Here are five observations about recent trends in monetary policy:

1. The Fed would really like to avoid any further increase in interest rates. This psychological aversion to interest rate increases in not rational, and it actually makes it more likely that the Fed will find it necessary to raise interest rates even further. That’s because this sort of “reversal aversion” is itself a form of forward guidance, which makes monetary policy more clumsy. It increases the risk that disinflation will reverse course, requiring further rate increases.

2. I’ve seen claims that Jay Powell privately prefers Biden to Trump. People often cite the fact that he refused to cut interest rates as often as Trump would have liked, and that he refrained from tightening monetary policy in late 2021 as Biden was considering whether to re-appoint him as Fed chair. I don’t know if these accusations of political favoritism are true (I’m skeptical), but if true it implies that Powell ended up greatly helping Trump and hurting Biden, even while appearing to be trying to do the opposite.

The message here is clear. People worry a great deal about political bias. But when it comes to monetary policy, policy mistakes are a far greater problem than policy bias.

3. Mohamed A. El-Erian has a new essay in Bloomberg:

Rather than maintain a policy reaction function anchored by excessive dependence on backward-looking data, the Fed would be well advised to take this opportunity to undertake a belated pivot to a more strategic view of secular prospects. Such a pivot would recognize that the optimal medium-term inflation level for the US is closer to 3% and, as such, give policymakers the flexibility to not overreact to the latest inflation prints.

As I detailed in a column last month, this path would not involve an explicit and immediate change in the inflation target given the extent to which the Fed has overshot it in the last three years. Instead, it would be a slow progression. Specifically, the Fed “would first push out expectations on the timing of the journey to 2% and then, well down the road, transition to an inflation target based on a range, say 2-3%.” . . .

While not without risks, such a policy approach would result in a better overall outcome for the economy and financial stability than one that sees the Fed run an excessively tight monetary policy.

I agree that this would result in a better outcome for the economy over the next few years. But I don’t believe that it’s a good idea. Ideally, the Fed would shift to a 4% NGDP target. But if they insist on sticking with inflation targeting, they should stay at 2%. This is a classic example of the time inconsistency problem. The best policy for the next few years is not always the best long-term strategy. In the long run, there are huge gains from creating a clear rule and sticking with it.

4. Brad Setser expresses some widely held views regarding China’s exchange rate policy:

China needs to look for policies that move it closer toward book internal and external balance – and that (uncomfortably) means limiting the use of classic monetary policy tools.

But it is also reasonable that China made a real effort to use its domestic policy space to support its own recovery—and so far it has not been willing to provide direct support to lower income households, or to consider reforms to its exceptionally regressive tax system. Logan Wright and Daniel Rosen foot stomped these points in a recent article in Foreign Affairs.

Ultimately, of course, China sets its own exchange rate policy; it has a long history of ignoring external advice that goes against its self-perception of its own interests. But there is no reason why China’s trade partners should encourage China to move toward more flexibility right now, when it would only help China export more of its own manufactures to a reluctant world. Pragmatism should rule.

I have exactly the opposite view. China should avoid fiscal stimulus and instead rely on monetary stimulus, even if this results in currency depreciation. I also doubt that this sort of yuan depreciation would result in a larger Chinese trade surplus. Monetary stimulus would likely boost Chinese investment, which tends to lower its current account surplus. It might also boost domestic saving, but probably by a smaller amount. In other words the substitution effect resulting from a weaker yen is likely to be weaker than the income effect resulting from easy money boosting GDP growth.

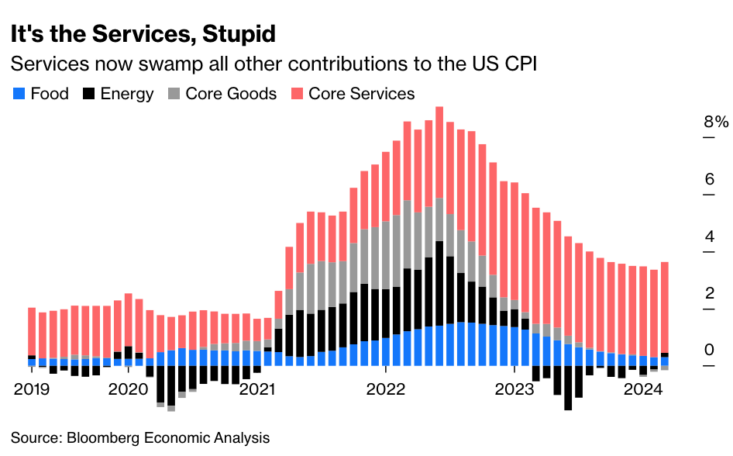

5. John Authers at Bloomberg has an interesting graph showing the contribution of 4 key sectors to the overall (12-month) rate of CPI inflation:

Food, energy and core goods are much more strongly affected by “supply shocks” than are services. But monetary policy does impact even the prices of these goods. Thus you can think of the red area (services) as almost entirely reflecting monetary policy, and fluctuations in the black, blue and grey areas as reflecting a mix of monetary (demand side) and supply side factors.

Service sector inflation stopped improving after October 2023, which is a worrisome trend.

READER COMMENTS

MarkLouis

Apr 15 2024 at 2:10pm

Most don’t realize the Fed has implicitly raised the inflation target twice already. First, via FAIT (correcting only for undershoots means realized inflation will mathematically be >2%). Second, via the apparent VERY long timeframe which they are comfortable letting inflation run hot (whereas significant inflation undershoots are attacked aggressively with bold new emergency programs, etc). A raise to 3% would be yet another increase. Which is why you are correct when you say it’s important to stick to your target – because we all know it’s a slippery slope and we will generate our expectations accordingly.

Thomas L Hutcheson

Apr 17 2024 at 4:58pm

a) “Average” inflation should never have been thought of as a backward looking average. We want an average inflation target that is appropriate for — facilitates the adjustment of relative prices that results from — the average size and frequency of shocks. Of course we want an extraordinarily high (over target) period of inflation to facilitate adjustment to an extraordinary shock like COVID that then returns to the target level. Of what relative prices would engineering a period of below-target inflation facilitate adjustment?

b) Has the writer forgotten a decade of below-target inflation after 2008, when a shock of that magnitude surely merited over-target inflation?

Kevin Erdmann

Apr 15 2024 at 2:52pm

It’s funny that El-Erian says the Fed is backward looking while his own estimation of the current inflation trend must include the CPI shelter component which has known lags and, on year-to-year measures is basically currently reflecting rent inflation from 2022. Inflation has been at 2% for nearly 2 years now using timely market rents for the shelter component.

MarkLouis

Apr 16 2024 at 3:29pm

This is just another way of saying the Fed underestimated past inflation (relative to an index calculated using real-time rents). So yes, inflation might be lower today. But it would have been higher over the past few years and rates would likely be higher than they are now. So perhaps you get a cut or two – to where we currently are today.

Kevin Erdmann

Apr 16 2024 at 3:57pm

Yes. True. The transitory inflation was higher in 2022 than the headline number because of the shelter lag. That inflation ended without rate hikes, but I suppose if the Fed had hiked sooner because of it, inflation would be even lower than 2% today.

Jose Pablo

Apr 15 2024 at 4:49pm

El-Erian seems to be paraphrasing Groucho Marx:

“Those are my principles, and if I don’t have the will/guts to comply with them… well, I have others”

Craig

Apr 15 2024 at 7:59pm

I typically find El-Arian to be a level-headed commentator.

Jose Pablo

Apr 15 2024 at 5:11pm

transition to an inflation target based on a range, say 2-3%.” . . .

Since 2012 the average inflation rate has been 2.63%

The 20-year break-even inflation rate is around 2.5%

So, it seems that both history and long-term forward-looking markets show that the FED is already doing/is believed to be able to keep doing, what El-Erian suggests the FED should do. Not what the FED says it will do.

Thomas L Hutcheson

Apr 17 2024 at 5:01pm

More like 2.3% based on regressions over a number of periods.

Craig

Apr 15 2024 at 7:58pm

“The Fed would really like to avoid any further increase in interest rates. This psychological aversion to interest rate increases in not rational”

Federal interest payments now exceed $1tn annually and how much of that debt is resetting this year? You’ll have to forgive me but I can’t count that high.

How much commercial paper is coming due this year this year set to be reset higher? Perhaps part of Friedman’s long and variable lead times?

All of this on the backdrop of nasty and potentially even nastier global conflicts.

#debttsunami ?

Jose Pablo

Apr 15 2024 at 8:50pm

The 30 yr treasury rate is 4.6%

The 30 yr fixed mortgage rate is 7.8%

Now, imagine a US citizen that can a) pay $100 more in taxes so that the US national debt (for a given level of expenditures) can be reduced by $100

or b) not paying this $100 in taxes and reducing the amount of the mortgage he needs to ask for in, precisely, $100.

In option a) “he” is saving $4.6 per year in interest, in option b) his savings will be $7.8

For our imaginary taxpayer-citizen, more deficit makes total sense.

The problem is whether the level of expenditure makes (or doesn’t make) sense (my guess: it doesn’t). The deficit is mostly irrelevant (or at least, its optimal level is extremely difficult to know. It depends on the summation of individual citizens’ decisions along the lines of the example)

Think of the national deficit as a way of shifting the burden of government expenditures from taxpayers-citizens with an opportunity cost for their money higher than the national debt interest rate to debtholders (citizens or not) with the lower possible opportunity cost of their money.

That’s a sensible thing to do. By all means.

Craig

Apr 16 2024 at 6:09pm

“The deficit is mostly irrelevant”

Well, we’ll see, if you ask me they represent a gross misallocation of monies to things like war, but I digress, the fact is you have been mostly correct for the duration of my lifetime. I do suspect that they are going to start to matter since I suspect that we are in the beginning stages of a sovereign debt crisis. Now that tax season is over reverse repo is trending down again and we have seen longer tails on treasury auctions. I have a suspicion that something is going to happen when reverse repo is drained and the government’s suction pump can’t suck in enough liquidity. If my suspicion is correct we should see a spike in rates to try to dry capital in and I suspect that the Fed might even intervene to buy the bonds. To me that represents the next inflection point.

And FYI I think in terms of probabilities and possibilities not absolute certainties, and the tete a tete on this website relatively good so I don’t mind sharing my thoughts because I suspect you won’t be Nelson from the Simpsons if my thoughts prove incorrect, which, trust me, my wife tells me every day, is frequent enough!

Jose Pablo

Apr 17 2024 at 12:52pm

my wife tells me every day, is frequent enough!

We do share that, Craig!

Regarding government debt, I see a great alternative to it which is less spending (all government spending is a waste).

But for a “given level of expenditures” I don’t see any benefit in financing it with taxes instead of debt. Taxes are, after all, “money in individuals and companies hands” and as such they do have an opportunity cost. And it is higher than the cost of government debt. Otherwise, individuals will devote that money to … government debt!

Raising debt is like “finding the money with the lowest opportunity cost and financing expenditures with it”. Not a bad deal.

All you need to know about the sustainability of the US government debt is embedded in the interest rate. This marvelous way for markets to transmit useful relevant information!

Do you really think you have some information that debt market participants don’t? If yes, use it to make some serious money!

Can debt markets be proved wrong? It wouldn’t be the first time

Can you be proved wrong? I am sure it wouldn’t be the first time either. Both your wife and mine are right from time to time.

But with the information available right now …

Craig

Apr 18 2024 at 9:35am

“Regarding government debt, I see a great alternative to it which is less spending (all government spending is a waste).”

My prediction is one based on predicting the actions of men and in so doing naturally men can choose to do something different, but at the end of the day my prediction is they will debase the denarius.

“All you need to know about the sustainability of the US government debt is embedded in the interest rate.”

I was once a believer in the collective wisdom of the bond market until the inflation. Inflation peaked in June 22 I think that was the month and a year prior to that what was the one year trading for? I view the bond market now simply as ‘dumb money’

“Do you really think you have some information that debt market participants don’t? If yes, use it to make some serious money!”

Well, I did, but always remember that markets can be ‘wrong’ longer than you can be solvent, right? I mean right now you noted a 2.5% inflation expectation on bonds, quick google on 10 year breakeven (FRED stat) at 2.39% so we’re close, but Y/Y is over 3%. And this on the heels of the post-pandemic inflation at 9%. Fed has defended dollar, QT, rates higher, but the fiscal situation is just absolute garbage.

“Can debt markets be proved wrong? It wouldn’t be the first time”

In the long run anybody long on these bonds is going to get hammered. The world’s largest debtor is going to inflate out of it.

“Can you be proved wrong?”

Of course, for my short term hypothesis I’ll be proven wrong if the reverse repo drains and the next issuance goes off without a hitch, ie there’s demand for the bonds at the sought for interest rate, no spike, no tail, nothing like that. If a bond auction fails and they come in with QE? Then I’m correct.

“But with the information available right now …”

Right here, right now, the US government is a turd. They will debase the denarius, the checks MUST go out.

Todd Ramsey

Apr 16 2024 at 9:28am

In support of 2: In Trillion Dollar Triage, Nick Timiraos writes that Powell thought it important to do the opposite of Trump’s public urging to lower interest rates and loosen policy, so there would be no uncertainty about the Fed’s independence.

Scott Sumner

Apr 16 2024 at 10:53am

OK, but he did lower rates three times in 2019, even before Covid. At a time the economy was booming.

vince

Apr 17 2024 at 12:49pm

Why are you ignoring the yield curve inversion and the repo crisis both in 2019?

Scott Sumner

Apr 18 2024 at 1:50am

It wasn’t relevant for what I had to say.

vince

Apr 18 2024 at 6:18pm

Weren’t you saying that Powell lowered rates in deference to Trump during a booming economy–despite other justifications for lower rates such as yield curve inversion?

Thomas L Hutcheson

Apr 18 2024 at 6:32am

TIPS expectations were still below target in 2019. Trump was right about the direction of monetary policy.

spencer

Apr 16 2024 at 5:59pm

re: ‘ At a time the economy was booming. ‘

It was due to slow.

There’s not much new under the sun. It’s the credit school vs. the money school.

In the credit school, large CDs constitute an increase in credit. They are thus, obviously, an increase in the money stock. Large CDs represent shifts from other deposit classifications, that is money is loose. Combine that with the FED counting MMMFs as banks and you get the rise in gold and other commodities.

spencer

Apr 16 2024 at 6:06pm

The FOMC’s proviso “bank credit proxy” used to be included in the FOMC’s directive during the period Sept 66 – Sept 69.

spencer

Apr 16 2024 at 6:10pm

Retail MMMFs are mis-classified as contained in M.

spencer

Apr 16 2024 at 6:20pm

As I said: Post by flow5 on Nov 26, 2019 at 6:45pmThe 1st qtr. R-gDp in 2020 will be negative.

vince

Apr 16 2024 at 7:14pm

Why are you ignoring the yield curve inversion and the repo crisis both in 2019?

Second attempt–Does someone at econlib censor?

spencer

Apr 16 2024 at 7:36pm

Censor? It’s the democratic way.

vince

Apr 17 2024 at 12:49pm

It’s the universal way.

Thomas L Hutcheson

Apr 17 2024 at 6:31am

Any kind of forward guidance (beyond reiterating the Fed’s goal of bringing inflation back to 2% PCE and is willingness to do what it takes to achieve that target) is undesirable.

What IS your interpretation of the delay in tightening monetary policy. [Mine is closer to it wanting to give markets lots of “warning” before doing it, but I agree that it was just and unforced error given that TIPS was showing expectation above target.]

The Fed should definitely abandon (If that is what is had been doing) making policy based on backward looking data. The FIAT should be forward looking. What that forward looking target should be is a separate issue.

I do not recognize what “advice” China is receiving and or ignoring. Making its tax system less regressive (in low deadweight loss ways) is good advice whether in Beijing or Washington. China should definitely avoid making fiscal policy for short-run macroeconomic reasons and rely rather on monetary policy. Whether that would result in greater exports depends in part on fiscal policies in the ROW. The US at least should be moving toward near zero deficits which would limit increased net imports from China.

I am unsympathetic to dividing up the caused of inflation into monetary and other factors. It the Fed, all Fed, all the time. “Other factors” may affect Fed decisions about how move its policy instruments to achieve its target, but the outcome is whatever the Fed (mistakenly or not) makes it.

Andrew_FL

Apr 17 2024 at 12:50pm

Inflation being mostly in services at a new high average level is exactly what I’d expect if inflation were permanently settling in at a new higher rate.

Jeff

Apr 18 2024 at 12:09am

Seems astonishing how much commentary from professional economists over the past few years has argued that optimal policy is simply to lie. Maybe telling people that all moral concepts and complex political questions can be boiled down to simplistic technocratic maximization exercises was not such a great idea.

Thomas L Hutcheson

Apr 18 2024 at 8:04pm

Who exactly said that?

Are you sure it’s not true?