During a normal demand-side recession, wage growth tends to fall sharply, with a modest lag due to nominal wage stickiness. In this recession, however, it’s been hard to interpret the data due to “composition effects”. Put simply, lower paid workers were more likely to get laid off, so average hourly wages actually rose faster than normal last year.

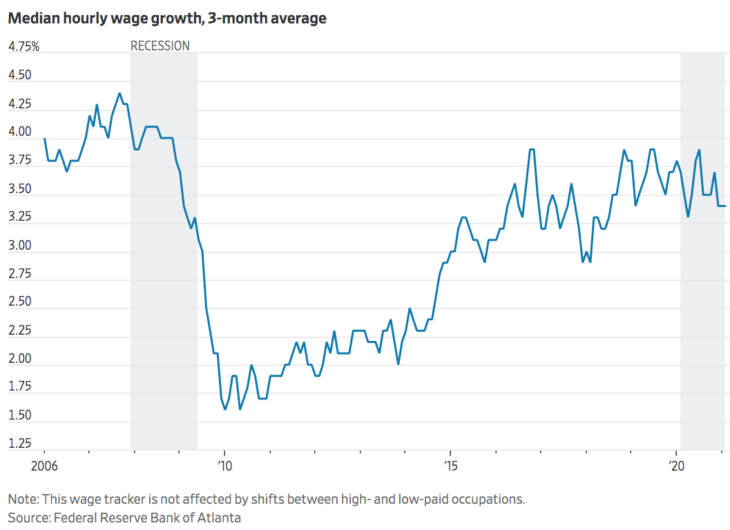

Fortunately, the government has another wage series that compares wage growth within a given job category. This shows average wage growth to have been relatively steady over the past year, which is still a bit surprising. Wage growth normally slows sharply during severe recessions:

Wage growth still might slow sharply, after all, wages respond with a lag. But given the severity of the slump last March and April, I’d expect to see some evidence by now. In the case of 2008, the severe slump didn’t begin until the second half of the year, and then wage growth fell a few months later.

One possibility is that this time the recession reflects a decline in both aggregate demand and aggregate supply, so the overall effect on the price of labor is relatively small, even as quantity falls sharply. (Never reason from a quantity change.)

This fits in with all sorts of other evidence that this recession is unusual. For instance, output and employment bounced back after the April 2020 slump much faster than after previous recessions. Indeed the actual downturn lasted only two months. Here’s the Wall Street Journal, discussing reports that companies are having trouble finding workers:

One shouldn’t put too much weight on anecdotes, but these are corroborated by data. Some 7.4 million jobs were open in February, above the pre-pandemic level. By contrast, job vacancies plummeted by half in 2007-09.

Mainstream economists tend to assume that causation goes from high unemployment to falling wages. In my view, the root cause of most recessions is tight money, which reduces the equilibrium average wage rate faster than the decline in actual wages. Because actual wages fall more slowly than equilibrium wages, the price of labor is too high. This causes mass unemployment. This recession was not caused by tight money, however, and hence there was no necessary reason for high unemployment to be correlated with falling wage growth.

To summarize, when we finally get a recession caused by real factors, not a demand shortfall, we can see how different it is from normal recessions. That should make us even more confident that most normal recessions are basically monetary problems. (During my life, the 1974 recession was the one with the largest “real” component—prior to Covid-19.)

One other point. Although I often advocate NGDP targeting, in some models nominal wage targeting does even better. If money were too tight then wage growth would be falling, and vice versa. In my view, the stability of nominal wage growth suggests that monetary policy has been roughly on target during this period.

READER COMMENTS

BJH

Apr 22 2021 at 8:14am

This is just composition effects, no? Low-wage workers were more likely to get fired than high-wage workers. So median hourly earnings among the employed have gone up or stayed constant.

BJH

Apr 22 2021 at 8:16am

Oops, apologies, I completely missed your first paragraph. But how does the graph control for composition? Or, where is the data on “wage growth within job category” (which could still have composition effects)?

JFA

Apr 22 2021 at 9:14am

I believe this is the data being referred to: https://www.atlantafed.org/chcs/wage-growth-tracker?panel=1.

Composition effects are usually thought of as changing the mix of high-skill vs. low-skill, so if you control for that, then composition isn’t such a big deal. I believe they use this list of occupation codes (https://cps.ipums.org/cps/codes/occ_2020_codes.shtml) to categorize the job category skill level. You can also view it by education level, since education is a strong correlate of job skill level.

You might be concerned with the composition of the unemployed vs. the employed. From the methodology section, the data are for wage and salary earners, so presumably the unemployed are not part of calculating these data.

Scott Sumner

Apr 22 2021 at 3:32pm

Thanks JFA. That information is useful.

In any case, the difference between 2008 and 2020 is striking, and presumably the same technique was used in both cases.

Bill Conerly

Apr 22 2021 at 3:58pm

In my view, the root cause of most recessions is tight money, which reduces the equilibrium average wage rate faster than the decline in actual wages. Because actual wages fall more slowly than equilibrium wages, the price of labor is too high. This causes mass unemployment.

Keynesian theory: recession are caused by demand shocks in an economy with sticky wages.

Keynesian policy: fiscal policy to mitigate demand shocks.

Why not: government policy to make wages more flexibles? Like all government labor contracts no longer than one year, or one quarter. Automatic downward adjustment (based on unemployment rate) of minimum wage and prevailing wage calculations. Maybe prohibit as not in the public interest private labor contracts extending more than a year or a quarter.

That this has not been suggested argues that Keynesian policy is a mix of short-run policy and a long-term preference for bigger government.

Am I wrong?

Scott Sumner

Apr 22 2021 at 7:18pm

Yes, you are wrong on all counts. Sticky wages do not call for fiscal policy (which I oppose.) I’m not a Keynesian, and I don’t regard the sticky wage model as Keynesian.

And no one knows how to make wages so flexible that demand shocks don’t matter.

Matthias

Apr 23 2021 at 4:46am

Yes, though we know some things which make wages more or less flexible.

Kailer Mullet

Apr 22 2021 at 8:00pm

I’m interested in the next two years when household savings isn’t there to counter public deficits, will the central banks have the nerve to offset the fiscal policy. I too used to roll my eyes at inflation hawks back in 2009-10, but this time I’m a bit more worried. Politicians have now completely tuned out anyone who says deficits matter and it feels a bit like the pre-pandemic world where people didn’t really think there could be a big 1918-style pandemic given advances in public health.

MarkLouis

Apr 23 2021 at 3:16pm

There is a news story out today that some Democrats are pushing to make the expanded unemployment benefits permanent. IF that were to happen, and if the Fed targets the unemployment rate, doesn’t that defacto allow the government to set the price-level?

Art Andreassen

Apr 23 2021 at 5:30pm

Scott: This is way off topic but I have to ask you if you have read Jeff Booth’s “The Price of Tomorrow”? He is a technology investor who is addressing the deflationary impact of technological changes that will exponentially increase in the future. His premise is that our present monetary system can not handle the job loss and price declines that increased productivity will cause.

A warning, he discusses Bitcoin.

I know you are not a fan of YouTube but there you can find a number of interesting discussions with him so you could get a feel for his point of view before buying the book. I was impressed by his demeanor.

His book got me thinking about the BLS PPI deflation process and how BLS increases real dollar output values based on its estimate of quality improvements, for which there are no offsetting estimates for inputs. Isn’t this difference due to the BLS adjustment between the current dollar and the real dollar values of output actually a measure of the loss of wages in real terms?

Scott Sumner

Apr 23 2021 at 5:53pm

I’m very skeptical of those sorts of claims, which we’ve been hearing for more than 200 years, and they’ll always been wrong. We aren’t even seeing a tiny indication of faster technological growth. I’ll believe it when I see it. In any case, it’s not a problem for monetary policy, it’s a problem (if at all) for the welfare state.

I don’t understand your last question.

Thomas Lee Hutcheson

Apr 24 2021 at 8:04am

I’d say that the fall in real income was indeed partly a supply side phenomenon: people feared going to work, firms had to reduce output to comply with (often unwise and excessive) anti-spread restrictions, workers were sick or died. But it was also a demand phenomenon as shown by the fall in inflation expectations and this was clearly the fault of the Fed that did not “flood the zone” to keep NGDP or even inflation on track.

art andreassen

May 1 2021 at 8:00am

Scott: Jeff Booth’s book, “The Price of Tomorrow”, includes a discussion of the monetary impact of deflation which you may find interesting.

My question about the BLS’s price calculation of PPI is whether the resulting BLS increase in real dollars is not a measure of the deflation brought on by technology. I do not understand the lack of interest on the part of economists in knowing the total value that BLS increases real GDP. The BLS can publish this value in total and by industry since they are derived in the calculation. Doesn’t this real increase in GDP have an impact on every equation which incorporates it?

Booth has an interesting example about lidar. He mentions a magazine article that said self driving cars were not a possibility because, at the time the article was published, lidar costs $60,000. Now lidar costs $5. This brings up the question of why the BLS deflation process does not now value the real dollar of a car $60,000 more than they do?

Comments are closed.