People on the left like Paul Krugman sometimes suggest that 1934-80 was a sort of golden age of stable banking—after the New Deal regulatory reforms and before the deregulation of the 1980s. I’m not convinced that regulation has much to do with this period of stability, for two reasons:

1. Banking was already getting unstable towards the end of this period, as the cost of small deposits rose above the interest rates that banks and S&Ls earned on their 30-year mortgages.

2. Unexpected price level increases during 1933-80 helped borrowers and reduced debt defaults.

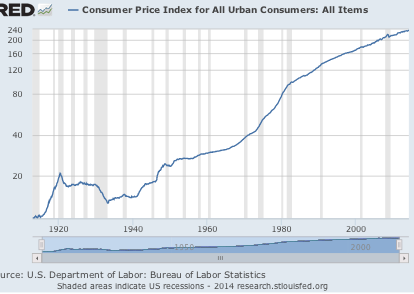

The US devalued the dollar from $20.67/oz to $35 an ounce between 1933 and 1934. This led to a large one-time increase in the price level, which was spread out over many years. In addition, changes in the monetary system reduced the demand for gold, which further increased prices. (For instance, it became illegal for Americans to hoard gold.) The net effect was a large, one-time increase in the price level between 1933 and 1968.

After 1968 the price of gold started rising in global markets, which meant that we were essentially on a pure fiat money regime. Inflation rose even higher during the 1968-81 period than during the previous 35 years. Much of this inflation was unexpected. Borrowers often had long-term loans that did not reflect the ex post rate of change in prices, and hence borrowers did very well. Mortgage loan defaults were not very common.

After 1980-81, both inflation and NGDP growth slowed sharply and unexpectedly. Now borrowers were hurt, as the interest rates they agreed to in the late 1970s and early 1980s were far higher than the rate of inflation after 1982.

[Note that the mild deflation of 1949 didn’t do much harm because back in those days deflation was expected after the end of major wars.]

Even though borrowers did well during the post war decades, banks were under increasing stress in the 1970s. In the 1950s and 1960s they had lent money long-term at fairly low rates, and then when inflation rose in the 1970s they had to pay much higher rates to attract short-term deposits. I’ve seen estimates that much of the banking system was technically bankrupt around 1980, if all the assets were marked to market. Policymakers saw this problem, and decided to deregulate to so that banks and S&Ls could have a more diversified balance sheet. This may have backfired as “zombie thrifts” that were protected by FDIC and FSLIC engaged in a sort of “double or nothing” strategy. Since they were already in dire straits, why not gamble with taxpayer funds? They had little to lose and a lot to gain. (And yes, FDIC funds most definitely are taxpayers’ money, even if these organizations are not formally bailed out. Their resources come from a tax on banks. And FSLIC was bailed out.)

The tight money policy adopted in 1981 led to much lower inflation and interest rates over time, which fixed the maturity mismatch problem. But it also led to many more loan defaults. If the Fed had adopted a tight money policy in the 1970s, it is very likely that we would have had a severe banking crisis then, even though “deregulation” had not yet occurred. Most of the bad behavior that got banks into trouble (subprime loans, mortgage-backed debt, etc.) has always been legal. That’s not to say that regulatory changes after 1980 did no harm, for instance many of the changes actually encouraged sub-prime lending. But banking crises can occur in even highly regulated banking systems, as long as inflation and NGDP growth falls sharply and unexpectedly.

READER COMMENTS

Zachary Bartsch

Jun 17 2014 at 1:17pm

George Selgin makes similar arguments in his book “Less than Zero”. He painstakingly describes the beneficiaries and victims of nominal GDP stabilization and a ‘productivity norm’. I remember that you posted comments about it. This post is very similar. Thanks! Heterogeneity in the effects of AD growth, by a monetarist, is usually enjoyable.

Patrick R. Sullivan

Jun 17 2014 at 2:27pm

The worst thing that banking regulation of 1933-80 did was to lock in the primitive, populist, system of ‘unit banking’ favored by politicians from rural states. Courtesy of Calomiris and Haber’s Fragile By Design;

In 1930 only 8 states allowed unlimited in-state bank branching. With over 9,000 bank failures between then and 1933, more and more states began to allow such branching, by repealing their laws prohibiting it. The Banking Reform Act of 1933 (aka Glass-Steagall) put a stop to that desirable result. So, by the 1970s only 12 states allowed within state branching and none allowed interstate banking.

That result was undermined by the inflation of the 1970s, demographics, and improved information technology. When computers could sweep funds from non-interest paying checking accounts, overnight, into Cash Management Accounts and NOW accounts, it was over for the unit banking coalitions.

Unfortunately, the coalition that replaced it was one between mega-banks and political activists (one of whom was Barack Obama). That new coalition gave us both reduced lending standards for home loans and too-big-to-fail banks dominating the USA (unlike Canada, which defeated its populist, unit-banking enthusiasts in the 19th century).

Scott Sumner

Jun 17 2014 at 7:30pm

Thanks Zachary.

Patrick, Good points.

Roger McKinney

Jun 17 2014 at 7:50pm

Good post! If one knows little about banking then it’s easy to make simple generalizations that support one’s ideology. This post shows that more information can cause reasonable people to come to different conclusions.

I would add that there was no deregulation of banking in 1980. The state quit setting interest rates and eventually got rid of Glass-Steagall, but that’s about all. Then we added thousands of new regulations, including the Basel accords. Banking is one of the most heavily regulated industries in the US.

The Bank of England has a great paper, “Financial Stability Paper No. 13 – December 2011 Reform of the International Monetary and Financial System” that proves Krugman wrong: “Net capital flows tended to be large under the Gold Standard (Chart 1). However, passive domestic monetary policy

responses meant that they were not accompanied by large cross-country policy inconsistencies and so did not pose the same threat to global financial stability as those of today. Table A below, which presents a range of summary statistics on the performance of different IMFS regimes, shows for

example that the incidence rate of banking and currency crises in the Gold Standard was much lower than in today’s system.”

Ari Tai

Jun 17 2014 at 11:53pm

A number of folks have commented on the stability of Canada and Australia’s banking systems though the GFC. Both nations don’t have “jingle mail” (unlike the U.S. and Britain) where we allow a homeowner to mail in the keys to the bank when the home loan is underwater (a total transfer risk to the bank).

Both of those countries bankruptcy systems have no tolerance for speculators leaving a bank with the bill (for reference see the case of Alan Bond, who won the America’s cup). Their judges will strip a speculator of all but the most essential assets – including selling all but the essential work-tools, furniture, transportation, non-essential assets, removing children from private schools, and stopping other deemed frivolous spending (including private health insurance). And when the assets aren’t sufficient, there’s jail time.

And Canada still has a 1800s style unelected House of Lords that has resisted all modernization (even when their banks were losing business to U.S. banks) of their nation’s banking system.

Scott Sumner

Jun 19 2014 at 6:43pm

Roger and Ari, Both very good comments.

Kelli

Jun 21 2014 at 12:27pm

I note references to Krugman in the post and comments. The trouble is that, while I read Krugman regularly, I cannot recall a time when he said that the financial crisis was caused by banking deregulation in the 80s. Instead, he says it was caused by unregulated shadow banking and the seizure of the repo market (a bank run on shadow banks). E.g., here: http://www.nytimes.com/2010/04/02/opinion/02krugman.html

The post is careful to say, “liberals like Krugman,” thus implying Krugman without having to show Krugman actually says that. There is no link.

I could take the thoughts of an uninformed Tea Partier and say, “Conservatives like Summer think that the government should keep its hands off of Medicare.” I don’t think you would be thrilled.

If you really do mean Krugman, rather than “random liberals,” would you please supply some links?

Comments are closed.