I am currently in DC attending a star-studded macroeconomic policy conference at the Peterson Institute. Today’s participants included Bernanke, Summers, Blanchard, Draghi, Fischer, and many other eminent economists. Bernanke’s paper was by far the most interesting, especially his proposal for addressing the zero bound problem:

So, to be concrete, at some moment when the economy is away from the ZLB, suppose the Fed were to make an announcement like the following:

(1) The FOMC has determined that it will retain its inflation-targeting framework, with a symmetric inflation target of 2 percent. The FOMC will continue to pursue its balanced approach to price stability and maximum employment, meaning in particular, that the speed at which the FOMC aims to return inflation to target will depend on the state of the labor market and the outlook for the economy.

(2) However, the FOMC recognizes that, at times, the zero lower bound on the federal funds rate may prevent it from reaching its inflation and employment goals, even with the use of unconventional monetary tools. The Committee agrees that, in future situations in which the funds rate is at or near zero, a necessary condition for raising the funds rate will be that average inflation since the date at which the funds rate first hit zero be at least 2 percent. Beyond this necessary condition, in deciding whether to raise the funds rate from zero, the Committee will consider the outlook for the labor market and whether the return of inflation to target appears sustainable.

Of course I’d prefer NGDP level targeting, partly for reasons outlined in this post. But Bernanke’s proposal would still be a dramatic improvement over current policy. More importantly, this is something that is much more politically feasible than any other proposal that I’ve seen. It actually makes the long run future price level more predictable than under current policy, which conservatives should love. It makes policy more expansionary at the zero bound, which liberals should love. It also eliminates the need to offset under and overshoots of inflation when not at the zero bound, which should assuage the fears of those who oppose traditional forms of level targeting. Indeed I think Bernanke’s proposal is now the odds on favorite to be official Fed policy the next time the US hits the zero bound. Most people at the Fed understand that something like this is needed at the zero bound, and Bernanke’s proposal could be sold to Congress as being fully consistent with the Fed’s 2% inflation target.

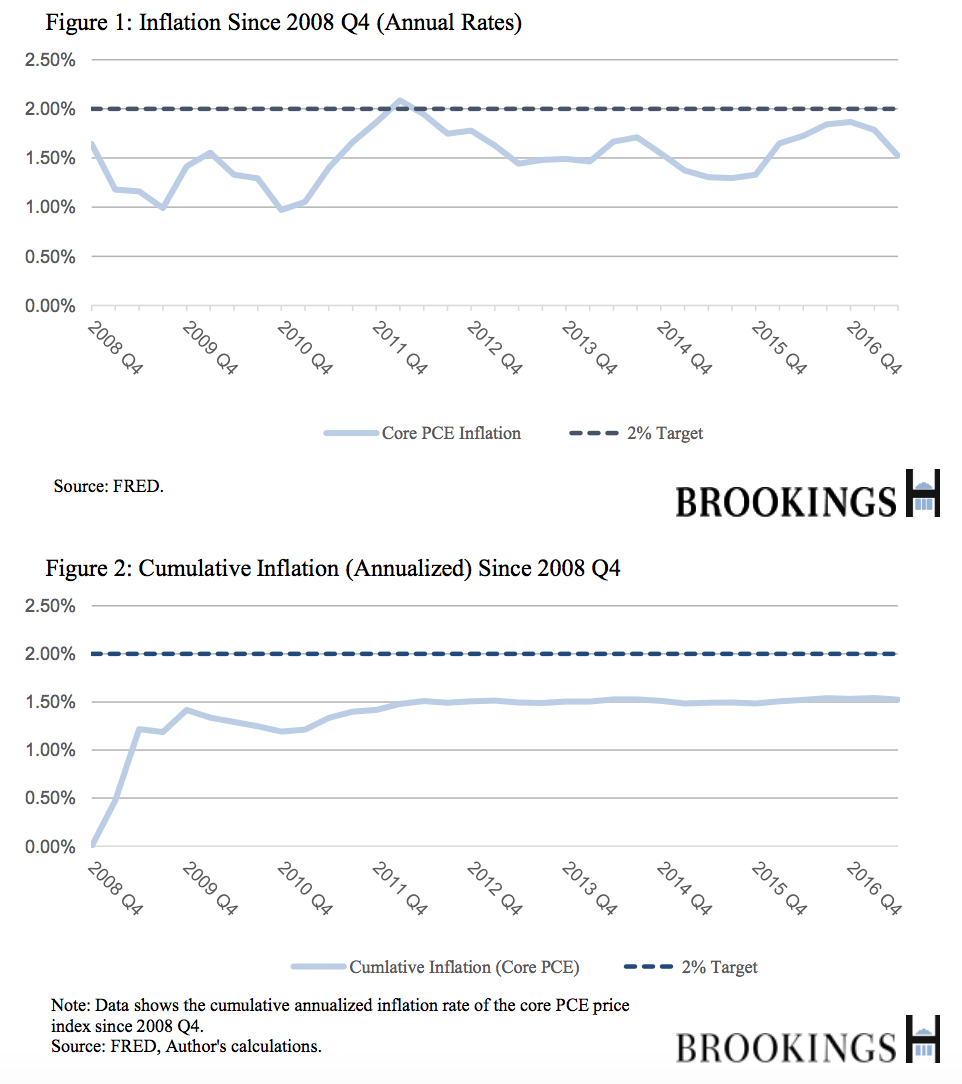

You might assume that under Bernanke’s proposal we’d still be at the zero bound, because we are still far below the 2% trend line from 2008. Not necessarily:

Note though, that if this policy rule had been in place prior to 2008, and if it had been understood and anticipated by markets, then longer-term yields would likely have been lower and the effective degree of policy accommodation during the past decade might have been significantly greater. In that counterfactual world, inflation might have been higher and the average-inflation criterion might have already been met. This is because the Fed would have already communicated their intention to be more accommodative going into the ZLB episode.

READER COMMENTS

bill

Oct 13 2017 at 12:10am

I have a question. Where he says “longer term yields would have likely been lower”, do you agree? My hunch is they would have been higher precisely because the policy accommodation would have been greater.

Scott Sumner

Oct 13 2017 at 12:13am

Bill, I suspect you are right, but it’s hard to be sure

ChrisA

Oct 13 2017 at 1:30am

Scott – With Bernanke’s proposal how do you feel about an explicit inflation target of 2% but a real target of 1.5% (as we seem to have thanks to the Fed’s worry that inflation will spiral out of control as it approaches 2%). Its seems to me that this is actually fine.

Michael Byrnes

Oct 13 2017 at 7:02am

Is it fair to describe this as “2% flexible inflation targeting with a special ZLB guardrail”?

I guess the question is how well this kind of policy would differentiate between “inflation is low because policy is very accommodative” and “inflation is low because long-term growth expectations are pessimistic”.

An NGDPLT guardrail would be better. “At or near the ZLB, rates won’t be hiked until the trend rate of NGDP growth returns to its trend from the 5 years prior to the recession.” Not as good as full NGDPLT, but maybe an effective was to gradually transition policy towards NGDPLT.

Effem

Oct 13 2017 at 9:11am

Prediction: the next time we hit the zero-bound the Fed will not have the political credibility to change its policy.

Steve F

Oct 13 2017 at 5:33pm

What I don’t understand is why inflation targeting is even in the conversation. AS can shift left for reasons unrelated to (and unaffected by?) monetary policy. This pushes up inflation and pushes down output. When that happens sufficiently enough such that the Fed is exceeding the inflation target yet output is depressed, the Fed wants to increase output, but how can they do that when that would just push up inflation further beyond the already exceeding target?

If I have this right, how do economists who support inflation targeting account for this problem? Doesn’t having an inflation target mean that the Fed has self-imposed restraints that make some recessions inevitable?

Scott Sumner

Oct 13 2017 at 8:09pm

ChrisA, If true, that would not be “fine” with me.

Effem, No one would stop the Fed from doing what Bernanke suggested, indeed hardly anyone would try.

That’s not really a concern.

Steve, I suppose they would defend it as “flexible inflation targeting”, willing to allow some divergence during supply shocks.

Thaomas

Oct 13 2017 at 8:55pm

Yes it does seem to be an improvement, but not as much as 1) admitting that the Fed has NOT had a a symmetric inflation rate policy and hence cannot “retain” it and b) removing the reference to the ZLB from timing of using a PL target.

Alex S.

Oct 16 2017 at 9:35am

Fed officials seem to see lower long-term interest rates as an unequivocal sign of an easy monetary policy (most likely because they believe inflation expectations are well anchored at 2%–very wrong according to TIPS spread). In their world, aggregate demand growth doesn’t depend on inflation plus RGDP growth (i.e., NGDP growth) but whether real interest rates are low.

Comments are closed.