early parts of Burns’ tenure, for instance in 1971, but then the real extreme periods of very high inflation in the 1970s, the first during Burns’ tenure, the second under Volcker, are the result of supply shocks in commodity and energy markets. So, you see, obviously the work of Alan Blinder on this has been formative for many, including myself, but you see core inflation going from about 4% in the late 1960s and early 1970s to around six by the mid to late 1970s, and then by the time we get on the other side of the Volcker shock, it comes back down to around four, but with these two very significant bumps, the first in 1973 and the second in 1979 and 1980, both of which related to geopolitical events, the Yom Kippur War, and then later the Iranian revolution and the Iran-Iraq war.

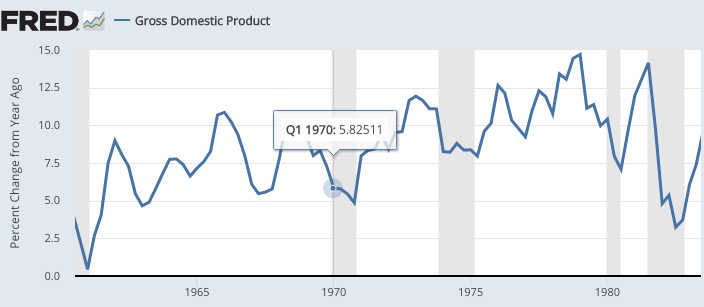

In my view, Burns’ tenure was even a bit worse than suggested by this quotation. Take a look at 12-month nominal GDP growth rates:

A few comments:

1. Under Fed chair William McChesney Martin, the inflation problem worsened during the 1960s. The problem was entirely demand driven; indeed the supply side of the economy did extremely well during the 1960s. Given those NGDP growth rates, it’s amazing that inflation was not even higher.

2. Arthur Burns was Fed chair from February 1970 to January 1978. At the end of the 1960s, a tight money policy had briefly reduced NGDP growth. So the situation inherited by Burns was not that bad. Unfortunately, he presided over an easy money policy that drove NGDP growth in the 1970s to rates even higher than those experienced in the 1960s. Thus “supply shocks” don’t tell us very much about inflation during Burns’ tenure (except during 1974). The problem was excessive growth in aggregate demand (NGDP).

3. By the time Burns left office in 1978, inflation had reached double digits. I don’t buy Blinder’s claim that core inflation was only about 6%. Closer to 8%.

Hughes has a nuanced view of the Burns’ tenure at the Fed:

Well, I think Arthur Burns is one of the most fascinating and overlooked figures in American economic history. I should say that I am under no illusions about the guy’s virtue. He made plenty of mistakes as Fed chair and my project here isn’t to try to paint him nostalgically as some hero that we can look back on. Instead, it’s to hold up a light to what in my experience is considered a kind of heresy. The idea that Burns was a leader of the Fed who operated from a place of ideological consistency, even conviction at times, and who importantly in his time was considered to be quite hawkish on inflation, which is just head spinning to people today.

It’s clear that the Fed performed very poorly during the Burns period. Any defense of Burns based on things like supply shocks won’t work. On the other hand, Hughes is correct that the political environment at the time was quite different than today. The zeitgeist within the economics profession was extremely dovish, and the Fed rarely deviates far from that consensus. Another Fed chair might well have produced similar results. Indeed, policy got even worse under ill-fated G. William Miller, who followed Burns and was replaced Paul Volcker after just 18 months as Fed chair. Even Volcker did quite poorly during his first 20 months as chair.

READER COMMENTS

Henri Hein

Jun 22 2023 at 2:00pm

Wouldn’t it be hard to compete with Mellon as the absolute worst? No matter what other virtues he had, being one of the principal catalysts* of the Great Depression must count as a disastrous negative.

*Or direct cause, I guess, depending on who you ask.

Andrew_FL

Jun 22 2023 at 2:20pm

Mellon was neither Fed chair nor one of “the principal [sic] catalysts” of the Great Depression

Scott Sumner

Jun 22 2023 at 2:48pm

Mellon was never a Fed chair. He was the Secretary of the Treasury, and a pretty good one AFAIK.

Henri Hein

Jun 23 2023 at 1:13pm

Thanks for the correction. I was confused by the footnote in this table on the Federal Reserve website: https://www.federalreserve.gov/aboutthefed/bios/board/boardmembership.htm

The Secretary of the Treasury served as Chairman until the Banking Act of 1935

But my question remains: who was responsible for the monetary policy 1928-1932, and how could Burns be considered worse than that?

Scott Sumner

Jun 25 2023 at 12:22pm

I had forgotten that. I gather Mellon delegated the chair position to someone else, but am not certain.

I believe the NY Fed president had the greatest influence, but the power was more dispersed than today.

MarkLouis

Jun 22 2023 at 2:31pm

It’s far too easy to throw around “supply shocks” to let central banks off the hook for high inflation. We should demand more rigor from economists. Industrial production grew over 3% pa during the 1970s – there was no major supply side issue.

Scott Sumner

Jun 22 2023 at 2:49pm

That’s right. It’s why I focus on NGDP growth, which is not impacted by supply issues.

spencer

Jun 22 2023 at 6:45pm

Dr. Leland Pritchard used to read Burn’s correspondence to his money and banking class. Prichard, who always wore a suit and tie along with his Phi Beta Kappa key, told the class that Burn’s problem was targeting interest rates as opposed to legal reserves. I.e., the trading pressure was always on the top side of the bracket, which the trading desk always accommodated.

Jim Glass

Jun 22 2023 at 6:57pm

Any defense of Burns based on things like supply shocks won’t work.

I’ll once more repeat what I always do when seeing claims that the 1970s inflation was caused by “supply shocks”, meaning dominatingly if not entirely the big oil price shocks from the Arab embargo and all…

In the USA inflation rose, in Germany prices were stable, in Japan inflation fell.

The USA had substantial domestic production of oil, which might be imagined to have cushioned the shock somewhat. (Though I was forced to gas up my teenager clunker-mobile only on days my license plate number allowed.) Germany and Japan had no domestic oil supply.

The Fed followed a policy cushioning the impact of the oil price shocks. The Bundesbank stuck to its policy of steady prices that it was truly and loyally wed to in memory of the hyperinflation. The BOJ stuck to a policy of disinflation that it had initiated before all the price shocks to reduce inflation from, IIRC, ~ 9%. And succeeded.

Andrew_FL

Jun 22 2023 at 10:36pm

Japan had a CPI inflation rate of 23% in 1974. Now, it did drop very quickly afterwards.

spencer

Jun 22 2023 at 7:01pm

The so-called “great inflation” was a direct result of the “monetization of time deposits”. All the devices which have in effect made time deposits an integral part of demand deposits, viz., daily compounding of interest, automatic fund transfers, etc., enabled people to economize on demand deposits, and resulted in the sharp increase in velocity since 1967.

In other words, under the existing institutional arrangements, an increase in time deposits resulted in an offsetting increase in transactions velocity – therefore no dampening effect resulted (up until 1981). If there was a growth in time deposits relative to demand deposits, there was an offsetting increase in velocity.

Today, we have the opposite senario.

spencer

Jun 23 2023 at 7:04am

It wasn’t a supply shock. It was an administrative price hike. Blinder is wrong. It’s money and banking 101. Any administrative price hike is deflationary unless validated by monetary policy. And OPECs price hike was more than validated. But the pundits aren’t smart enough to add up the #s.

spencer

Jun 23 2023 at 7:11am

It’s just another example that income velocity is fictitious.

Vivian Darkbloom

Jun 23 2023 at 7:50am

I’m always somewhat puzzled by the (over) assignment of personal credit and blame to the Federal Reserve Chairman for the performance of the Federal Reserve and the FOMC, as if he or she is in total control of what happens there. Does the Chairman have some special dictatorial powers I’m not aware of? Surely, the Chairman is the most powerful person on the Board–he or she is the public spokesman and, presumably, has some additional power of persuasion; however, the Board consists of seven members and, more relevant here, the FOMC consists of fourteen whose terms overlap the tenure of the respective Chairman or woman. Each member of the FOMC has one vote, each one equal in weight to the others. None of these additional members are appointed by the Chairman. Why, in relation to the Federal Reserve do the media and pundits tend to leave the impression that the Chairman is responsible for (nearly) everything? Qualfiers such as “under his tenure” are quickly overshadowed by the relative personification of the Board by the identity of the Chairman.

Perhaps I’m ignorant of the functioning of the Federal Reserve system; however, I can’t help in my own mind to compare the situation with, say, the Leader of the House of Representatives or the Chief Justice of the Supreme Court. These are also collegiate bodies and yet we don’t tend to assign credit and blame in nearly the same fashion as we do the Federal Reserve Board Chairman (e.g., “any defense of Burns”, etc).

Scott Sumner

Jun 23 2023 at 12:37pm

I agree, although in fairness the Supreme Court analogy is not exact. In practice, Fed chairs tend to be more influential that Chief Justices of the Supreme Court. They are rarely outvoted.

Vivian Darkbloom

Jun 23 2023 at 1:59pm

No analogy is ever exact–by definition. Nevertheless, one needs to ask the question why there are relatively fewer dissents on the FOMC than, say, the Supreme Court. I don’t think the reason is that the Federal Reserve Board Chairman has more official power or even unofficial persuasive power. My hunch is that the FOMC feels more the need to present its decisions with one voice and the Chair feels a need to vote with the majority whatever that may be—a big difference from successfully convincing others to vote with him or her. (Can one cite a single instance when the Chair dissented from a majority vote?) It is likely that the reported decisions are the result of compromises that are not part of the official record—compromises made not only by the Fed Chairman, but also individual voting members For example, the Chair might argue for a half point rise and can only get support for a quarter point rise. The end result is a vote of yay or nay and may or may not reflect the Chair’s personal conviction. Or, is it that FOMC voting members are lackeys compared with Supreme Court Justices?

In any event, I stand by the observation that there is too much of a cult of personality with respect to Fed Chairmen. It’s a gross over-simplification of the role in that the Chairman, like the Chief Justice, is not in a position to dictate voting outcomes.

Scott Sumner

Jun 25 2023 at 1:26pm

Again, I agree on your basic point. But even in the “backroom stage” where compromises are forged, the chair is highly influential, especially over other Board members (who are often far less experienced.) Yes, they arrange not to be outvoted, but they are also very influential in persuading others.

spencer

Jun 23 2023 at 8:00am

If the Chairman didn’t argue against a bad money policy, then they are to blame.

The current problem is that the demand for money is falling (velocity rising). The percentage of transaction deposits to gated deposits is growing. It is an historic reversal.

spencer

Jun 23 2023 at 8:24am

Powell just unleashed a lot of cash. (The FED’s GAAP accounting is wrong). The O/N RRP award rate is lower than 3-mo T-bills.

spencer

Jun 23 2023 at 2:12pm

As an example, Jerome Powell is to blame:

#1 “there was a time when monetary policy aggregates were important determinants of inflation and that has not been the case for a long time.”#2 “Inflation is not a problem for this time as near as I can figure. Right now, M2 [money supply] does not really have important implications. It is something we have to unlearn.”#3 “the correlation between different aggregates [like] M2 and inflation is just very, very low”.

Grand Rapids Mike

Jun 24 2023 at 11:55am

Regarding number 2, wonder if Powell has changed his position on M2. Interesting how the Fed could disregard Milton Friedman position on the cause of inflation so quickly.

spencer

Jun 23 2023 at 2:15pm

Another example: Velocity: Money’s Second Dimension – By. Bryon Higgins

“Money has a ‘second dimension’’, namely, velocity . . .. ” Arthur F. Burns in Congressional Testimony.

Comments are closed.