Last year, the consensus view of economists called for a recession in 2023. At the time, I said this sort of prediction is foolish, as the science of economics has no method for predicting turning points in the business cycle. It was akin to astronomers trying to emulate astrologers, and made the profession look foolish. And this wasn’t the first time; economists have failed to predict any of our recent recessions. We should not even try—leave prediction to the asset markets.

Nonetheless, there was some reason to believe that a recession was a bit more likely than usual. After all, the US was suffering from high inflation, and anti-inflation programs are often associated with recessions. So why did no recession occur in 2023? I see three reasons, each of which is important:

1. The wrong Phillips Curve

2. Immigration

3. Gradualism

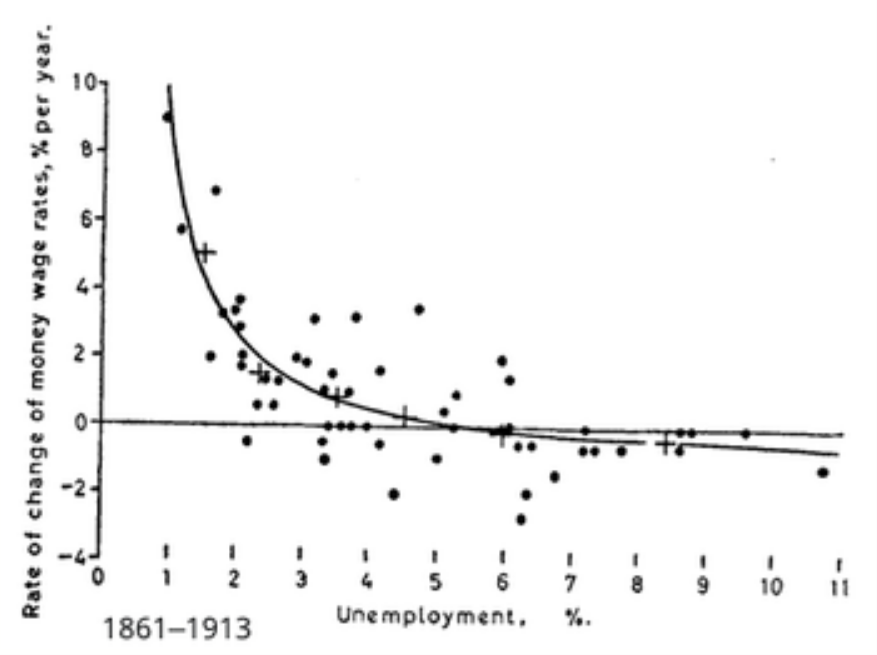

Back in 1959, Bill Phillips graphed the relationship between inflation and unemployment. Not the relationship between price inflation and unemployment, rather the relationship between wage inflation and unemployment (which is negative.) Almost immediately, Keynesian economists like Paul Samuelson and Robert Solow saw the value in the model, but decided that wage inflation should be replaced by price inflation. But guess what—those brilliant American economists were wrong and the obscure New Zealand economist was correct; the Phillips Curve should use wage inflation, not price inflation. That’s because the high unemployment associated with disinflation occurs because the equilibrium wage falls faster than the actual wage, during periods where wage growth is slowing. This leads to high unemployment.

During 2022, annual CPI inflation peaked at over 9%, and has since fallen to less than 4%. That sounds like a lot of disinflation. But price disinflation doesn’t matter, only wage disinflation causes high unemployment. And thus far were have seen much more modest wage disinflation:

Nonetheless, even that degree of wage disinflation might normally be expected to produce a mild recession. But as the Wall Street Journal recently pointed out, a massive surge in immigration has helped to moderate wage growth, without reducing employment:

There have been more immediate effects, too. The U.S. probably owes its soft landing—declining inflation without a big rise in unemployment—in part to the influx of foreign workers who have, according to Federal Reserve officials, helped alleviate labor market pressure. For better or worse, America’s semiporous southern border can act as a safety valve when the economy overheats, drawing in low-skilled workers and making the emergence of a wage-price spiral and persistent inflation less likely.

Another WSJ article provides specific data:

The precise scale of that economic boost was laid out in the Congressional Budget Office’s latest long-term budget and economic outlook, released Feb. 7. It estimates the labor force will be larger by 1.7 million potential workers in 2024 and 5.2 million more—about 3%—in 2033 than the nonpartisan agency expected one year ago. Gross domestic product—the value of all goods and services produced in a year—should be 2.1% larger. . . . More than 2.5 million migrants crossed the southwest border in 2023, according to the Department of Homeland Security. That resulted in net immigration of 3.3 million people last year, up from an annual average of 919,000 in the 2010s.

Back in 2022, I did a bunch of posts discussing the acute labor shortage. Without a sudden surge in immigration, this would have led to higher nominal wages, making disinflation much more painful. Many immigrants are applying for asylum and are allowed to work while their claims are being processed. (Whether you think this is good or bad has no bearing on the question of whether they help to explain the strong labor market.)

The third factor is gradualism. The Fed is trying to slow NGDP growth at a gradual pace. If NGDP growth were to slow too rapidly, we’d have a recession. If it did not slow at all, then inflation would not come down. Obviously, it’s not easy to “thread the needle” and achieve exactly the right pace of disinflation. I certainly would have preferred that they move more aggressively in late 2021 and throughout 2022 and early 2023, when there were labor shortages. Even so, slowly but surely they have been slowing the rate of NGDP growth and wage inflation, although there is much more work to be done. It is still quite possible that the “last mile” of inflation reduction leads to a recession. It won’t be easy getting nominal wage growth down from the current 4.3% to a figure closer to 3.3%. (Ignore price inflation—wage inflation is the real story when it comes to stabilization policy.)

To be clear, I am not saying that the US has achieved a soft landing, or will achieve one in the near future. Some recent statements by Jay Powell give reason to be concerned about the Fed’s commitment to 2% inflation. I still think the so-called “flexible average inflation targeting” policy has been something of a fiasco. The Fed is obviously not committed to an average inflation rate of 2%, and thus they never should have said that they were.

PS. A few comments on the wage graph. Because of “composition bias” (low wage workers are fired first), average hourly earnings often spike during recessions, even as the underlying wage rate for any given job category declines. That effect was especially pronounced during Covid, but also appeared in 2008. In addition, “money illusion” makes it hard to reduce nominal wages for any given job. Because some workers (teachers, nurses, police, etc.) get pay increases even during periods when the overall economy is weak, the overall average wage rate generally rises at least 2%/year, even in during periods of high unemployment. (This was not true under the gold standard, when wages occasionally fell.) Thus it took the labor market years to recover from the severe shock to NGDP in 2008-09.

PPS. Public opinion polls (which I don’t trust) suggest that Americans view the US economy as “poor”. But the foreign media is in awe of the strength of our economy, in contrast to weaker economies in Europe and Asia:

READER COMMENTS

MarkLouis

Mar 24 2024 at 7:58pm

Shouldn’t a decision like abandoning a 2% inflation target require congressional approval? There are very large distributional consequences (probably larger than many policies we label “fiscal”)?

Michael David Sandifer

Mar 24 2024 at 11:48pm

The Fed effectively loosened policy last week, despite inflation remaining high and every indication that both they and the markets expect rate cuts to start this year. The 5-year breakeven is continuing to rise above the Fed’s 2% target in core PCE terms. This is perplexing. The Fed should have signaled that it was delaying rate cuts versus expectations, at least.

Additionally, the current gap between the NGDP growth and the S&P 500 earnings yield is still large, and as you often point out, NGDP growth is still well-above the pre-pandemic trend. There’s every indication that monetary policy is too loose right now.

That said, there are also indications that the economy is still expected to slowdown and approach equilibrium over the next couple of years. I just don’t understand why the Fed wants to risk another inflation burst.

MarkLouis

Mar 25 2024 at 8:37am

Agree, but worst of all there is no coherent Fed explanation. Powell stammered when repeatedly asked about inflation. That communications void is rapidly being filled by the narrative that the Fed has become politicized and is trying to get Biden re-elected. True or not, letting that narrative fill the void is terrible for Fed independence.

Michael David Sandifer

Mar 25 2024 at 9:07am

I don’t see how this helps Biden. The Fed would be better off on the slow glide path they were on. Risking letting inflation expectations get unanchored again increases the risk of further mistakes that could lead to recession.

MarkLouis

Mar 25 2024 at 9:47am

The argument would be it’s a play on timing. You get the asset appreciation fist (already happening) but the inflation down the road.

bill

Mar 26 2024 at 10:54am

Can you explain more about the links between SP500 growth and NGDP growth? I haven’t seen that connection made before. Thanks!

MIke Sandifer

Mar 26 2024 at 3:46pm

Bill,

Neoclassical growth theory says that the mean nominal economic growth rate and the mean return on capital should be equal, at least in the long run. Hence, the mean NGDP growth rate and the mean S&P 500 earnings yield should have an equilibrium relationship. And, in fact, the difference between the two since 1990 is only 0.04%. Most of the time however, there is disequilibrium, as monetary policy is far from perfect. Hence, one can interpret divergences as NGDP output gaps.

This doesn’t work well if you use the typical 12-month trailing earnings yield, but if you just annualize the concurrent earnings yield, it seems to work pretty well. You can see a chart on my latest blog post, if you’re interested.

There are ways to make this forward-looking, by using S&P 500 earnings forecasts, S&P 500 futures, and various NowCasts and GDP forecasts, such as those offered by the Fed. One can also try to extrapolate from trend growth rates.

Back to the chart I mentioned, it shows that monetary policy was too loose during the internet boom of the late ’90s and early ’00s, and too loose during the Great Recession and the long recovery.

Michael Sandifer

Mar 26 2024 at 11:19pm

I meant to show the chart shows that monetary policy was too tight during the Great Recession and the slow recovery.

Scott Sumner

Mar 25 2024 at 1:25am

Congress did not set that specific target. Of course Congress has a right to require the Fed to set a 2% target, but it would be very difficult to get that sort of legislation through Congress.

Another option is to bring Powell in to testify, and grill him on how the “average inflation target” of 2% is supposed to work. Why is inflation consistently averaging more than 2%?

Craig

Mar 25 2024 at 9:05am

“Another option is to bring Powell in to testify, and grill him on how the “average inflation target” of 2% is supposed to work. Why is inflation consistently averaging more than 2%?”

These are questions the world’s largest debtor likely doesn’t want to ask or for the bond market to contemplate. Abandoning 2% amounts to a partial ‘default’ — the US govt isn’t going to default by not paying the dollar obligations, it will default by paying back dollars that simply buy less. We’ll see how it plays out, I can also see a productivity miracle, but the US has a debt problem and the incentive is there to give creditors a haircut. Let’s rwmember JP is accommodating them. Congress is going to bring him in and grill him? Chutzpah.

Jose Pablo

Mar 26 2024 at 8:24pm

Abandoning 2% amounts to a partial ‘default’

No, abandoning 2% amounts to making the narrative match reality. Average American inflation has never been 2%. Being honest can only help debt markets (although most likely it would be totally irrelevant. Debt investors already know).

the US govt isn’t going to default by not paying the dollar obligations, it will default by paying back dollars that simply buy less.

the US has a debt problem

Looking at your first statement it looks much more like the creditors (not the US government) have a “US debt problem”.

And they (the creditors) seem very happy with it, by the way.

You sell non-collateralized debt that you can repay with “pieces of papers” that you print yourself in your own “garage”. And you are pretty open about it, you don’t fool the buyers. They are well aware of this reality.

And, even knowing that, they make you pay interest rates well below those of any other sound lender offering very real liquid easy to execute collateral.

Where, exactly, is the problem?

Craig

Mar 27 2024 at 12:23am

“Where, exactly, is the problem?”

Well, then just QE it all away and be done with it.

Jose Pablo

Mar 27 2024 at 7:06pm

No Craig! You never rush the execution of your worst-case scenario plan. And don’t worry creditors already know that you have this option (it is implicit in the “sovereign” of “sovereign debt”)

Just follow Scott’s advice. Don’t listen to the economist’s prediction about the future path of US sovereign debt markets. Listen, instead, to what this “asset market” is “telling” us.

What seems to be, “please give us more of this wonderful commodity. We can’t have enough of it“.

Unless you have some privileged information about the sustainability (or its lack of) of government debt unknown to the markets.

Craig

Mar 25 2024 at 8:58am

I’m still Team Hard Landing given yield curve, Conference Board leading indicators, I see divergence between Household and Estabkishment surveys, and rising rates starting to impact some ZIRP financed zombie companies. Could I be wrong? Of course. To me its about probabilities and possibilities and not certainties. My bull case is that the US already had the recession, a mild 2 quarter negatice GDP in 2022 and also 2020 pandemic cleared out alot of dead wood. We’ll see.

Scott Sumner

Mar 25 2024 at 10:28am

“My bull case is that the US already had the recession, a mild 2 quarter negative GDP in 2022”

I don’t know how many times I’ve swatted away this myth. Two negative quarters is not the official definition of recession, nor is it a sensible definition. The US economy was obviously booming in 2022. If you wish to focus on one area, look at the job market.

Craig

Mar 25 2024 at 11:06am

Who cares? Its semantics, the point remains that the bull case is: no recession because the soft landing may have already happened. Call it a mild recession or simply ‘two quarters of negative GDP growth’ — makes no difference to me.

Craig

Mar 25 2024 at 11:56am

But in amy event, BEA definitions notwithstanding I’d be curious to hear your thoughts on a non-recessionary yield curve inversion? Is it as simple as just chalking it up to the bond market being ‘wrong’?

Scott Sumner

Mar 25 2024 at 8:38pm

An inverted yield curve doesn’t necessarily imply the bond market expects a recession.

And it’s not just “semantics” if you think 2022 helped to achieve a soft landing—the economy overheated in 2022.

Craig

Mar 26 2024 at 7:59am

Well, I remain in Team Hard Landing but it absolutely is semantics because the pandemic recession was the major event and whether you call Qq and Q2 negative GDP a recession or thr ‘insanely ultra mild barely a recession that even the BEA didn’t officially call a recession’ or even if we presuppose that those quarters were just a hard 0 the bull case doesn’t change, their point, which is not mine is that whatever recession you were going to have — you had it already, the economy ‘soft landed’ or perhaps ‘no landing’

Scott Sumner

Mar 26 2024 at 11:24am

It wasn’t even close to a recession—it was a boom.

Craig

Mar 26 2024 at 12:02pm

Well, most people don’t call negative GDP growth a boom. Now you very well might want to describe 2022’s FOUR quarters as a ‘boom’ that’s up to you. Those two quarters WERE negative though and there’s people today saying that the predicted recession, quite probably the most predicted recession ever is not going to happen because ‘it happened already’ that Q1 and Q2 2022 were ‘as bad as it was going to be’ put whatever label you want on it, semantics.

Brent Buckner

Mar 25 2024 at 10:31am

You wrote: “We should not even try—leave prediction to the asset markets.”

Perhaps the predictions by economists are a (tiny) part of the information flow that the asset markets productively use – in which case economists not trying may lead to (slightly) less efficient asset markets.

Craig

Mar 25 2024 at 11:18am

“Perhaps the predictions by economists are a (tiny) part of the information flow that the asset markets productively use”

How many economists work for the Fed? Hundreds? And the Fed makes decisiojs based on what those economists are seeing, for better or for worse. Markets lurch when JP speaks, the jobs report comes out, the CPI/PPI numbers come out. So I’d say its a major part actually.

Jose Pablo

Mar 26 2024 at 8:34pm

Interesting coment Brent.

It is not clear to me what “asset markets” are, but companies very active in “asset markets” do hire a lot of economist to help them in making predictions.

Scott’s indiscretion regarding their true capabilities might (should?) result in these economists being terminated.

However, to be fair, Scott’s indiscretion will not catch some other companies heavily involved in asset markets off guard:

“If you have one economist on your payroll, you have one too many” (Warren Buffett)

TMC

Mar 25 2024 at 1:17pm

Maybe the ‘Pumped-up’ headline refers to our money supply.

Scott Sumner

Mar 26 2024 at 11:22am

No, it refers to the current economic boom.

billy

Mar 28 2024 at 3:34am

The reason there has been no recession so far is because money supply was increased excessively, not because the Fed successfully avoided an economic overheat through rate hikes. Their rate hikes have merely reduced demand, but the economy remains overheated, evidenced by assets like stocks, bitcoin, and U.S. Treasuries continuing to decline.

Even if the Fed targets 3% inflation, higher inflation is already expected, making further rate hikes essential. Talk of avoiding a recession is misleading, as high interest rates have already depressed consumption, and even higher rates will be necessary going forward to control stubbornly high inflation, implying further consumption weakness ahead.

In summary, the economy is overheated despite rate hikes so far. More aggressive tightening is required to rein in elevated inflation expectations, even though this will inevitably weaken consumption further and increase recession risks. Avoiding a recession was never really an option given how high inflation has become.

Thomas L Hutcheson

Mar 28 2024 at 5:00pm

I see no reason to think the Fed is not trying to get to 2% going forward. We should not WANT then to do backward looking “averaging”

Here was my answer to the question last December:

https://thomaslhutcheson.substack.com/p/why-no-recession

Comments are closed.