Ramesh Ponnuru directed me to a couple of Wall Street Journal pieces on the German trade surplus. The first, by Greg Ip, argues that President Trump was partly correct in pointing to this as a problem:

President Donald Trump took his bellicose economic agenda abroad last week, blasting Germany for its “very bad” trade surplus–or “evil” as one German newspaper translated it.

Though German Chancellor Angela Merkel did not seem to care for the messenger, she should nonetheless hear the message. While Mr. Trump gets a lot wrong about trade, on this particular point he’s right. Germany’s current account surplus, which combines trade and investment income, is now the world’s largest. Along with China’s, it is a dangerous imbalance that leaves others, including the U.S. and the rest of Europe, worse off.

Not surprisingly, I don’t agree. One of my objections to this argument was made just a week later in the WSJ, this time by Jason Furman:

President Trump is right: Germany’s trade balance is out of whack, and this ought to be called out. Although it’s a fool’s errand to condemn bilateral imbalances in specific industries–such as auto manufacturing–the important truth remains that Germany overall has the world’s largest current-account surplus.

Unfortunately, a fix will not be found in the sort of bilateral trade negotiations Mr. Trump’s comments seem intended to provoke. The solution is the sort of global cooperation Mr. Trump disdains: multilateral engagement on the macroeconomic drivers of the German surplus by European countries, the Group of Seven, the Group of 20 and–yes–even the North Atlantic Treaty Organization.

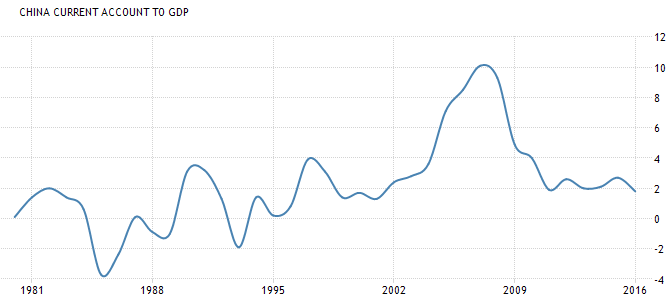

First, the facts. Last year Germany’s current-account surplus was $300 billion, or 8% of its gross domestic product. This largely reflected its trade surplus, but also some net investment income. Germany’s surplus was 50% higher even than China’s, though the German economy is only one-third as big. It wasn’t always this way. In 2000 Germany ran a slight current-account deficit.

The German surplus does not come at American expense in a simplistic, zero-sum sense. The U.S. currently has an unemployment rate of 4.3%. The Federal Reserve appears not to want that figure to go much lower because it views this as close to full employment. So if the U.S. got a boost from increased exports to Germany, the Fed would offset it by raising interest rates faster and lowering domestic demand.

Furman is right, the Fed will offset any negative impact on America’s aggregate demand. So I read the rest of the article, looking for Furman’s explanation of why Trump’s right about the German surplus hurting the US, given that the Fed offsets the impact on AD. And I found . . . nothing.

Instead Furman turns his attention to other countries within the Eurozone:

Other European countries could make a more legitimate zero-sum complaint about Germany, even if they rarely do these days. Trade partners inside the eurozone do not have access to independent monetary tools, and with a single currency there are no exchange rates to adjust. Countries like France and Spain cannot fully offset Germany’s surplus absent prolonged and painful declines in relative wages and prices.

You might assume that Germany’s big surplus is balanced out by big deficits in these two countries. Not so, Spain has a surplus of 1.6% of GDP and France has a deficit of 1.1% of GDP. Their combined current account balance is roughly zero. (Italy has a surplus of 2.4% of GDP.) So how exactly is Germany hurting other Eurozone members?

Furman then correctly points out that the German surplus is caused by domestic saving exceeding domestic investment. But can they fix this “problem”?

The solution to this problem, contra Mr. Trump, is not for Germans to buy more Chevys and Fords or to sell Americans fewer Mercedes-Benzes and BMWs (many of which, by the way, were made in places like Alabama and South Carolina). Instead it is to increase Germany’s domestic demand. Faster wage growth leading to stronger consumption would help, but the key is stronger public and private investment.

Faster wage growth? Weren’t the Hartz reforms of 2003 the most successful policy reform in recent decades, in any advanced economy? Didn’t it reduce German unemployment from over 10% to 4.3%? Does it make sense to reverse this sort of reform?

Mr. Trump did make one concrete proposal that would materially help: He called on Germany to fulfill its commitment under NATO to spend 2% of its GDP on defense. Assuming Berlin obliged without cutting spending elsewhere, that would at least make a discernible difference.

Germany current spends 1.2% of GDP on defense. If that figure were raised to 2%, at most it would reduce the CA surplus by 0.8% of GDP. But in fact, economic theory predicts a much smaller effect, as fiscal stimulus tends to boost private saving.

Greg Ip suggests that the Chinese current account surplus might have reduced US employment during 2009-14, when we were at the zero bound and it was harder for the Fed to offset the impact.

China was the largest of a group of countries that from 2003 to 2013 spent more than $5 trillion intervening in foreign exchange markets to hold down their currencies and bolster trade surpluses, according to a new book by Fred Bergsten and Joseph Gagnon of the Peterson Institute for International Economics. That drew production and jobs from deficit countries like the U.S., worsening the 2007-2009 recession and holding back the subsequent recovery. They estimate U.S. employment was depressed by more than one million jobs between 2009 and 2014 as a result.

But in these sorts of Keynesian models what really matters is not the level of the surplus, but rather the change over time. And China’s CA surplus actually fell from about 10% of GDP to about 2%, during this period.

Indeed the big China boom was one factor that brought the global economy out of its tailspin in the second half of 2009.

I wish countries would worry less about the saving propensities of other countries, and spend more effort putting their own houses in order. A good place to start is the zero bound problem. Roughly 100% of economists agree that there is a solution, they merely disagree as to whether the best solution is a 4% inflation target, or 4.5% NGDPLT, or price level targeting, or negative interest rates, or free banking, or the gold standard, or a myriad of other options. I don’t know of a single economist who doesn’t believe that monetary policymakers can overcome the zero bound problem. So let’s do it!

PS. Rereading the Furman article, it’s not clear he meant to claim that the German CA surplus hurt the US. But in that case, it’s misleading to say “President Trump is right”.

READER COMMENTS

marcus nunes

Jun 9 2017 at 8:13pm

“You might assume that Germany’s big surplus is balanced out by big deficits in these two countries. Not so, Spain has a surplus of 1.6% of GDP and France has a deficit of 1.1% of GDP. Their combined current account balance is roughly zero. (Italy has a surplus of 2.4% of GDP.) So how exactly is Germany hurting other Eurozone members?”

That already takes into account the adjustment taht Spain et al had to undertake after 2008. You need to go a bit back in time.

https://thefaintofheart.wordpress.com/2011/12/05/with-a-little-help-from-my-friends/

marcus nunes

Jun 9 2017 at 8:17pm

PS Much of that adjustment was through painful internal devaluation in Spain et al.

https://thefaintofheart.wordpress.com/2012/05/27/meade-swann-and-how-two-simple-lines-perfectly-illustrate-the-eurozone-conundrum/

Scott Sumner

Jun 9 2017 at 8:56pm

Marcus, Maybe so, but that suggests that Germany might have hurt Spain in the past, but not today.

David O'Rear

Jun 10 2017 at 7:02am

Fred Bergsten and Joseph Gagnon say China was acting like a protectionist in 2003-13 … maybe something like the US in 1985-94? Still, it might be useful to search for a non-protectionists source on the matter.

The Peterson Institute for International Economics has not shown itself to be neutral on the issue of international trade.

Thaomas

Jun 10 2017 at 10:24am

While a German trade surplus is not harmful to the US per se, it may be a (desired by the German political class) by-product of the failure of the ECB to maintain ngdp growth in the Eurzone o even to maintain the average EU price level on track. Faster EU growth would be good for the US, particularly since the Fed has itself been failing to keep the price level raising at a stable, predictable rate.

Thaomas

Jun 10 2017 at 1:21pm

Scott,

But would Spain and the rest of the Eurozone be even better off with more ECB stimulus, higher German inflation and a less devalued German real exchange rate?

bill

Jun 10 2017 at 4:40pm

Writers like to write “President Trump is right” because it feels contrarian and/or increases clicks. Sad.

Scott Sumner

Jun 10 2017 at 5:59pm

Thaomas, Yes, the ECB was too tight.

mariorossi

Jun 12 2017 at 4:14am

It seems a bit pointless to discuss the trade surplus of a part of a currency area. I am pretty sure Florida must run some spectacular current account deficit (not sure the data is available to check).

The Eurozone current account balance is currently 3% of gdp I think. It was flat not long ago. It seems within the normal variations due to differences in the economic cycle.

You can argue the Euro is currently undervalued, but given the unemployment level in southern Europe, you’d be surprised if it wasn’t…

I am also not sure I believe we already are in the long term. I don’t think it’s impossible the effects of bad monetary policy under Trichet are still having an effect 5 years later. Disrupted economic patterns can take a long time to heal especially in less dynamic economies like Italy.

Comments are closed.