I recently rode a commuter train through San Mateo County, California, which is just south of San Francisco. San Mateo is one of the most expensive places to live in all of America, and the view from the train made it easy to see why.

Zoning restrictions in the Bay Area are almost unbelievably counterproductive. Looking outside the train window, you see lots of valuable land right next to the major commuter rail line that is used for unproductive purposes. While there are a few newer apartment buildings, mostly you see lots of ugly low rise buildings, including run down ranch houses, one story warehouses, strip malls, etc. It’s a bleak sight, and a tremendous waste of valuable real estate.

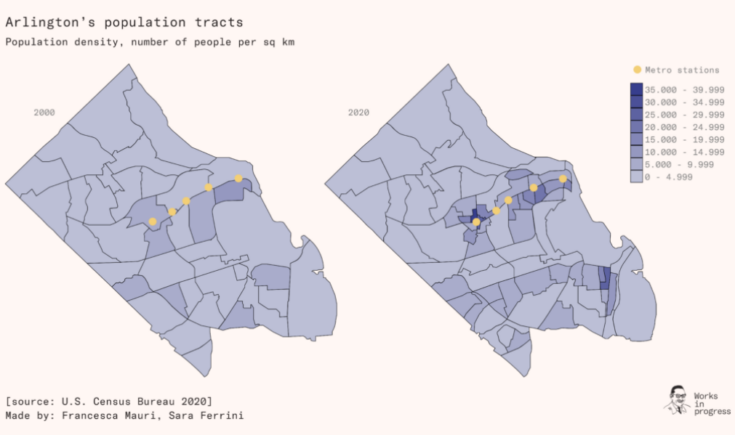

While riding in the train, I thought about the Orange Line subway through Arlington, Virginia, which is the county just south of Washington DC. It’s a nice comparison, because each country is a beacon for high paid professionals working in some of our most dynamic labor markets.

But there’s a big difference between San Mateo and Arlington counties. While the latter does contain lots of low-rise residential neighborhoods, it also allows dense high-rise development within walking distance of the subway line. According to a study by Emily Hamilton, this has led to a surge in apartment construction:

Development along the Rosslyn-Ballston Corridor is visible (most strikingly where I live, in Ballston) as is development along the other transit corridors. In the 1970 Census, ahead of the Orange Line’s inauguration, the county’s housing stock included about 30,000 detached single-family houses, a number that has remained steady in the decades since. But the stock of other types of housing has more than doubled from about 41,000 units to nearly 88,000 units. This infill apartment construction has allowed the county’s population to increase by 60,000 residents in this 50-year period – without expanding the area developed at all.

This contributes to the DC area being substantially cheaper than metro areas with lots of professional jobs but tighter building restrictions. Not surprisingly, they are showing greater population growth:

Four US metropolitan areas in particular – Los Angeles, San Francisco, New York, and Boston – have become increasingly expensive, thereby pushing out low- and middle-income families as higher-income in-migrants outbid them for a stagnant supply of housing. Two other ‘superstar regions’ with high productivity and high average incomes – DC and Seattle – are doing a better job of accommodating new demand for housing with new housing construction. Relative to the other four superstar cities, they are losing domestic residents at much lower rates. DC, Seattle, and some other growing cities across the country are suffering from their own housing shortages, but not on the same scale as those places with the most severe impediments to housing construction.

In case you think this comparison is unfair because there’s something special about the geography of the Bay Area, or reflects the effects of Silicon Valley, keep in mind that San Diego also has tight building restrictions and extremely high housing prices. It’s a general problem wherever you combine lots of well paid jobs and tight restrictions on building. It impacts all of coastal California, as well as New York and Boston.

And even the DC area is far from perfect, with many more building restrictions than would occur in a truly free market. I cite Washington DC rather than a city like Houston, because DC is more similar to other affluent metro areas in the northeastern US and California.

Nor has all this apartment construction led to deterioration in the schools:

Contrary to some of the received wisdom on high-density residential construction in the U.S, Arlington has a highly-rated school district (one school ranking organization ranks it second in Virginia, behind only the city of Falls Church, Arlington’s neighbor to the west with fewer than 15,000 people)

Scott Alexander recently argued that increased density would push up property prices. While there is undoubtedly a positive correlation between real estate prices and density, the causal implications depend on why density has increased. If density rises because of a booming job market in a specific location, then housing prices will rise. If density rises because regulatory changes allow for more apartment construction, then prices will usually decline, or at least rise more slowly than otherwise. Here’s Hamilton:

Between 2012 and 2018, rents in DC actually rose slower than inflation. Virginia Beach, VA, was the only other large metropolitan area in the country for which this was true.

The Hamilton study is full of interesting information, and is well worth reading. Here’s another example discussing northern Virginia’s Fairfax County:

Many of Fairfax County’s peers in California, Massachusetts, and New York are permitting virtually no apartment construction. For example, between 2000 and 2020, the stock of apartments in Marin County, just north of San Francisco, didn’t increase at all. Long Island didn’t do much better, with its supply of housing other than detached single-family housing increasing by about seven percent in those two decades. By contrast, Fairfax County’s increased by about one-quarter.

If you don’t build it, they won’t come.

PS. Hamilton provides a map showing how the recent rise in density is concentrated along the Orange Line subway (yellow dots):

READER COMMENTS

David Henderson

Jul 2 2023 at 6:08pm

Really nicely done.

Sammie M

Jul 2 2023 at 10:06pm

Arlington VA does not have the water shortages that California has. The main reason Californians have resisted adding more housing is that there is barely enough water for the 40 million people who already live in California.

Adding more housing will only make this shortage worse.

Matthias

Jul 3 2023 at 9:50am

California wastes the waste majority of its useable water on agriculture. Domestic use is a drop in the bucket by comparison.

Sammie M

Jul 3 2023 at 11:25am

Yes, most of California’s water goes to agriculture. Perhaps there should not be so much water-intensive agriculture in a state that does not have the water to support it. Farmers argue that growing food is not wasting water. I believe a solution to the current water availability issues -whether it be to build desalination plants, implement toilet to tap recycling, re-allocate the Colorado River, or whatever – should be implemented prior to building more housing. If more water isn’t made available for household use, then there should not be any more housing added in California. Requiring residents to stop using water (which seems to be the current plan) is really not feasible.

Scott Sumner

Jul 3 2023 at 11:48am

This claim is false. California has plenty of water, and the so-called “water shortage” is not at all a factor the in reluctance to allow more housing construction.

Sammie M

Jul 3 2023 at 12:30pm

Well sir, if there is no water shortage but yet government officials are mailing letters to residents threatening fines and imprisonment if you don’t reduce your water use by 50%, and patrolling neighborhoods at all hours of the day and night to see if anyone is breaking the rules by watering their garden, washing their cars, or allowing their children to play on a slip and slide, then we have an even bigger problem than water! If there is no water shortage, why are water districts rationing water to residents, golf courses closing, and wells throughout California running dry?

BS

Jul 3 2023 at 7:51pm

I never accept a claim of “water shortage” without some proof that it’s not really just a “storage shortage”.

Bob

Jul 2 2023 at 10:20pm

Absolutely: And density changes drastically as you change the regulatory environment. Tax the improvements and not the land, and you end up with cities full of surface parking lots, as it’s the cheapest way for a speculator to own the actually valuable thing: well placed land. In the real world, basically every building should be a depreciating asset, just like a mobile home. It just happens that we bundle it together with very valuable land, so it looks like the price went up overall.

We often see underdevelopment and huge price increases in places where there is no practical cost in owning underdeveloped land: Canada and the UK have even worse regulatory regimes than the US for this, so you see single family homes valued at 20 million pounds in basically downtown London. The land is not going to get cheaper, so why redevelop?

Land value taxes are utility maximizing, as the value of land is what is near it, so underdeveloped property is lowering welfare for everyone around. The tax that is excessive for a single family home with a giant lawn becomes quite low when you put 6 apartments in the space, and a business in the ground floor. It might be the only good tax on wealth, as it punishes waste.

There are many ways in which America is the best country in the world, but on urbanism? It’s amazing how we manage to waste so much space, for so little, if any, quality of life improvements. We drive everywhere, therefore we talk to nobody at all, and grow fat due to so many hours sitting while driving. It’ll be seen as bad an idea as leaded gasoline.

Thomas L Hutcheson

Jul 2 2023 at 10:35pm

“The land is not going to get cheaper, so why redevelop?”

Because the developed property if permitted, will ear more revenue. The “why”: is opportunity cost

Matthias

Jul 3 2023 at 9:53am

Yes, opportunity costs are the bane of many Internet-Georgists.

Land value taxes are still a good thing, though. Or in other words, they are still amongst the least bad taxes.

Jeff

Jul 3 2023 at 12:36pm

Perhaps, but the subject of this post (California) will reassess you if you redevelop. So you lose the benefit of years/decades of accumulated inflation differentials.

Brandon Berg

Jul 3 2023 at 12:02am

“While there is undoubtedly a positive correlation between real estate prices and density, the causal implications depend on why density has increased.”

In other words, never reason from a density change.

Jeff

Jul 3 2023 at 3:42pm

I think private ownership of land actually has a bleaker future in California than meticulous controls on development. Unlike Manhattan, California has no aspirationally-libertarian founding myth whereby the land was supposedly purchased from indigenous for a few baubles. It has always been well known that landholdings originating in the Spanish conquest of the New World were acquired via bloody coercion, often several times over. It’s more a historical quirk that the states of California and Hawaii, having what are possibly the two most problematic title histories out of all the states, also have the most property-friendly laws—the 19th and 20th century Anglos who wrote them understood at a deep level that they were trafficking in stolen property and figured they may as well play for keeps. But those people are long gone, and their legacy curiously seems to have set the table for those locations to be the first to transition to full state ownership of land.

Comments are closed.