Patrick Sullivan left me the following comment:

[Read] what Alan Greenspan did in October 1987. He was on an airplane to Dallas on ‘Black Monday’ when the stock market began to plummet. On arrival he made a few phone calls, and early the next day the Fed issued a statement;

https://www.richmondfed.org/publications/research/

region_focus/2006/fall/pdf/federal_reserve.pdf‘The Federal Reserve, consistent with its responsibilities as the nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.’

It followed up that statement with substantial open market purchases over the next days and weeks. I.e. it created more money. And Fed officials began a round of telephone calls to banks, reminding them they were in the business of lending that money.

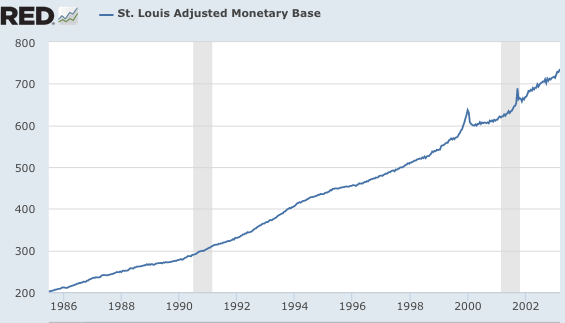

American liberals argue that institutions like the Fed rescue the economy from a deeply unstable capitalist system. Libertarians are skeptical of the activism and worry that it just stores up more trouble for the future. But what if they are both wrong? What if the Fed rescues the economy by doing nothing? Here’s a graph of the monetary base from 1985 to 2003:

If you look closely you’ll see two spikes where the Fed injected liquidity. One occurred at the end of 1999, as the Y2K issue led to fears that ATMs would not work on January 1, 2000. Liquidity was again injected for a very brief period after 9/11. But these are special cases, where even many libertarian economists would recognize the value of some temporary liquidity.

Notice, however, that the Fed didn’t do anything significant in 1987, which saw a stock market crash almost identical to the 1929 crash (both saw a gradual decline of 20% to 25% over 6 weeks, followed by a sharp decline of 20% to 25% over one or two days.) If they did a few open market operations, they were nothing out of the ordinary. The base did not show any unusual moves around the time of the crash (at least using bi-weekly data, perhaps money was injected for a few days and then withdrawn.)

The standard view of 1987 is that Alan Greenspan wanted to avoid the mistakes of 1929. This time the Fed would heroically ease money, and rescue the economy. That’s what the Fed would like us to believe. But where is all this extra money?

How about interest rates? Did the Fed avoid the mistakes of 1929 by slashing interest rates, unlike after 1929? What do you think?

Again, I don’t see anything dramatic in 1987, just a fed funds rate fluctuating between 6% and 7%.

Actually it was the 1929 Fed that heroically cut interest rates, immediately after the stock market crash, and then again and again in 1930:

This doesn’t make any sense. Is the standard view that Greenspan avoided the mistakes of 1929 totally wrong? No, that view is exactly right, but only if you accept my claim that the monetary base and the fed funds rate tell us NOTHING about the stance of monetary policy. In 1987 Greenspan made it clear that the Fed would do whatever it takes to keep AD growth at an adequate level. (He didn’t use those exact words, but that was the essence of his message.) In contrast, in 1929 Fed officials were actually trying to implement a tight money policy, to “pop” the stock market bubble. There were not committed to stable growth in AD, indeed they barely knew what it was.

This is what Nick Rowe calls the “Chuck Norris effect.” Show enough determination and you don’t need to act.

If the base and interest rates are not reliable indicators, then what is? I’d argue for expected NGDP growth. By that metric there was probably almost no change in monetary policy; NGDP kept chugging along at a decent rate for another 3 years, before we experienced a mild recession in 1990-91. And then another decade long boom, and another mild recession.

With sound monetary policy the Fed is not called upon to rescue the economy with wild and crazy actions like massive QE and unconventional asset purchases. And you need not fear imbalances building up, because NGDP growth stays stable. Both the liberals and libertarians are wrong. In 1987 Greenspan did not rescue the economy, nor did he store up future problems by bailing it out with lots of money printing. He did almost nothing other than keep on doing what he was already doing, and it worked. If the Fed had adopted 5% NGDPLT in 2007, there would have been no Great Recession, and yet it would have looked like the Fed did far less than they actually did. Interest rates would not have fallen to zero, and there would have been no QE. (In fairness, we would have suffered mild “stagflation,” slow growth and above 2% inflation.)

PS. In contrast, the 1998 rescue of LTCM was a big mistake, as was Bear Stearns. These actions created moral hazard that came back to bite us when Lehman was able to borrow huge sums from investors that assumed it too was “too big to fail.” Bailouts are not the Fed’s job, stable NGDP growth is.

PPS. Ironically it is those periods where Fed policy fails that it looks the most active by the now-discredited interest rate/monetary base measures. It looks like it’s valiantly trying to boost the economy (or stop inflation with high rates), but just doesn’t have enough “ooomph.” Actually, the aggressive interest rates changes and/or QE reflect the condition of the economy, an economy way off track due to previous Fed policy errors.

READER COMMENTS

E. Harding

May 3 2015 at 12:34pm

Such confidence-building measures as Greenspan’s in 1987 are really important. For example, the most influential U.S. government decision in the 1933 recovery was the blocking of gold exports on April 18, which did little to the base or M1 in itself, but led to an instant stock market and industrial production recovery.

Jon Murphy

May 3 2015 at 12:48pm

I learn so much reading your posts (specifically how little I know about monetary policy 🙂 )

B. B.

May 3 2015 at 2:00pm

Greenspan cut the Fed funds rate several times after the 1987 crash, ending a cycle of tightening. Plus there was a lot of emergency lending.

As for LTCM, it did not get a bailout. It received not one dollar of federal capital nor a Fed loan. It was an expedited Chapter 11.

E. Harding

May 3 2015 at 2:24pm

“Greenspan cut the Fed funds rate several times after the 1987 crash, ending a cycle of tightening.”

-Then what was that three percentage point FEDFUNDS increase in 1988-1989 about?

Scott Sumner

May 3 2015 at 3:31pm

E. Harding, That’s right.

Thanks Jon.

B.B. There were some tiny rates cuts, but compare graph 2 and 3 above. Unlike 1930, the interest rate movements were so small as to look like noise. Ditto for the monetary injections.

Here’s what Wikipedia says about LTCM:

“Seeing no options left, the Federal Reserve Bank of New York organized a bailout of $3.625 billion by the major creditors to avoid a wider collapse in the financial markets.[24] The principal negotiator for LTCM was general counsel James G. Rickards.[25] The contributions from the various institutions were as follows:[26][27]

$300 million: Bankers Trust, Barclays, Chase, Credit Suisse First Boston, Deutsche Bank, Goldman Sachs, Merrill Lynch, J.P.Morgan, Morgan Stanley, Salomon Smith Barney, UBS

$125 million: Société Générale

$100 million: Paribas, Credit Agricole[28]

Bear Stearns and Lehman Brothers[29] declined to participate.

In return, the participating banks got a 90% share in the fund and a promise that a supervisory board would be established. LTCM’s partners received a 10% stake, still worth about $400 million, but this money was completely consumed by their debts. The partners once had $1.9 billion of their own money invested in LTCM, all of which was wiped out.[30]

The fear was that there would be a chain reaction as the company liquidated its securities to cover its debt, leading to a drop in prices, which would force other companies to liquidate their own debt creating a vicious cycle.”

People define “bailout” in different ways, but the Fed facilitated a rescue. It’s not the Fed’s job to prevent “vicious cycles” in the financial world, it’s their job to provide monetary stability. The Fed should not have facilitated a rescue of LTCM.

There’s also debate about whether TARP was a bailout, as the loans to big banks didn’t end up costing the taxpayers a dime. But it still creates moral hazard.

vikingvista

May 3 2015 at 4:30pm

What would have happened if in 1987 Greenspan also *said* nothing unusual–i.e. what if the Fed had acted oblivious to the dramatic stock market changes?

Perhaps no Fed, or no Fed discretion, would be better generally than a reactive Fed.

Andrew

May 3 2015 at 7:46pm

In 3 years I have gone from thinking you were a crazy socialist to looking forward to every post you make. I just want to say thanks Mr Sumner.

Lorenzo from Oz

May 3 2015 at 8:21pm

The job of the central bank is to manage (i.e anchor) expectations. They already acknowledge that about inflation, they just have to take that extra step …

bill

May 3 2015 at 8:52pm

TARP was a bailout.

I’ve always thought of the LTCM rescue as an expedited Chapter 11 too. The primary beneficiaries of the expediting were the creditors of course. The pity is that all creditors should be able to get that type of service, not just the privileged creditors.

Kenneth Duda

May 3 2015 at 11:24pm

Scott, you didn’t mention that if the Fed had implemented sensible monetary policy in 2007, there would have been much less pressure to do bail-outs, as a stable monetary environment could have greatly reduced mortgage defaults, unemployment, auto maker problems, etc.

-Ken

Kenneth Duda

Menlo Park, CA

Rajat

May 4 2015 at 8:22am

Didn’t Bernanke / the Fed do quite a bit of the Bagehot-style liquidity injections at penalty rates of interest in 2008? I don’t know much about these activities but for example, see here: http://www.ny.frb.org/newsevents/speeches/2013/bax130919.html

Eric Rasmusen

May 4 2015 at 1:04pm

Good post!

Scott Sumner

May 4 2015 at 8:51pm

Vikingvista, Hard to say, but I wouldn’t want to take that risk. Better to have transparent policies that avoid uncertainty.

Andrew, I may be crazy, but I’m no socialist! 🙂

Lorenzo, That’s right.

Bill, Or maybe no creditors.

Ken, That’s right, although I don’t want to suggest that good monetary policy would prevent all financial distress.

Rajat, As I recall they did. The focus was on helping banking without easing policy, hence programs like IOR to sterilize the reserves being injected.

Thanks Eric.

Jose Romeu Robazzi

May 9 2015 at 12:47am

@prof. sumner

According to this book http://en.wikipedia.org/wiki/When_Genius_Failed

LTCM had a little below 5 billion in equity, 125 billion in assets, and 1.2 trillion in derivatives notional positions. That is a lot of leverage. Technically, the fund was not able to meet its obligations with the investment banks that were its counterparts in the derivatives transactions. The NY Fed was looking into this, and arranged a meeting between 10-12 banks in order to syndicate a loan to the fund, in order to keep it afloat. If I am not wrong, it looks that the lender of record was the Fed, but the banks themselves provided the funds. Bear Stearns, the main clearing house for the funds trades, refused to participate. Probably the Fed did provide funds to some of the banks involved, or promised to do so. Given contagion fears, this was a financial stability set of measures, eventhough the actual money injected in the system was zero or very little

Comments are closed.