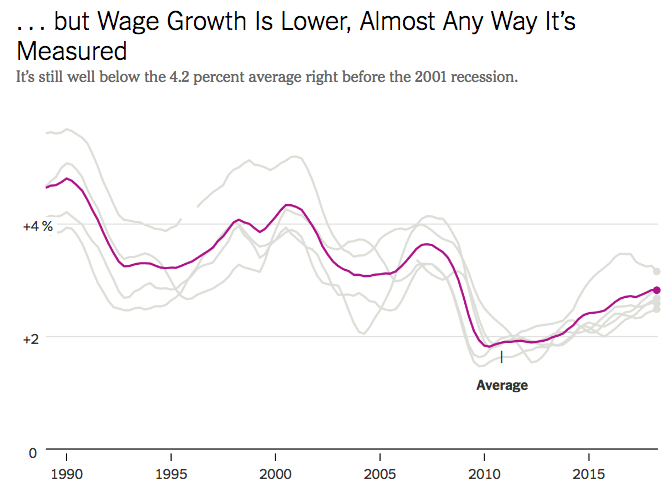

The New York Times has a graph showing a slowdown in the rate of nominal wage growth, compared to the 1990s:

They then argue that this is a sort of mystery, which cannot be explained by slowing inflation:

So why has wage growth slowed since 2001, across many different measures, when unemployment is so low?

We can rule out two possible reasons immediately. It wasn’t because of a decline in inflation, and it wasn’t because benefits like health insurance and hiring bonuses crowded out wages.

As with wages, the government has many different inflation measures. But none that we analyzed have slowed by nearly enough since 2001 to explain the weakness in wage growth; some have even increased a bit.

And government data suggests that measures of pay growth that include nonwage benefits are also below their 2001 levels. Moreover, the fastest growth in nonwage benefits was before 1994; in recent years, the nonwage share of compensation has grown more slowly.

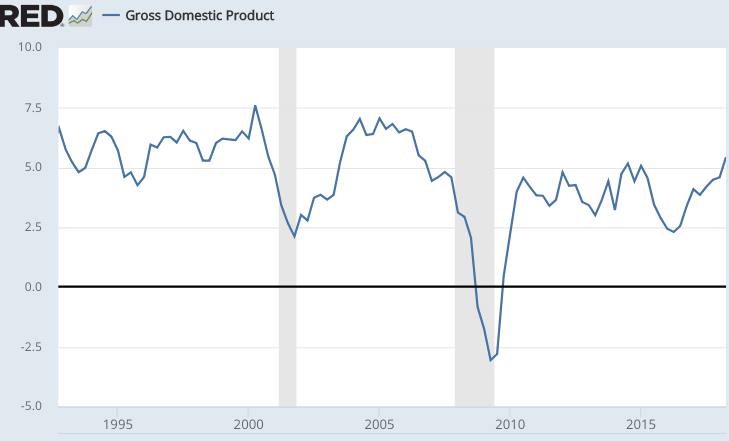

But inflation is the wrong variable; it’s NGDP growth that determines wage growth, not inflation. And NGDP growth has slowed since the 1990s, indeed it’s slowed by roughly as much as wage growth has slowed:

Note that NGDP growth generally runs a bit higher than nominal hourly wage growth, because employment also trends upward over time.

Note that NGDP growth generally runs a bit higher than nominal hourly wage growth, because employment also trends upward over time.

There’s no wage mystery. When NGDP growth slows, wage growth will usually (not always) slow as well. If you want faster nominal wage growth, then adopt a more expansionary monetary policy. If you want faster real wage growth, then deregulate the economy and do tax reforms that encourage saving. Printing money won’t boost real wages.

(David Henderson has a recent post showing that real wages are doing better than is widely reported, if measured properly.)

HT: Stephen Kirchner

READER COMMENTS

Thaomas

Oct 24 2018 at 1:28pm

Deregulation (of those regulations that do not pass cost benefit criteria) and tax reform to increase saving (a progressive consumption tax and a VAT instead of the capped wage tax that funds SS and Medicaid) is good for raising real wages, but so would tax reform to tax externalities like net CO2 emissions, regulations that DO pass cost benefit analysis, fiscal policy that regulates surpluses/deficits according to a NPV criteria (presumably surpluses when the economy is near full employment like now), monetary policy that targets constant price level growth and low unemployment of all factors of production (approximately constant NGDP level growth ), and immigration reform to attract more young high skilled and educated immigrants. And since these will take time to reverse the slow real wage growth in recent decades, a much higher EITC to raise after tax wages of low income people.

robc

Oct 24 2018 at 2:02pm

According to a Coase interview (Reason mag) from about 20 years ago, those don’t exist anymore. We are past the point where any new regulations can survive the law of diminishing returns.

Thaomas

Oct 24 2018 at 2:31pm

Regulation is not unidirectional. That sounds right on average, but with technical and economic change constantly going on, all margins must be shifting, some toward more some toward less (although many of the “more” are probably better accomplished by fees or taxes (congestion taxes, for example) rather than quantitative regulation).

Thaomas

Oct 24 2018 at 2:33pm

My bad! I omitted removal of trade restrictions. True, that is a form of “deregulation,” but certainly not what politicians who talk about “deregulation” mean.

Marcus Nunes

Oct 24 2018 at 2:35pm

That’s true.

http://ngdp-advisers.com/2018/07/07/contrary-popular-opinion-low-rate-unemployment-not-signal-strong-labor-market/

nobody.really

Oct 24 2018 at 3:49pm

MORE expansionary than quantitative easing? How did we manage faster nominal wage growth in the past without such herculean measures?

MORE deregulated than today? Sure, we’ve had Obamacare and some CO2 regulations. But deregulation has swept the nation since 1990. We deregulated much of the electricity market in 1992, interstate bussing/trucking in 1994, telecommunications in 1996, natural gas choice in the late 1990s, ocean shipping in 1998, the Glass-Steagall Act in 1999. And this doesn’t even address the removal of all kinds of barriers due to the rise of the internet, cell phones, and ever-more-prevalent electronic financial transactions. I have a hard time believing that today’s businesses and consumers face more impediments than they did in 1990.

MORE savings than today—for what? Aren’t firms still sitting on mountains of cash? Moreover, there are not only plenty of investment funds and angel investors, but people can simply ask for cash with a Go Fund Me account. More savings might be salutary for other reasons, but I don’t see how throwing more savings on the existing piles of cash would boost real wage growth. Given that interest rates have only barely grown above 0%, is liquidity really a problem?

It’s hard to look at the trends and see a strong correlation between deregulation, aggregate savings, and real wage growth.

robc

Oct 25 2018 at 2:13pm

We haven’t dergulated on net, as the federal register is growing, not shrinking.

RPLong

Oct 24 2018 at 4:02pm

Even if NGDP growth is down, we’re still yet to explain why unemployment is so low despite slowing wage growth rates. Just as the Times article states:

Note that the article points to record-high job openings and an increasing labor participation rate. If the Times‘ researchers are unable to account for inflation component of slowing NGDP growth, then isn’t pointing to slowing NGDP growth despite inflation-adjustments is really equivalent to pointing to slowing RGDP growth? And if so, how do you square that with a booming labor market?

Of course, the NYT article settles on one explanation you omitted: slowing productivity:

I, personally, favor this explanation. Note the focus on “advanced economies.” If the laborers in advanced economies are being out-bid on the international labor market by competitors from developing economies, then isn’t this precisely what we’d expect to see? Wouldn’t we expect slowing wage growth across advanced economies, significant wage growth across developing economies, and decreasing advanced-economy productivity as MNEs discover that they can buy equivalent computer programming, engineering, and management consulting from the BRICs compared to buying them locally?

Scott Sumner

Oct 24 2018 at 4:55pm

Nobody. There are probably more regulations today that at any previous point in US history—tens of thousands of them, and more every day.

As for monetary policy, don’t confuse QE with easy money. The Fed had no difficulty pushing NGDP growth above 5% in the 1990s, what makes you think it would be difficult today? Do you think the Fed is currently raising rates because they have difficulty getting faster NGDP growth, or to prevent NGDP growth from rising?

nobody.really

Oct 24 2018 at 6:11pm

And from that fact, you conclude … what?

Imagine an agency adopts a regulation saying “Do X.” Then the agency adopts a second regulation that says, “Alternatively, you can do Y.” Obviously you must concluded that this would crush the economy—after all, it resulted in twice as many regulations! Or you could conclude that this change has granted people greater freedom than before, even if doing so required more words, and that counting “regulations” is a poor proxy for anything.

Deregulation was always a bit of a misnomer; it was generally different regulation. De-regulation of railroads, landline telephones, electricity grids, and interstate pipelines generally involved eliminating monopoly grants—and the advantages that came with them. And this latter part of the equation almost always involved a huge amount of scrutiny to keep the incumbent from exploiting new entrants. If your goal was having fewer regulations—that is, fewer words on a page, not greater freedoms—then you probably favor monopoly franchises.

Likewise, many people decry the complexity of the income tax code. But the bulk of the complexity arises from optional mechanism that enable people to REDUCE their tax bills. Don’t like the complexity of itemizing your deductions? Don’t. Don’t like the complexity of putting funds into pre-tax accounts? Don’t. Don’t like the constraints of qualifying for 501(c)(3) status? Don’t. You can achieve greater simplicity–at the cost of paying higher taxes. But the fact that plenty of people DO take advantage of these provisions tells me that people DO like the added complexity.

Finally, regulations strike me as a trivial burden compared with lack of technology. Look at all of today’s internet businesses: They didn’t exist in 1990—not due to regulatory burdens, but due to lack of technology. Comparing the burdens of doing business today—even with all the new regulations—to the burdens of doing business in 1990, the current era seems pretty favorable. Even if you have more forms to fill out, you can fill them out on-line.

Still, today’s compensation growth seems to lag….

Ok, you’ve lost me here.

I understand the Fed to raise interest rates to limit inflation, even if this has the ancillary effect of dampening GDP growth. Thus, I guess we could characterize their behavior as seeking to limit the rise of nominal GDP–if we focus on the nominal part.

I guess that if we simply let inflation run amok, we could get higher nominal compensation growth. But from 1993 to the 2008 crash, inflation seemed well constrained around 2.5% or so, yet (nominal) compensation growth seemed to be stronger. What am I missing?

Thaomas

Oct 26 2018 at 3:44pm

The “difficulty the Fed had in keeping NGDP rising at a constant rate was the political pressure they were getting from inflation hawks who, unlike neo Keynesians, were experiencing inflation just around the corer.

Benjamin Cole

Oct 24 2018 at 9:54pm

Getting rid of property zoning, or perhaps better termed residential housing supply controls, might result in higher real wages at the same time you get much lower inflation rates, as measured.

Indeed, for large swaths of the US economy, property zoning is probably the primary structural impediment.

Mark Z

Oct 24 2018 at 10:57pm

Doesn’t the claim that ‘lower NGDP growth has caused lower wage growth’ necessitate that either 1) lower inflation has caused lower wage growth, or 2) that lower RGDP growth has caused lower wage growth? Or some mixture of both? The NYT may just be assuming (perhaps too hastily) that a decline in real productivity in the past ~20 years can’t be a factor, and that, given our original proposition that NGDP growth determines wage growth, it must be the inflation component that’s explaining the decline in wage growth. And if it isn’t that, it’s a mystery. Though, I guess the real “mystery” they should be writing about wouldn’t be “why are wages growing more slowly” (as you point out, it’s slower NGDP growth), but rather, “why is NGDP growing more slowly?”

RPLong

Oct 25 2018 at 7:45am

You have it right, in my view.

I wrote a lengthy comment that I think got caught up in spam filtering because I quoted parts of the NYT article that had lots of links. Anyway, Scott Sumner is in a bit of a pickle here, because it’s hard to explain why the economy has record-low unemployment and record-high job offers, but that inflation doesn’t explain slow wage growth. Like you point out, if all this is true, then Sumner seems to be suggesting that slower RGDP is driving slower wage growth. But that would be an odd claim to make during such a booming labor market. I’m interested in hearing what he thinks the mechanism is.

As I pointed out in my lost comment, a compelling explanation in my view is that productivity is slowing down in advanced economies because high-skill labor can be had for a lower price in developing economies. Or, more accurately, it only looks like developed economies have higher productivity because up until now, programmers and engineers in New York weren’t competing against people in Hyderabad. But they are now. Given this, we’d expect to see rising wages in the developing world, slowing wage growth in the West, and decreasing measures of Western productivity even despite a booming economy.

But that’s just my opinion.

Ahmed Fares

Oct 24 2018 at 11:17pm

“it’s NGDP growth that determines wage growth”

Shouldn’t it be productivity growth that determines wage growth?

GDP growth is a combination of labor force growth plus productivity growth. The part of GDP growth due to population does not improve wages as the larger GDP is spread over a proportionately larger population. It is only the remaining productivity portion of GDP growth which ends up in wage growth.

Incidentally, countries like Japan can become richer, on a per capita basis, if their GDP declines and their population declines at a faster rate.

Sometimes bad news, like falling GDP, is good news.

Scott Sumner

Oct 25 2018 at 1:56am

Ahmed. The fact that people take advantage of complex tax breaks does not imply they like complexity. Rather it suggests the cost of complexity is lower than the tax break. Even so, most people would be better off with a simpler system. Tax breaks are not free money, they must be offset with higher rates.

I don’t understand your point about regulation.

It’s true that NGDP growth per capita is closer to wage growth, but that has slowed just about as much as overall NGDP growth, so my point remains the same.

Ahmed Fares

Oct 25 2018 at 2:21pm

Dr. Sumner,

I think you were responding to someone else as I said nothing about tax breaks, regulation, etc.

My comment was simply that wage growth should correlate with productivity, not GDP growth, because the latter also includes population growth.

(I’m sure you’re aware of that but sometimes people forget so please take my comment in that light.)

Thaomas

Oct 26 2018 at 3:49pm

The bigger reason that slow wage growth need not be a “mystery” is that their is simply no reason to expect wage share of output to remain the same. On may think that slow growth in wages is a problem to be fixed and want to identify the way increases in output affect the demand for labor, but the starting point need not be that wages always make up the same share of GDP.

Comments are closed.