The Economist is probably the best magazine in the world, but a recent cover story on “The German problem” is just appalling:

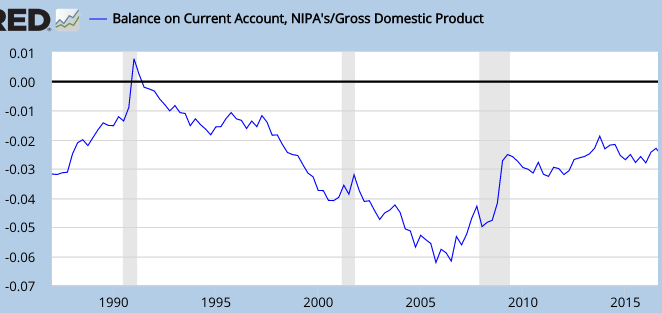

For a large economy at full employment to run a current-account surplus in excess of 8% of GDP puts unreasonable strain on the global trading system. To offset such surpluses and sustain enough aggregate demand to keep people in work, the rest of the world must borrow and spend with equal abandon. In some countries, notably Italy, Greece and Spain, persistent deficits eventually led to crises. Their subsequent shift towards surplus came at a heavy cost. The enduring savings glut in northern Europe has made the adjustment needlessly painful. In the high-inflation 1970s and 1980s Germany’s penchant for high saving was a stabilising force. Now it is a drag on global growth and a target for protectionists such as Mr Trump.

There are so many misleading statements here that one hardly knows where to begin:

1. The Economist confuses trade and aggregate demand, which are entirely unrelated issues. People do not need to “borrow and spend with . . . abandon” to insure an adequate level of aggregate demand, rather they need a sensible monetary policy.

2. We know that Italy, Greece, and Spain were not “forced” to run large deficits by Germany, because Italy and Spain have sizable surpluses, and Greece’s current account is roughly balanced. That would not be possible if the German surplus forced these three countries to run deficits. It’s true that these countries currently have a shortfall of AD and high unemployment, but that’s due to a combination of the ECB’s tight money policy and very rigid labor market regulations, not Germany’s trade policy.

3. It’s true that at a global level a German CA surplus must be offset by an equal deficit elsewhere. But the German economy is only a very small percentage of the global economy, so a Germany CA surplus of 8% of GDP implies a “rest of world” deficit of far less than 1% of GDP.

4. As a practical matter, one can see the German surplus as being offset by the even larger US CA deficit. But obviously this US deficit does not create an AD problem in the US, as the Fed is currently involved in raising interest rates to prevent AD from rising too rapidly! The rest of the world (not the US and not Germany) is currently running a large CA surplus. So Germany certainly does not force the rest of world (excluding the US) to run a deficit.

5. Some argue that current account deficits are problems even if they don’t depress AD. Perhaps the US current account deficit has led to de-industrialization. If so, that must have happened before 1987, as the US deficit has not increased at all over the past three decades, so it can’t have contributed to recent de-industrialization. It’s a bit over 2% of GDP, even less than in 1987.

6. Some argue that trade causes job loss through “re-allocation of labor”. This is a channel that might apply to the US, even if our CA deficit is not getting “worse”. But this argument would equally apply to Germany, indeed even more so, as it’s CA has changed more rapidly than in America. So Germany has presumably been doing a lot of re-allocation from its declining industries to its advancing industries. Re-allocation is a genuine challenge (from both trade and automation) but it has absolutely nothing to do with current account balances.

7. The Economist makes the common error of confusing CA deficits with net borrowing. The German CA surplus in no way “forces” other countries to borrow more. It’s up to each individual, business and government to decide how much they want to borrow. Even in a world with zero debt, there would be large and persistent CA imbalances as assets are bought and sold across borders. The Economist is simply wrong, CA balances and net borrowing are completely separate issues.

Their entire cover story seems based on the worst elements of Keynes’s General Theory, where he speculates that the mercantilists might have a point. These ideas were wrong in the 1930s, and they are still wrong. Unfortunately this sort of article gives aid and comfort to protectionists like Donald Trump, Steve Bannon and Peter Navarro, and that’s the last thing the world needs right now.

Germany is not the problem; it’s the solution. More countries should emulate Germany’s labor market reforms and its high savings rate. If we all did so, the world would be much better off.

PS. Tomorrow I say goodbye to Boston and leave for Southern California by car. While I’m getting my kicks on Rte. 66, blogging will be spotty.

READER COMMENTS

marcus nunes

Jul 19 2017 at 10:22am

Scott

Conceptually, you are correct. But othr “sentiments” are at play

https://thefaintofheart.wordpress.com/2015/07/02/germans-we-have-them-greeks-and-the-other-lot-by-the-balls/

“I pushed back politely. Look, I said, it’s not Greece I’m worried about. It’s Italy. Third-biggest bond market in the world. Bond spreads this morning again heading over 7% (before the ECB intervened this to push them back down again.) Too big to fail, too big to save. Is the government, even one under a new Prime Minister, going to push through sufficient austerity to avoid a default?”

“Now the consultant perked up, speaking what he too believes to be the unvarnished truth. They have to, he said, because “to be blunt about it, we have them [both the Greeks and the Italians] by the balls.”

More generally:

https://thefaintofheart.wordpress.com/2013/11/02/a-german-obsession-usually-proves-to-be-costly/

Kevin Dick

Jul 19 2017 at 12:42pm

Bob Voyage. Welcome to Californistan, where the sun and sanctinomy are always shining.

Do you feel comfortable disclosing your city? You might want to think about doing some meetups. You could call the Sumnerian Summits 🙂

Or you could be a guest at a Less Wrong or Slate Star Codex one.

If you get up to the Bay Area, let us know!

Rajat

Jul 19 2017 at 1:24pm

Safe drive, Scott. Incidentally, former RBA governor Glenn Stevens took his retirement holiday earlier this year driving down Route 66. Will you be renting a white Mustang as well? http://amp.smh.com.au/business/the-economy/reserve-banks-hit-to-retirees-and-first-home-buyers-is-all-part-of-the-plan-20170106-gtn3d6.html

Gamal Atallah

Jul 19 2017 at 2:03pm

The Economist magazine supported the Iraq war in 2003. And you write that it is “the best magazine in the world”? Interesting.

Bob Murphy

Jul 19 2017 at 2:32pm

Scott,

Be honest: This was your favorite cartoon from the best magazine in the world. Am I right?

marcus nunes

Jul 19 2017 at 3:04pm

This is also relevant:

“Germany is engaged in a purifying crusade, epitomized by its push for the unconditional adoption of “austerity” by all member countries of the euro, in particular the so-called PIIGS.”

https://thefaintofheart.wordpress.com/2012/05/13/saint-and-sinners-germany-the-periphery/

Alan Goldhammer

Jul 19 2017 at 3:42pm

Is this a permanent move? If so, where in CA? Have a safe journey.

Leo

Jul 19 2017 at 4:03pm

Michael Pettis would disagree with this assessment. The argument that Pettis puts forth in a number of books and articles, is that Germany has artificially suppressed wages in order to keep unemployment low (see the Hartz Plan). This is a form of excess savings and manifests in a current account surplus. Pettis argues that China is doing the same thing. It’s not that current account deficits are inherently good or bad, the issue is when domestic policies inflate the surpluses or deficits. Also, while the German C/A surplus may not be large relative to world GDP, especially when compared with China, it accounts for almost all of the EZ wide surplus. German merchandise trade is also about 25% of all intra-EZ merchandise trade and Germany runs a significant surplus with the rest of the EZ. Germany’s C/A surplus is also equivalent to around 2.5% of EZ GDP

Colin Fraizer

Jul 19 2017 at 8:09pm

Are you allowed to call it a magazine now?

Pyrmonter

Jul 19 2017 at 8:41pm

The Economist lost me when it turned on a dime from supporting Lamont’s policy of staying in the ERM to leaving it (though events suggest it might have been right – the problem the tether solved, of controlling inflation expectations, had been solved). However, it has lurched decidedly to the social democratic left in the last few years; not what it was.

Scott Sumner

Jul 19 2017 at 9:51pm

Marcus, Yes, but of course that’s a different issue.

Kevin, Mission Viejo.

Rajat, My blue Maxima.

Bob, No, it was the one that featured me playing the drums.

But that’s a good one too.

Alan, Yes, Mission Viejo.

Leo, I’m not sure why these facts matter. Who cares about Germany’s balance with the rest of the eurozone? The non-German part of the eurozone runs a sizable surplus ($120 billion), so even if you think CA deficits are a problem (and they are not), it is not hurting the eurozone.

China’s surplus is 1.6% of GDP, so it’s a minor issue even if one assumes it’s a problem.

Pettis is very knowledgeable about China, but I don’t agree with his views on global macro.

Colin, I forgot, it’s a newspaper.

A

Jul 20 2017 at 10:51am

Clemens Fuest made a similar point on Project-Syndicate.

“Germany represents 4.4% of global GDP. So a reduction in its external surplus, even by as much as 2.5 percentage points from the current level of 8.5% of GDP, would have a minimal impact on the global economy. An increase in demand equal to 2.5% of German GDP would boost global demand by just 0.1%.”

Thaomas

Jul 21 2017 at 7:19am

German’s failing to follow an NPV fiscal policy rule (and therefore th=o have had slower growth that it could have had which growth in turn would have been good for the rest of the Eurozone) is indeed NOT a big problem now and was not even during the worst of the recession.

Germany IS a problem for the Eurozone because they were and are the source of the pressure that prevented ECB from keeping NGDP on its pre-crisis rate and to even raise ST interest rates in 2010. It’s one aspect of what Marcus Nunes’s qoutes.

Tom

Jul 21 2017 at 10:17am

My issue with discussions like these is that they always almost exclusively focus on production and consumption which are demanded to be steadily growing. It’s also just absolute numbers and percentages but no real consideration of necessity. So what if German workers had more money to consume. Does consuming / producing more stuff make us better of?

The Double-entry Bookkeper

Jul 21 2017 at 1:05pm

“The Economist is simply wrong, CA balances and net borrowing are completely separate issues”

A current account surplus indicates that a country is a net lender to the rest of the world, while a current account deficit indicates that it is a net borrower.

Alec Fahrin

Jul 22 2017 at 2:12am

Leo,

Germany’s current account surplus in 2016 was larger in relative AND absolute terms than China’s. Same for the capital account.

Pretty amazing, right? The Chinese have rebalanced their economy towards services and consumption quite rapidly. Most recent counts put it at 53% services and 50% consumption / GDP. Massive capital outflows in 2014-2016 (since slowed) helped of course.

Nonetheless, let’s keep our facts straight, especially with China the perennial inspirer of fake economic news in the West. Pettis has been proven too skeptical of China’s ability to rebalance, as he has grudgingly admitted.

As for Germany, I do believe the German current account surplus of over 8.5% of GDP is a global net negative. We don’t need lower interest rates and more savings right now. We need more demand, especially in the Eurozone.

This is where I fundamentally disagree with Sumner’s views. In a private sector debt crisis, pump-priming can help significantly if combined with looser monetary policy and the end goal of boosted NGDP. Monetary policy simply cannot do it alone.

Comments are closed.