There seems to be a consensus that Japan has been stuck in a “liquidity trap” since the 1990s. Here’s a typical story, from the Wall Street Journal:

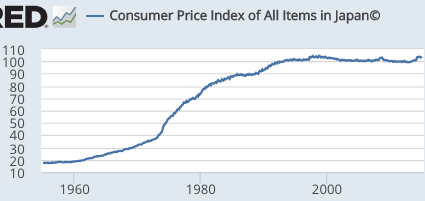

Japan remains definitively stuck, despite a long and aggressive experiment with ultralow rates. A quarter-century after its property bubble burst, a penny-pinching generation has come of age knowing only economic malaise, stagnant wages and deflation–a condition where prices fall instead of rise.

The belief that deflation will continue has become so ingrained it has presented seemingly insurmountable challenges to monetary policy, a lesson for other countries that are traveling a similar path.

Suppose that were true. Would you expect to read the following story in the New York Times, in July 2006?

TOKYO, July 14 — Economists applauded the Bank of Japan’s interest rate increase, the first in six years, as a long-awaited signal that Japan’s $4.6 trillion economy is finally getting back on track.

They said that by moving pre-emptively on Friday, long before a return of inflation is likely to became a threat, the central bank was also hoping to demonstrate that it was watching prices carefully, and was therefore up to the task of stewarding Japan’s economy, the world’s second largest after the United States.

If Japan really were in a liquidity trap, this story would literally make no sense. Economic theory says the absolute worst thing you can do in a liquidity trap is a temporary monetary stimulus, which is pulled out as soon as the economy starts to show signs of life. Paul Krugman and others have shown that temporary currency injections are infective at the zero bound. But that’s exactly what the Bank of Japan did—a temporary currency injection, which was pulled out in 2006.

The NYT story from 2006 looks crazy from the perspective of 2017. Economists “applauded”?!? But the story is accurate in one sense. The Bank of Japan was happy with the condition of the Japanese economy in 2006, despite the complete lack of inflation, and they tightened policy because they were happy with this situation. Some liquidity trap!

Now let’s consider another common misconception, that countries like Japan and China are “currency manipulators”. How do we know this? Supposedly because they run large current account surpluses. In Japan’s case there is also some circumstantial evidence that the BOJ (secretly) wants a weak yen, and that its policies of QE and negative interest on reserves are aimed at creating a weaker yen.

What I find odd is that these two views often seem to be held by the same person. Japan is stuck in a liquidity trap, and Japan is a currency manipulator that is weakening the yen. It’s clearly impossible for both of these views to be true. If you are in a liquidity trap, then the central bank has absolutely no ability to affect the nominal exchange rate.

Although both of these two views cannot be correct, they can both be incorrect. And in this case they are both incorrect. Japan is not a currency manipulator, but it can and should be one. The BOJ absolutely has the power to depreciate the yen as much as they desire. The current exchange rate is 113 yen to the dollar, but the BOJ could set the exchange rate at 1000 yen to the dollar, tomorrow morning. And they could make it stick by offering to sell unlimited quantities of yen at that rate. If they ran out of yen they could always print more.

Of course if the BOJ actually did this, then they would not have to sell buy very many yen. Maybe none at all. Traders would correctly see that rapid inflation was just around the corner. No one would be anxious to accumulate lots of yen, which are about to lose 90% of their value through hyperinflation.

When I point out that the BOJ could easily create as much inflation as it liked by depreciating the yen (a point made by many other economists as well) some people will respond that the US would not allow the Japanese to do this, as it would be viewed as currency manipulation. Once again, I don’t think the people who hold this view understand what they are saying. If you insist that the Japanese not depreciate the yen, because that would be currency manipulation, then you are essentially insisting that the Japanese run a deflationary monetary policy. That’s because when countries are accused of currency manipulation they are essentially being accused of running an excessively expansionary monetary policy.

The one country that has averaged roughly zero inflation in the past several decades is also the one country that foreigners insist on bossing around.

Think about just how ironic this is. One set of foreigners, led by people like Ben Bernanke (pre-Fed), Paul Krugman, me, and many other academic economists, insist on telling the Japanese that they need a more expansionary monetary policy. Another set of foreigners, led by the United States government, insists that the Japanese need a contractionary monetary policy. That second group probably would deny the change, but telling the Japanese to refrain from currency “manipulation” is effectively the same as telling them to run a contractionary monetary policy.

So perhaps we should revise the textbook definition of liquidity trap:

“A liquidity trap occurs when the U.S. government threatens protectionist barriers against smaller, weaker countries if they refuse to run deflationary monetary policies.”

READER COMMENTS

SilasLock

Mar 2 2017 at 10:19pm

Perhaps I’m just ignorant, but the idea of currency manipulation has always baffled me. Are there any academic economists who view monetary policy this way at all?

Laidler's Ghost

Mar 3 2017 at 8:25am

Good post. (NB I think that when you say near the end that the BoJ would not actually have to “buy” many yen, you mean “sell”.)

It seems to me that a ‘defensible’ definition of currency manipulation would be the accumulation of foreign currency reserves (foreign cash or foreign government bonds) at an ‘abnormal’ rate.

On this basis a current account surplus, matched by private capital outflows, would not imply currency manipulation.

As long as the Japanese authorities print yen only to buy yen assets (bonds? equities? houses?), they would not be manipulators. The policy would still have the indirect effect of driving the yen down against the dollar, of course, but it would not be overt manipulation.

bill

Mar 3 2017 at 9:11am

It would be interesting if the BOJ promised that they’d give 1000 yen for a dollar and the Fed promised a dollar for 100 yen. Would that arbitrage have any value? ie, how much effort should I put into getting a quadrillion dollars if that’s the new price of a loaf of bread?

Majromax

Mar 3 2017 at 10:04am

Currency manipulation can still have independent meaning in this situation. Sumner’s post is based on the premise that the exchange rate is a market equilibrium, which is obviously the case for Japan even if the BoJ offers to buy unlimited US dollars at 500 Yen apiece.

If a nation also imposes capital controls, however, it can be a currency manipulator. If it’s easy to buy Russian Rubles with US Dollars but not easy to reverse the exchange at a similar price, then the official exchange rate may not be a market equilibrium.

Not all capital controls result in currency manipulation, however. Bretton Woods had lots of capital controls involving who could redeem national currency for gold, but the intent of the arrangement was for the official exchange rate to come close to the market equilibrium that would have prevailed with unlimited redemption.

Scott Sumner

Mar 3 2017 at 1:39pm

Silas, Unfortunately yes.

Ghost, That’s a distinction some people make, but it seems pretty artificial to me.

Thanks for pointing out the error, I’ll fix it.

Bill, Interesting, I never thought of that possibility.

Majromax, I’m not sure that’s a useful definition of currency manipulation, as it’s usually done for other reasons.

Todd Kreider

Mar 4 2017 at 6:22pm

1)The Bank of Japan was happy with the condition of the Japanese economy in 2006, despite the complete lack of inflation, and they tightened policy because they were happy with this situation.

What does a lack of inflation have to do with the strength of an economy. There can be strong growth at 0% inflation or 2% inflation?

2) “The one country that has averaged roughly zero inflation in the past several decades is also the one country that foreigners insist on bossing around.”

Well, two decades of around zero inflation, not several.

Craig

Mar 9 2017 at 1:32pm

Small typo: I don’t think you want “infective”

Comments are closed.