Over the past few years, I’ve noticed that people tend to predict that Bitcoin is a bubble, and then later suggest that a subsequent price drop shows that it was a bubble. Thus lots of pundits said Bitcoin was a bubble when its price was at $30. Then when it was at $300, even more suggested that it was a bubble. Each time the price plunges they say “I told you so.” Now the price of Bitcoin is over $3300, and even more people are saying it was a bubble. Noah Smith has a new piece in Bloomberg:

Yep, Bitcoin Was a Bubble. And It Popped.

His main piece of evidence is that the price rose sharply and then fell sharply. But that sort of price pattern also occurs in 100% efficient markets that are highly volatile because the fundamental value of the asset is hard to ascertain. And if there ever was an asset with a value that is difficult to ascertain, it’s Bitcoin. I have no clue as to what Bitcoin should be worth, and I doubt anyone else does either.

Bubble theories are only true if they are useful, and they are not useful. The people who said it was a bubble at $30 were implicitly giving you advice not to buy. Ditto for those who said it was a bubble at $300. This advice was exceedingly non-useful; in fact if you followed the advice of bubble proponents you missed out on the opportunity to earn a massive profit investing in Bitcoin. That’s why I don’t follow the advice of bubble theorists; it’s not useful. BTW, I don’t own Bitcoin for unrelated reason; I prefer index stock (or bond) funds.

In any efficient asset market with an extremely volatile price, the current value of the asset will usually be far below the historical maximum price. That’s equally true if bubbles don’t exist. BTW, I define a bubble as a price that is clearly too high relative to fundamentals, and thus an asset with a poor expected return, based on rational analysis. In fairness, Noah Smith defines it differently:

Formally, an asset bubble is just a rapid rise and abrupt crash in prices.

In the real world, the vast majority of times where people speak of bubbles they are using my definition, assuming market irrationality. And it’s clear that while Smith’s definition of bubbles does not explicitly endorse market irrationality, he thinks they provide pretty strong evidence for that hypothesis:

Defenders of the efficient-market theory argue that these price movements are based on changes in investor’s beliefs about an asset’s true value. But it’s hard to identify a reason why any rational investor would have so abruptly revised her assessment of the long-term earnings power of companies in 1929, or the long-term viability of dot-com startups in 2000, or the long-term value of housing in 2007.

Actually there is very good reason why investors might have revised their expectations for future earnings in late 1929, we were entering the Great Depression. But his point is valid for the 1987 stock crash.

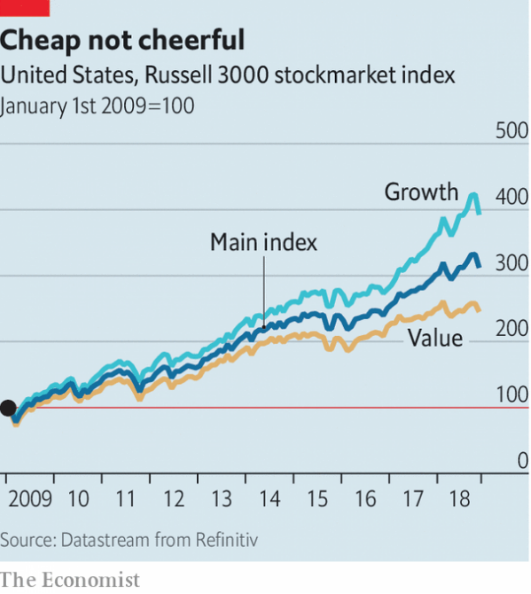

Speaking of efficient markets, there’s another nail in the coffin of anti-EMH theories. When I started blogging in early 2009, people pointed me to all sorts “anomalies”, which they believed show that markets are not efficient. I’ve done many posts explaining how those theories have failed to do well in the period since I became aware of them. Recently I learned of the failure of another anti-EMH theory that was provided to me back in early 2009—value stocks as a good investment:

Just to be clear, I understand that value stocks had an amazing run for quite a long while. So did Bitcoin. My point is that anti-EMH theories are not useful, because by the time you start trying to take advantage of them they are likely to stop working. If that were not true then mutual funds based on highly robust anti-EMH theories would outperform index funds.

Market’s are amazingly efficient, and you’d be wise to base your life decisions on that assumption. For instance, if someone insists that his investment fund consistently offers really high returns, year after year, and the returns seem uncorrelated with the broader market, that should raise a red flag. Otherwise you might find that the investment manager made off with your money.

In contrast, the SEC does not believe in the EMH, and ignored warnings about a fund with implausible returns, year after year.

READER COMMENTS

Diocretus

Dec 11 2018 at 6:37pm

I don’t agree that calling something a bubble implicitly implies you shouldn’t invest in it. Rather, it implies that any investment in it is not based on the underlying value of the asset, but rather on the inflated valuation market participants place on it. Plausibly if you think they will continue to place this higher valuation on it then at least short term investments can be profitable.

Cliff

Dec 11 2018 at 10:57pm

I imagine the market is getting more efficient all the time. But there’s no question there have been inefficiencies in the past, and I think traders would tell you there are still inefficiencies now that allow them to exploit private information and low lag to generate excess economic returns in the stock market.

If you look at certain historical hedge funds, there are some that had very outsized returns, claimed to be engaging in arbitrage, and had such a huge volume of transactions that there is no way they could have lucked into their returns.

Scott Sumner

Dec 11 2018 at 11:36pm

Fair point. Market’s need enough inefficiency to motivate people to try to make markets more efficient. I was referring more to the idea that there’s publicly available information that an average person can use to earn outsized returns, just waiting to be absorbed like fruit plucked from a tree. That’s what the “bubble” theory implies. The proponents are basically saying “Look at that far too high asset price; returns going forward will be very low on average.” They can’t really know that.

By the time an average person reads about an investment scheme, it’s too late for them to benefit. Some will work, but they have no way of knowing which ones.

robc

Dec 12 2018 at 9:23am

As you state, there are rare exceptions. A number of years back, I wanted to short the hell out of SCO at $18, because I knew it would be going to $0 or near $0. But I didnt because I dont short stocks, and the risk of being wrong is too high. And I would have been sweating when it bounced off $24.

But I was right. I worked in the open-source industry (that sounds like an oxymoron) at the time and knew enough about the Linux code to know that SCO’s lawsuit was BS and that the company had nothing else going for it.

I think all the information was publicly available allowing the average person to make oversized returns, but maybe not publicly understandable.

Scott Sumner

Dec 12 2018 at 1:31pm

robc, I don’t agree. If the information was publicly available the stock would not have been at $18. You may not like shorting, but plenty of smart money does. It can’t have been obvious that the stock was too high.

Being right about a single investment, ex post, tells us nothing about bubbles or market efficiency.

robc

Dec 12 2018 at 2:32pm

groklaw.net (I read it a lot at the time) covered the SCO lawsuits in insane detail. Between that and the fact that the Linux code was open source meant that all the necessary info was available to the public.

I don’t know how to look up historical stock prices for symbols that no longer exist (well, not for that company, SCO is being used for something else now), but it remained high for a lot longer than it should have considering the amount of info available. From what I remember, it had very high short positions though, so plenty of people were shorting it the way I wanted to.

I agree with you on 1 stock, and I believe in efficient markets, at least mostly. It gets efficient in a time scale that allows some big money to be made some times.

robc

Dec 12 2018 at 2:52pm

Looking up some info, because it has been a long time and I can’t remember everything, but I think SCOX (that was its stock symbol, not SCO) fits your definition of a bubble.

In Feb 2003, its stock price was just over $1. They filed a lawsuit against IBM and the stock price rose to over $19 by September. It began to decline in 2004 and was down to $3 by Oct 2004. In late 2006 it was back to $1, and was trading at 45 cents in 2007, which is the last reference I can find easily.

I (mis)remember it hitting $24, but I am probably wrong. Instead of $18 and $24, maybe it was $12 and $18 (and actually $19).

Either way, it was a quick rise that was clearly too high based on fundamentals. It is weird, all the info was public, but interpreting the information may have been hard, so investors could have rationally expected that there was a probability of winning the lawsuit. There was also a lot of conspiracy theories going around at the time (some of which may even be true), so that makes the information even more confusing.

Peter McCluskey

Dec 13 2018 at 1:03pm

robc is mostly right here. I made $50k shorting SCO then.

Hardly any smart money paid attention to it because it was time-consuming to evaluate all the relevant evidence, and it wasn’t easy for anyone outside of the open-source movement to guess whether that was a good use of their time. Partly because that kind of evidence rarely yields a clear conclusion that the company is overpriced, and partly because with small companies like that there aren’t many shares available to short.

Mark Z

Dec 12 2018 at 1:36am

“Formally, an asset bubble is just a rapid rise and abrupt crash in prices.”

That’s… a bad definition of a bubble. It’s trivial. Every asset I guess is always in an asset bubble. Smith may as well have said, “an asset bubble is when the price of an asset varies with time.”

I was going to say, people talking about bubbles often seem to conflate ‘noisiness’ with being a bubble. Bitcoin prices are certainly noisy, which makes sense for any asset with a lot of uncertainty. But apparently some people actually define noise as a bubble.

I think the correction (or at least, actually useful) definition of a bubble is: when a rapid rise in prices is predictive of a subsequent fall in prices. If a big rise in prices one day is highly predictive of a collapse in prices the next day (or week, month, or whatever the hypothetical period of the cycle is), then it’s likely a bubble. But if the price seems no more likely to down than up after a big increase the prior day, i.e. is, in the short run is more or less a random walk, then it’s not a bubble.

Brian Donohue

Dec 12 2018 at 9:50am

Great post:

5/16/1997: $1.73

4/25/1999: $105.06

8/13/1999: $48.72

12/10/1999: $107.13

9/28/2001: $5.97

That’s Amazon. Definitely a Noah bubble. DO NOT BUY IN 2001!

Garrett M

Dec 12 2018 at 10:17am

It’s interesting that you would consider buying “value stocks” to be “anti-EMH”, considering the amount of work Eugene Fama has done trying to show that the value premium is risk-based. Not that I agree with Fama.

Gene Laber

Dec 12 2018 at 11:26am

You refer to a bubble as a price that is high relative to fundamentals and thus reflecting poor returns to the asset.

What are the fundamentals of Bitcoin? Alternatively, what are the returns generated by the Bitcoin asset? The stock and bond index funds that you prefer generate returns from assets that are held by the firms issuing the stocks and bonds. Those firms are producing goods and services to generate the returns. Are there similar returns from assets held by Bitcoin?

Scott Sumner

Dec 12 2018 at 1:35pm

Mark and Brian, Good comments.

Garrett, Good point, but is the risk premium plausibly large enough to explain the earlier excess performance?

Gene, Bitcoin produces a flow of services: liquidity, hiding wealth, etc.

Nishu Chauhan

Dec 13 2018 at 1:00am

It’s fascinating that you would consider purchasing “esteem stocks” to be “hostile to EMH”, considering the measure of work Eugene Fama has done attempting to demonstrate that the esteem premium is hazard based. Not that I concur with Fama !!

Scott Sumner

Dec 13 2018 at 2:17pm

I think you misunderstood. It was opponents of the EMH who told me (in the comment section) that value stocks proved the theory was false. I never made any claims about value stocks.

Thomas Sewell

Dec 13 2018 at 1:25am

Not a real prediction market, and not to be used for anything with scientific rigor, but you may be interested in this ongoing poll of primarily tech folks about the value of Bitcoin at the middle of 2019.

Scott Sumner

Dec 13 2018 at 2:21pm

robc and Peter, I’m no expert on that stock, but my point is that markets are mostly efficient, and any inefficiency is just large enough to motivate people to nudge prices back to the appropriate level. There will be cases like you describe, but ex ante it’s not clear to average people which of those cases are good investments and which are not. An expert may occasionally spot a $100 bill on the sidewalk, that others don’t see.

robc

Dec 13 2018 at 2:46pm

I think we are both right.

All the evidence needed was publicly available. But, to make money off of it, you needed to be an expert in two different fields that have little overlap. You needed to understand open-source software, and the linux codebase in particular AND you needed to understand financial markets and investing.

Even then, because of the size of the company and the limited amount of stock available for shorting, there wasn’t the opportunity to make mega-money, but someone could, as Peter points out, make a nice personal chunk.

dede

Dec 14 2018 at 1:57am

“And if there ever was an asset with a value that is difficult to ascertain, it’s Bitcoin”

My two cents question is why do sensible people call it an asset? For what it is worth, I am of the opinion that anything on the credit side of a ledger is a liability…

Matthew Waters

Dec 14 2018 at 3:40am

The “anti-EMH” theories of value stocks can coexist with competitive allocation of capital. A value stock can take years to pay off while capital can flee far more quickly. For example, Buffett has benefited from two sources of capital which do not flee based on short-term returns (equity in Berkshire and insurance float). Otherwise, the value portfolio performs poorlyunder most investment managers’ incentive structures.

On Bitcoin: Look, if a market truly runs on finding a greater fool, it’s not sustainable. Bitcoin had one true, honest use: Settlement of illegal transactions. Bitcoin proponents could have analyzed that use, but all Bitcoin proponents in my experience believed complete nonsense about monetary economics.

With how anti-EMH arguments are portrayed, I will portray the pro-EMH argument on Bitcoin. Extreme EMH would say one should be indifferent between Bitcoin at $15k and $15k in index funds.

First, stocks and bonds pay interest from outside the markets. Bitcoin, like gold, has to rely on future people paying more for it. If it’s just people selling something back and forth, then the market as a whole will ultimately just lose transaction costs. Assets without yields start at a fundamental disadvantage.

To sustainably make money with Bitcoin at $15k or at $300, there had to be large demand for Bitcoin truly for its own utility. In the run-up to $15k, the true demand went the other way. Steam stopped taking Bitcoin due to the price swings. Lightning Network was/is supposed to save Bitcoin, but that’s yet to be seen.

To me, “anti-EMH” means that investors can benefit from *some* ideas of fundamentals. Market prices are ultimately just what the very last stock or very last Bitcoin traded at. Real-world liquidity and transaction contraints go against simplistic pro-EMH arguments to correct the market.

Comments are closed.