Here’s Matt Yglesias on fiscal stimulus:

What the country needs is a stimulative process that has the bureaucratic properties of monetary policy, but the heft and comprehensibility of fiscal stimulus. If we had a national sales tax like Japan does, letting the Fed set the rate up and down to boost the economy would work. One alternative would be to enact temporary cuts in the payroll tax, and have the Fed fill the resulting gap in the Social Security trust fund with printed money. Another alternative would be to print money and mail it directly to American households. But barring broad Federal Reserve reform, Congress could act on its own. Back in 2008, Nancy Pelosi and George W. Bush teamed up to enact a cash in the mail stimulus program and it was highly effective. And in the winter of 2010, Barack Obama and congressional Republicans agreed on a payroll tax holiday that also boosted the economy.

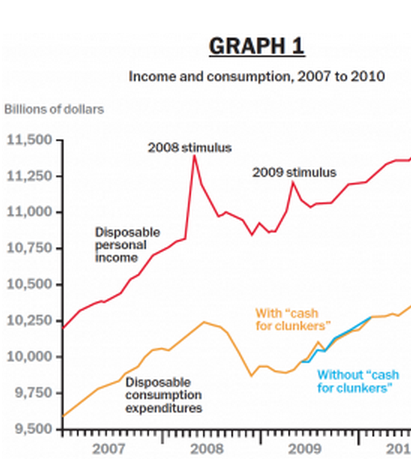

I’m very dubious of all this. When the payroll tax cut was rescinded at the beginning of 2013, Keynesians predicted that growth would slow—especially since lots of other austerity measures were imposed at the same time. In fact, economic growth (2012:Q4 to 2013:Q4 nearly doubled over the previous 12 months. That was due to monetary offset. The Bush tax cuts were also ineffective, for two reasons. One is the normal “permanent income theory” argument, people mostly save temporary tax changes. Here’s a graph from an article by John Cogan and John Taylor:

Notice that the tax rebates of the spring of 2008 boosted disposable income sharply (but only briefly). Consumption rose only modestly, suggesting that most of the tax cuts were saved. Nonetheless, I’d guess that some borrowing-constrained households spent more, so let’s assume that the faster NGDP growth in 2008:Q2 was due to the rebates:

Annualized NGDP growth:

2008:Q1 – 0.5%

2008:Q2 +3.9%

2008:Q3 +0.8%

2008:Q4 -8.0%

Remember, these are nominal figures, the real numbers for the first three quarters are much worse. My claim is that even if the strong Q2 number is due to the tax rebates, it merely stole growth from later in the year.

Let’s consider the Fed minutes from 2008. They show worry about the high inflation rates of mid-2008 (largely due to oil), and also some complacency that the Fed’s aggressive moves in early 2008 had worked. As late as mid-October, the Q2 figures were the last GDP data available. Even as late as the meeting 2 days after Lehman failed (September 16), the Fed saw risks of inflation and recession as being roughly balanced. Thus they did not cut interest rates (from 2%) at that meeting. Indeed there were no rate cuts at all between the beginning of May and early October. That’s pretty shocking given the severity of the 2008 recession. In retrospect, the Fed was clearly offsetting the growth in spending in Q2, which was produced (perhaps) by tax rebates. It’s a nearly perfect example of monetary offset.

Indeed even an economist as Keynesian as Paul Krugman concedes the Fed steers the economy in normal times, and that fiscal stimulus is only justified when at the zero bound. So my argument here is just as much new Keynesian as market monetarist.

However Yglesias does raise one good point, which calls into question my earlier grudging support for the Japanese national sales tax increases (3% this year, another 2% planned for next year.) Matt says that stocks rose sharply on the news the second increase might be delayed. I’m not sure if that’s why stocks rose, but let’s say it is (did they rise right after Abe’s comment?) In that case, I may be wrong about the sales tax increase. Perhaps it has more of a negative effect on AD than I assumed. Or maybe stocks rose because investors like low tax/smaller government policies (an argument one of my supply-sider commenters tried to sell me on.) It might have also been a subtle signal of more monetary stimulus. That later claim may seem far-fetched, but is testable in principle. Fiscal growth measures strengthen a currency while monetary stimulus weakens it. How did the yen move on the Abe statement?

READER COMMENTS

Andrew_FL

Oct 22 2014 at 9:07am

You were doing good until you called them the “Bush tax cuts” which is going to call to mind the rate cuts of 2003 and not the rebates of 2008 (or 2001 for that matter, which didn’t work either).

Ah well, I would hope nobody reading this could possibly get confused by that.

On the permanent income hypothesis, I have a simpler explanation: you can lead a horse to water, but you can’t make it drink.

John Becker

Oct 22 2014 at 9:28am

I’m surprised to see the argument that people saving money from tax cuts doesn’t boost the economy on Econlog. Isn’t that the Keynesian paradox of thrift? Do we really have to debate the view on here that the economy boils down to aggregate spending with no role for savings? When I want to read that stuff I go to Paul Krugman.

Scott Sumner

Oct 22 2014 at 9:51am

John, I was criticizing that argument. I certainly don’t believe in the paradox of thrift.

Kevin Erdmann

Oct 22 2014 at 1:51pm

On the savings issue, if much of the savings involved deleveraging in an economic context where credit markets were not expanding, could it have a paradox of thrift appearance? In a healthy economy saving might mean buying stocks, but in a contracting economy, it seems like that kind of stimulus, even if matched by monetary accommodation, could be pulling cash out of industrial investments into treasuries to fund cash payments that go into deleveraging of consumer and real estate debt. In that case, couldn’t it exacerbate the temporal problems already in place? With the added problem of future taxation distortions.

Scott Sumner

Oct 22 2014 at 9:57pm

Kevin, Definitely agree with the final line. Regarding industrial crowding out, I’m not certain–you might be right. You might want to develop the argument more fully, however, as your comment is rather short and a bit hard to evaluate.

Maryanne, I think you failed the Turing test. But if I’m right you won’t care.

Andrew_M_Garland

Oct 22 2014 at 10:59pm

Sumner: “I’m not sure if that’s why stocks rose, but let’s say it is (did they rise right after Abe’s comment?) In that case, I may be wrong about the sales tax increase. Perhaps … How did the yen move on the Abe statement?”

This “(assume not, maybe this, maybe that, what happened?)” statement doesn’t inpire me to confidence in macro economics. Do macro-econ’s know anything? Are any of the theories and suppositions falsifiable?

ThomasH

Oct 23 2014 at 1:44pm

I’d say that “fiscal stimulus” (meaning more than would result from governments borrowing to execute projects whose NPV’s are positive at the ZLB) is justified if the monetary authority acts as if it is constrained in maintaining/restoring NGDP growth to trend. Since neither the Fed nor Congress acted as they “should” have in 2008-14, it’s hard to say which was more in the wrong.

I’m not inclined to be too hard on those (like PK) who seem to assume that the Fed is constrained and argue categorically for more fiscal policy.

Comments are closed.