When an airliner crashes into the ocean, investigators generally consider the possibility of pilot error. But what about inflation? When inflation is too high, should we consider the possibility that the inflation-targeting pilot screwed up?

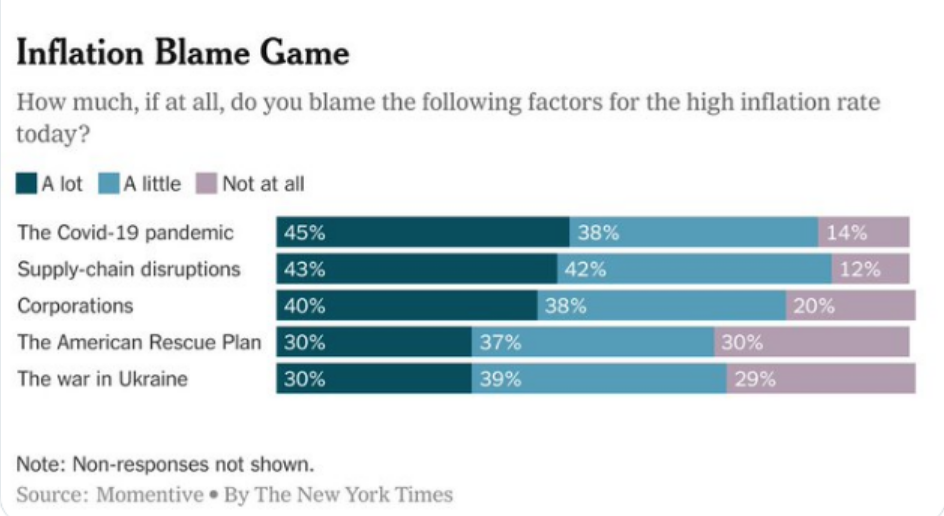

Pat Horan recently pointed out that the NYT omitted the Fed as a possible cause of high inflation in its recent public opinion poll:

We should not write this oversight off as the NYT being a “dumb” newspaper. They are certainly biased to the left, and they often misinterpret economic stories. But the NYT isn’t dumb. At the bottom of this post I have a google screenshot showing many recent stories that indicate the Times does understand that the Fed is responsible for controlling inflation.

Furthermore, if you polled professional economists on the cause of the current high inflation, I am confident that many of them would not name monetary policy. (I suspect that excessive fiscal stimulus and supply shocks would be the most often cited causes.)

During the long slow recovery from the Great Recession, I used the fireman/arsonist analogy to illustrate why policy was so far off course. Both the media and the economics profession tend to view the Fed as a sort of fireman, which comes in to solve economic problems that pop up spontaneously. People don’t generally blame fireman for causing fires. Fed critics like myself view the Fed as more like an arsonist that creates unstable NGDP growth.

Ideally, the Fed would be viewed like an airline pilot, except the goal would be to keep NGDP growing along a steady path. When pilot error does occur, as on Air France flight 447 from Rio to Paris, it’s often in response to some sort of external shock. In that case ice crystals interfered with instrument readings. Nonetheless, the cause of the plane crash was judged to be pilot error. Similarly, Fed inflation targeting mistakes don’t generally happen in a vacuum, rather they tend to occur during periods when the economy is also being disturbed by non-monetary shocks. Nonetheless, if NGDP is too low (as in 2008), or too high (as it is today), then the Fed should be viewed as the cause of the problem.

Perhaps if there were widespread recognition bad inflation outcomes are caused by bad Fed policy, then bad Fed policy would occur less often. Even better, imagine if we could all agree on a simple and unambiguous metric for whether policy is too easy or too tight. What might that policy indictor look like?

How many times must we live through policy errors that could have been avoided if the Fed had focused like a laser on the level of NGDP?

READER COMMENTS

Spencer Bradley Hall

May 25 2022 at 11:17am

In retrospect, it’s remarkable how prescient the high level of N-gDp was.

Michael Rulle

May 25 2022 at 12:48pm

I like the pilot error analogy. To continue with that metaphor, I assume when “ice crystals” interfere with instrument readings it makes it more difficult to get accurate readings, even as they are trained to do so.

As hard as that might be, it must be harder for the Fed to get accurate readings in normal times, let alone when polices by government are changing all the time due (in this case) to a change in those in power, combined with changes in Covid policies, changes in how are our work force “works”, and surprise wars from nuclear powers.

Its like playing tennis against a 4 armed alien. And that assumes our two armed guy is world class. But you have expressed the view that the Fed should have the necessary skills——-let’s hope they do.

Capt. J Parker

May 25 2022 at 1:33pm

OK, so if today we are experiencing a non-monetary supply shock, (coming on the heels of the pandemic recession) what is the appropriate future path of NGDP? Is that path really a continuation of the pre supply shock trend as Beckworth suggests? Shouldn’t there be some short term upward shift in the path of prices because of the shock and shouldn’t this be reflected in the path of NGDP? Wouldn’t forcing NGDP back to the pre-supply-shock trend entail tightening monetary policy during a supply shock – and hence actually be contractionary?

Powell has been quoted as saying that he sees no scenario where future inflation would run lower than 2%. I see this statement as consistent with NGDP returning to an upward shifted trend and not necessarily an indication the Fed has abandoned FAIT.

Kenneth Duda

May 25 2022 at 6:33pm

Hello Capt,

If there is a negative supply shock, the appropriate policy response is *no change to the target level-path of NGDP*. That means there will be a one-time increase in the CPI to bring real wages in line with supply. This way, we can have the unavoidable reduction in consumption (unavoidable under the assumption of a negative supply shock) without recession and unemployment.

The important thing to understand about a negative supply shock is that people will have to consume less, as a simple consequence of the fact that (by assumption) we are producing less. From there, we have choices as to how that happens — what causes people to consume less. The choices are: (1) cut everyone’s salary by 10%; (2) inflate away 10% of the value of everyone’s salary; (3) lay off a random 10% of people. #1 is impossible because of nominal rigidity; employees consider wage reductions as constructive termination. #3 is terrible; in addition to being horribly unfair, it also can reduce production further as the 10% who are laid off stop producing, and also reduce consumption further as the 90% with jobs cut their spending fearing they’re next, and the whole economy melts down into a classic Keynesian depression. That pretty much leaves us with #2.

-Ken

Jose Pablo

May 26 2022 at 9:26am

So, by this reasoning after a supply shock that reduces RGDP, inflation IS the “right” solution, since it is required to keep NGDP trend providing the best way of adjusting to the fact that we are producing less stuff.

So we are “almost” fine now with NGDP growing at around 5% since 2019 4T. After all it would be too harsh to blame the FED for overshooting a little bit after the “brutal” “ice crystal interference” of Covid19 supply shock.

https://fred.stlouisfed.org/series/GDP

So, the NYT question should have been, who is responsible for us having “about the right” inflation problem after the very significant supply (and fiscal) shocks that we have experienced in the last couple of years?

I bet nobody would guess that one correctly.

Kenneth Duda

May 26 2022 at 12:53pm

Yes! And the answer is, “The Fed”. And to answer “I bet nobody would guess that one correctly.” — yes again! The answer to that one is a prediction market — a market where individuals or institutions can make money by correctly forecasting what level of NGDP we will get based on current monetary policy. The Fed can then adjust the money supply until the prediction market is predicting on-target inflation, effectively pegging the value of futures in that market. It’s one of the best ideas ever. I wish I had thought of it. But even more, I wish someone would implement it.

Kenneth Duda

May 26 2022 at 12:54pm

Of course, I meant “until the prediction market is predicting on-target level of NGDP.”

Scott Sumner

May 26 2022 at 3:30pm

“So we are “almost” fine now with NGDP growing at around 5% since 2019 4T.”

Actually, NGDP is about 3.5% above trend, and getting worse. That’s bad. But if you are arguing that the Fed’s mistake this time is much less serious than in 2008-09, then I agree.

Jose Pablo

May 26 2022 at 5:45pm

Can better than “3.5% above trend” be asked of the FED after the shocks we have experienced in the last couple of years?

It seems pretty good to me, taking into account that we are not talking about “physics”.

“and getting worse”

yes, but the FED is doing a lot to address this part. Using the instruments they have aggressively to cool the NGDP growth by reducing inflation.

Looks like good steering to me, taking into account the “steering tools” at the FEDs disposal.

Scott Sumner

May 26 2022 at 8:18pm

They can do far better, and would have if they’d adhered to the FAIT policy.

Jose Pablo

May 26 2022 at 9:40am

And #2 only works if salaries (and pensions) don’t grow with inflation.

In real life, they have a certain degree of “real stickines”. People assume their salaries will keep up with inflation allowing them to consume the same amount of goods and services … but there are less of those good and services around, so we are kind of back to square one

Kenneth Duda

May 26 2022 at 12:49pm

Yes, if there is a negative supply shock, i.e., there’s less stuff to consume, and we raise incomes to prevent inflation from reducing people’s real purchasing power, then there are no degrees of freedom left in the system. You either run out of stuff (you have income, but there’s nothing to buy), or hyperinflation / death of the currency (people stop accepting money as payment for stuff at all).

Note that this scenario is incompatible with NGDP level targeting because in a hyperinflation scenario, NGDP is going to infinity. With NGDP targeting, prices increase only as needed so new_higher_prices * less_stuff hits the target. Prices can’t increase further because if they try, an NGDP-level-targeting central bank cuts back the money supply, and people run out of money to buy the stuff, and prices are limited to a level compatible with hitting the NGDP level target.

NGDP level targeting is one of the best ideas ever. I don’t know what it takes to get it implemented, but boy, do we need it.

Jose Pablo

May 26 2022 at 6:03pm

“Note that this scenario is incompatible with NGDP level targeting”

no, this scenario unfolds precisely because of NGDP targeting.

1.- If there is a real supply shock, the FED (under NGDP targeting) should increase inflation to keep NGDP growing at trend

2.- But an increase in inflation will be followed by an increase in pension and salaries since people want to keep their purchase power intact. This is human nature, out of the FED control and, maybe, even sponsored by other branches of the government and by the unions.

[This #2 could also happen with the wrong fiscal policy aimed at correcting the very same supply shock and coming into place with the very usual delay of fiscal responses]

3.- If 2 results in an increase in inflation, the FEDs aim should be to reduce NGDP which could, very easily result, instead, in a reduction in RGDP

4.- The whole thing can spiral out of control, even if the FED is targeting NGDP with the (blunt?) instruments they have

Actually, the FED seems well aware of the problem with #3 when addressing a supply shock problem:

“The appropriate policy response to a supply shortfall is not so clear-cut. Efforts to stabilize real activity will add to already-elevated inflation pressures, while efforts to stabilize inflation will further depress activity. The FOMC has promised to weigh “inflation pressures” against “employment shortfalls” in such a scenario, but it has offered no explicit guidance on how it will weigh them.”

https://www.dallasfed.org/research/economics/2022/0113#:~:text=Nominal%20GDP%20After%20COVID%2D19&text=Private%20analysts%20were%2C%20in%20fact,percent%2C%20and%20prices%20were%20unchanged

Jose Pablo

May 26 2022 at 6:13pm

Another conclusion will be that attention should be paid to mechanism 2, which is out of the FED’s control.

But:

a) the present labor market does not seem the best one to prevent salaries from increasing and

b) there are significant plans for fiscal expansion and 2022 is a critical election year (every other year is actually election year).

Capt. J Parker

May 27 2022 at 6:44pm

Ken,

Thanks for the reply. Totally agree that the supply shock will result in an increase of the price level. Is this increase in the price level permanent? I argue that at least some of the increase in the price level is permanent because even if the supply shock is temporary, we never make up for the lost production that occurs during the shock. If you have a permanent increase in the price level then, absent a period of contractionary monetary policy, you have a permanent increase in the level of Nominal GDP.

Scott Sumner

May 25 2022 at 11:40pm

I agree with Ken’s response. Regarding this:

“Wouldn’t forcing NGDP back to the pre-supply-shock trend . . . ”

I would not assume that the supply shock moves NGDP off trend. It might, but that’s not at all clear. It moves prices off the trend line, but not necessarily NGDP.

Iskander

May 25 2022 at 4:33pm

A quick glance at the NYT articles at the end of the post seems to put that newspaper firmly into the fireman camp which fits with their choice of not including monetary policy in the poll options.

Fred

May 25 2022 at 8:27pm

How would you compare today to the 1970s? I was completing my education then, and I remember a decade of ineffectual gestures (WIN buttons, etc.) that eventuated in the Volcker led strong medicine that worked. I remember a huge run-up in gold, eighteen percent Treasury strips that I didn’t have the means to buy, and a eleven percent mortgage. I was trying to start a business, and we had about three lean years. These are personal recollections not scholarly analysis.

BTW, the current situation is some in-flight turbulence, not a crash from my standpoint.

Scott Sumner

May 25 2022 at 11:37pm

Yes, the 1970s were far worse (so far.)

Thomas Lee Hutcheson

May 25 2022 at 9:46pm

How could the Fed focus “like a laser” on NGDP without an NGDP futures market to provide day to day feedback?

My image of what the Fed is trying to do is more like a hunter firing at where the thinks the duck is going to be a few seconds from the time they pull the trigger. Missing the inflation target is still “pilot error,” but that does not mean they were aiming at a cloud. The ducks have been flying more erratically recently.

Spencer Bradley Hall

May 26 2022 at 10:58am

R * and U * are fictitious. Monetarism has never been tried. The FED’s accountants’ error when they claim that reserves are drained, but not the money stock, during RRP operations.

If you know how to count, then you know AD and therefore N-gDp.

Jose Pablo

May 26 2022 at 6:31pm

That’s very interesting Thomas … but a little “circular”, after all, the participants in the NGDP future market will be looking mainly (only?) to FED’s “forward guidance” on NGDP.

Any possible discrepancy between the future market and the FED forecast would mean that the FED had lost credibility on its ability to steer NGDP.

Does not seem to be the most useful information to fine-tuning the NGDP steering (although very likely will open a lucrative private market for ex-FED’s NGDP analysts)

Matthias

May 28 2022 at 4:39am

The Fed can start an NGDP prediction market, if they want one.

Philo

May 26 2022 at 5:52pm

I don’t like the Times’ word ‘blame’, but I would attribute a substantial pro-inflation effect to every one of the choices they offer. Of course, the Fed could offset any such factors, but it is not disposed to do so. Given the Fed as it really is, I think these factors all contributed to its error, and thus to excessive inflation and NGDP.

Jose Pablo

May 26 2022 at 6:21pm

This quote from Friedman:

“All other alleged causes of inflation—trade union intransigence, greedy business corporations, spend-thrift consumers, bad crops, harsh winters, OPEC [Organization of Petroleum Exporting Countries] cartels and so on—are either consequences of inflation, or excuses by Washington, or sources of temporary blips of inflation.”

is from 1977!!

It seems that the NYT keep doing/promoting the same mistakes that Friedman was pointing out in 1977, forcing you to repeat, basically, what he said 45 years ago.

Haven’t we (= the people, the NYT, the politicians …) learnt anything in 45 years?

That would be sad, no?

David S

May 26 2022 at 9:32pm

As an aerospace engineer, I lived by the mantra “there is no such thing as pilot error.”

The reason was, if the pilot made an error, we made him do it. In the Air France example, the flight controls should have had some visual feedback telling the more experienced pilot that the inexperienced pilot had his controls full back. We can’t make better pilots. We can make planes easier/safer to fly.

As an aspiring economist, is there some analogy for the Fed? Is it possible to add strong enough guard rails so that even a moron could set good policy?

It sounds like NGDP targeting might be such a guard rail. I wonder if it is possible set up a market large enough that it could automatically do the Fed’s job in some way?

robc

May 29 2022 at 4:45pm

Friedman proposed a couple of methods that was basically the Fed on autopilot.

Comments are closed.