In this post I’m going to ask for your advice. I’d like to know why the public, and even the more sophisticated pundits, have so much trouble understanding monetary offset.

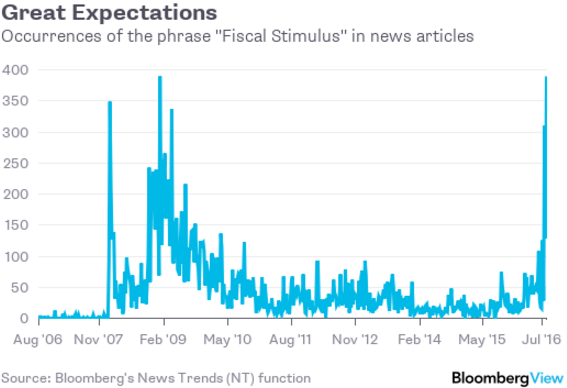

Stephen Kirchner sent me a Bloomberg piece discussing the sudden interest in fiscal stimulus:

Monetary policy has done the heavy lifting to date, boosting asset values in the stock market and driving down borrowing costs in the bond markets to record lows for both companies and governments. But the law of diminishing returns seems to be neutralizing central-bank efforts to do anything more than stop the global economy from cratering; never-ending interest-rate cuts and expanded quantitative easing halted the economic slide, but don’t seem able to generate robust growth.

Hence, there’s increasing chatter about the prospect of fiscal action from governments, which is shorthand for borrowing money to spend on infrastructure projects, thereby creating jobs, boosting growth and investing in the future. The U.S., the U.K., Japan and the euro zone are all being urged to ease up on austerity and open their pocketbooks.

The chatter, though, has become a roar — which raises the uncomfortable prospect that speculation about fiscal action will lead to disappointment. Here’s a chart showing how the hubbub has become louder and louder in recent weeks:

There are so many fallacies here one hardly knows where to begin. The central banks have not done any “heavy lifting”. They can print money at virtually zero cost and their massive portfolio of bonds is generating enormous profits, more than twice as large as before the recession.

Interest rates have fallen to low levels because of slow NGDP growth, not easy money. If policy were actually expansionary, we’d see increasing inflation/NGDP growth.

There are no “diminishing returns” in monetary stimulus, as Joe Gagnon showed in his recent study of QE.

The unemployment rate in the US has fallen back below 5%. That’s all monetary policy is supposed to do, and all it can do. If we have sluggish growth due to productivity, there is nothing that monetary policy can or should do about that. We need supply-side reforms.

Of course the biggest mistake has to do with monetary offset. If fiscal policy becomes more expansionary, central banks will simply offset it. Already there is chatter that the ECB may not ease policy at its next meeting, as had been expected. Why not? Because the post-Brexit economic slump does not (yet) seem to be materializing. When growth is stronger, money becomes tighter. Now it’s very possible that the ECB is making a mistake in not easing—inflation is far below their target—but that has no bearing on whether monetary offset occurs.

Let me head off one possible misconception. It’s not possible to do fiscal stimulus in both good times and bad. There is a long run budget constraint. Years when the national debt is rising as a share of GDP need to be offset by years where the national debt is falling as a share of GDP. If the fiscal policymakers do more stimulus at a time when unemployment is 4.8%, they will not be able to do as much the next time it is 8% or 10%.

I’m also being to see murmurs in the pundit class that Britain might not fall into recession after all. Gee, do you think it’s possible they forgot about monetary offset?

Have people already forgotten that Japan’s earlier experiment in fiscal stimulus, including lots of bridges to nowhere, did absolutely nothing for aggregate demand? In fact, Japan is one of the few fiat money countries to ever experience a two-decade fall in NGDP, from 1993 to 2013. Have people forgotten that growth in the US picked up during the austerity of 2013, when 350 Keynesian economists warned that austerity risked a double dip recession?

Even Paul Krugman used to remind his readers that monetary offset applied when interest rates were being controlled by the central bank. This is not rocket science, so why is it so hard for pundits to understand? I’m genuinely perplexed.

PS. Alex Tabarrok linked to an excellent Scott Alexander post that exposes the progressive tendency to respond to every failure of regulation with a call for more regulation. I see an analogy with fiscal stimulus. Instead of asking central banks to do more (the obvious solution) they propose dubious schemes to try to use fiscal policy to make up for the failures of monetary policy.

PPS. David Henderson’s new post links to another great example. Instead of responding the the 2008 banking crisis by unwinding the regulations that did so much to contribute to the crisis, they left them in place and added many more, each of will have dozens of unexpected side effects.

READER COMMENTS

Effem

Aug 30 2016 at 1:06pm

People believe that money today disproportionately likes to be hoarded as wealth as opposed to spent as consumption. While there may not be a “cost” to monetary stimulus, people fear that there could be either a “painful reset” or asymmetric policy due to political pressure.

If financial wealth expands massively relative to underlying income the unit of return per unit of volatility is depressed, leaving financial assets vulnerable to a sharp return to historical norms of risk/return.

If the desire to consume vs hoard wealth ever increases, policy makers must be willing to potentially accept a period of highly negative financial asset returns with a healthy “real economy.” People fear that this will be politically unacceptable and thus policy will be forced into an asymmetric stance by leaders/voters (can’t withdraw stimulus despite healthy consumption due to falling financial assets).

Right or wrong, it is perceived that fiscal policy helps avoid the expansion of wealth/income ratios thus lowering the risk of the above scenarios thus making fiscal vs monetary stimulus somewhat apples-to-oranges.

Bob Murphy

Aug 30 2016 at 3:08pm

Wow, thanks for linking to that Scott Alexander post, Scott. That was a thing of beauty.

Patrick R. Sullivan

Aug 30 2016 at 3:19pm

Well, this is timely;

Scott Sumner

Aug 30 2016 at 3:53pm

Effem, Interesting theory, but I’m trying to figure out why people don’t get monetary offset. I doubt it’s because they think fiscal stimulus will make asset prices more stable.

Kevin Erdmann

Aug 30 2016 at 4:10pm

I came to say basically what Effem has said better. Asset prices are strongly tethered to forward income expectations, but these are unmeasurable. Monetary policy tends to improve forward income prospects while fiscal policy is supposed to boost current incomes temporarily. So, it is fiscal policy’s weakness that makes it popular because we are basically operating in a low trust atmosphere.

This idea that asset prices are unmoored from rational expectations has become deeply and broadly embedded. In housing, in academic papers debating about whether credit supply was an active cause of the housing boom or a passive result of it, whole papers on both sides are written that never once mention rent or imputed rent. Then, in their conclusions, they are left to debate only what form of irrationality led to the boom. Because on both sides of the debate they excluded rational expectations from their explicit discussions.

The same thing is happening on the broader scale. Rising equity values are a sign, first and foremost, of rising growth in national incomes, but, in the end, this must be taken on faith, because it is based on something that can never be measured or confirmed. The scientific method is pretty boss, but nobody was ever promised that the truth would be falsifiable.

The internet bubble and the housing bubble have undermined faith in asset prices as a measure of future incomes. In the case of the housing bubble, this is kind of crazy, since the correlation between high and rising rents and high home prices at the MSA level is extreme, even though many don’t care to notice. But, it is what it is. Faith in this connection has been undermined, and I don’t know of an easy way to re-establish it.

Here is a post I did a while back on the topic.

Jeff G.

Aug 30 2016 at 4:36pm

One thing you probably noticed is that the article defines fiscal stimulus as investment spending that will boost long-term growth. I would bet that is how your average person thinks of fiscal stimulus. How can “stable monetary policy” compete with the lofty promise of investment in the future?

ThaomasH

Aug 30 2016 at 5:25pm

Actually, no. Monetary policy had not done everything it could. It has failed (for lack of trying, not for lack of ability) to keep the price level rising a its supposed target of 2%.

We need not do fiscal “stimulus” at all. We need to have the public sector invest in activities with positive NPVs. These will expand when borrowing rates are low and market prices of project inputs are above marginal costs during recessions and contract as interest rates rise and real goods markets tighten during recovery. The attempt to do this will of course be denounced as “stimulus” by mecia macro pundits, but so what?

Matthew Moore

Aug 30 2016 at 5:43pm

People think that the Fed ‘controls’ inflation. They think that the government ‘controls’ growth.

This fallacious separability is deeply entrenched. They don’t realise that (I) long run growth is a supply-side issue, not a stimulus issue or that (II) monetary and real factors are not in fact seperable, both being demand-side policies.

That’s it.

Matthew Moore

Aug 30 2016 at 6:10pm

*in the short run

Effem

Aug 30 2016 at 8:33pm

To actually answer your question: 1) most people are simply not good at this type of thinking.

BUT 2) many consider monetary policy to work more on future income (“wealth effect should eventually lead to consumption”) and many types of fiscal stimulus to work more on current income (“put money in the hands of those with high propensities to consume today”).

The simplistic thinking is along the lines of “if we had simply handed average people $1T instead of buying $1T of treasuries” we would certainly have a consumption boom on our hands.

Benjamin Cole

Aug 31 2016 at 12:33am

In this post I’m going to ask for your advice. I’d like to know why the public, and even the more sophisticated pundits, have so much trouble understanding monetary offset.–Mr, Sumner

Not sure, but remember, there is a powerful orthodoxy that fiat money central banks and the Fed are “easy,” and have been “easy” and by being so “easy” for so long have gotten us into the mess we are now. This is gospel, and even recited at Alt-M and Cato etc. let alone the usual right-wing position propaganda mills (the left-wingers are just as bad in other ways).

That the Fed is easy is the premise, despite the fact that inflation and interest rates have been falling since the early 1980s.

So now, having brought about zero-bound, the central banks are out of ammo!

In a sense, the public can hardly be blamed. Shrewd, articulate people everyday say how easy the Fed is.

When the Fed engaged in QE, the Niagara of fear-mongering nearly overwhelmed sensible observation and debate.

Maybe most pundits are just mouthpieces, and there is a politico-economic reason for this enduring hysteria regarding easy money, the savaging of QE, and the absolute refusal to even consider helicopter drops.

And now, as you point out, the building crescendo that central banks are out of ammo! This is like sending the battleship home after it never fired a salvo. “No powder left!”

Most regulatory bodies are subject to industry capture; maybe that has happened at the Fed.

Structural reforms? Every developed nation needs structural reforms. Tyler Cowen, noting the economic doldrums in Singapore, said they need structural reforms, Singapore!

In Nirvana, we will have nations without structural impediments. Until then we have to make monetary policy for where we actually live.

Also, the USA and Japan grew rapidly during decades when they had far worse structures than today.

Send in the Hueys, the Chinooks, and the Sikorksys. Darken the skies.

bill

Aug 31 2016 at 7:22am

I think the primary reason the public does not understand monetary offset is Paul Krugman. He has spent the last eight years calling for fiscal stimulus because we are “at the zero lower bound and everything is different at the ZLB”. It seems his definition of that phrase is “less than 2% or so” – I say that because he would claim that Europe has been at the ZLB for the last 8 years too. The sad fact is that Krugman’s columns and blog posts are the primary source of monetary policy analysis for a large majority of the commentariat.

Rajat

Aug 31 2016 at 8:21am

“Why is it so difficult to understand?”

I proffer two reasons.

First, most people aren’t much good at counterfactual thinking. After all, even 75% of economics PhDs or whatever couldn’t correctly identify opportunity cost in a simple example. It’s like the human brain is wired to analyse the direct consequences of a decision (run or fight) rather than deeply consider the path not taken.

Second, even central bankers like Ben Bernanke have been saying for years that monetary policy is losing its effectiveness so help is needed from fiscal policy. If the custodians of monetary policy say these sorts of things, why should anyone else think differently? They would just prefer to live in a world of (temporarily) higher interest rates even if it means higher deficits. It means they won’t get blamed for bubbles that burst. If due to fiscal policy they can get rates up above what they were in 2007, they’ll feel immune from bubble criticism.

Scott Sumner

Aug 31 2016 at 10:15am

Thanks Bob.

Patrick, Good article.

Kevin, Again, a few people may believe that, but it doesn’t explain why they think fiscal stimulus will boost growth.

Jeff, I call that voodoo Keynesianism.

Effem, Both impact present and future expected income, but I suppose people might believe in that fallacy.

Bill, Yes, he has not been helpful in recent years. His old stuff on monetary offset is excellent.

Rajat, Good point about counterfactuals.

#2 Note that people are still saying this stuff when the Fed is raising interest rates, and hence the “out of ammo” excuse is no longer operative.

pyroseed13

Aug 31 2016 at 10:32am

“I’m also being to see murmurs in the pundit class that Britain might not fall into recession after all. Gee, do you think it’s possible they forgot about monetary offset?”

If Britain does not fall into a recession it will have nothing to do with monetary offset and everything to do with the fact that the profession overstated the risks from Brexit.

Joe Leider

Aug 31 2016 at 12:49pm

I think people are making the mistake that, close to the zero bound, monetary policy can’t do much more. They are also assuming that the Fed will “keep” interest rates near zero while fiscal stimulus happens. While that is undoubtedly true, it is because, with higher gov’t spending, the Fed will start to talk up tightening. The talk will lower expectations of future NGDP growth and keep us near zero. The public doesn’t understand that statements about tightening constitute tightening, even if rates end up the same. They also don’t understand the point you’ve driven home time and time again – never reason from a price change.

James Alexander

Aug 31 2016 at 4:24pm

Pyroseed13

How would you go about providing quantitative backing for that assertion?

I could assert that Carney, despite campaigning for Remain, was clearly very alert to the risks of Brexit and on the front foot monetarily on Friday 24th, as many market participants noted.

FWIW I agree the likely cost of Brexit is overstated and the benefits barely even estimated. The path not taken etc.

James Alexander

Aug 31 2016 at 4:30pm

On monetary offset misunderstanding. You are a party pooper. Fiscal policy is MOAR government and that’s gottta be good vs market failure all the time.

Brett

Aug 31 2016 at 5:08pm

[Comment removed pending confirmation of email address. This is your final notice. We have attempted to contact you several times previously. Email the webmaster@econlib.org to request restoring this comment and your comment privileges. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

Scott Sumner

Aug 31 2016 at 8:40pm

pyeoseed13, There are two issues here. One is the uncertainty created by fear of Brexit, and the other is the direct economic impact of Brexit itself. Monetary policy can probably offset most of the cyclical impact of the uncertainty. The long run drag on growth caused by Brexit itself cannot be offset with monetary policy, but may well be rather small. It’s too soon to say.

Joe, You said:

“I think people are making the mistake that, close to the zero bound, monetary policy can’t do much more.”

It’s not about the Fed doing more, it’s about refraining from doing less. Surely people understand that the Fed can refrain from raising interest rates, don’t they?

Brett, But there was a massive increase in the Japanese national debt, and the worst performance on NGDP ever experienced over a long period of time. How is that not a major embarrassment for Keynesianism?

James Alexander

Sep 1 2016 at 2:19am

On monetary offset misunderstanding. You are a party pooper. Fiscal policy is MOAR government and that’s gottta be good vs market failure all the time.

J Mann

Sep 1 2016 at 2:03pm

Scott, here’s my take on why it’s hard to understand monetary offset.

1) Macro is hard. As an example, I think I’m pretty smart, I have an economics B.A., I’m interested in economics, I’ve been reading your blog for several years, and I’m specifically interested in monetary offset, and I am not confident that I understand it well enough to say for sure if it’s true or not.

I like to imagine that if I spent somewhere between a long afternoon and a long weekend really working on it, I’d get it, but that’s unproven, and anyway, most of the public and pundits aren’t going to spend that kind of time.

2) When you don’t understand complicated issue, expert consensus is a good alternative, so it’s pretty effective with me when you say “Paul Krugman agrees with me.” A survey of 100 economists or a letter from 100 economists would go even farther.

3) I think really understanding it requires a reasonably sophisticated understanding of how fiscal stimulus actually stimulates the economy and how fed targeting would prevent that stimulus. You could try to dumb it down – my dumbed down understanding goes something like:

a) People generally think that fiscal stimulus increases economic growth because people have more money, and they spend it, so producers make more things, and then you have a virtuous circle. (Effectively, increased velocity produces a multiplier).

b) But “people have more money” means the money supply increases. The fed controls the money supply to control inflation. If the fed wants the money supply to be eight trillion kwatloos next month, that’s pretty much what it’s going to be, and if fiscal operations produce another quarter million quatloos, then you can expect the fed to take it out.

3) The other problem is that people want fiscal stimulus for other reasons, so it’s easy to talk themselves into it, no matter what the consensus or evidence. Still, better arguments will convince some people. Compare rent control.

Comments are closed.