Inflation, defined as an increase in the general level of prices, is not directly observable more than the general price level itself (also called “overall price level”). You cannot go to your local convenience store and order one unit of GDP, asking, “How much is it?” —that is, how much is the general price level for one unit of GDP, made of a fraction of an automobile, a few words of medical advice, a bit of an Amazon delivery service, a dozen bubble gums, etc.? Inflation is estimated by measuring the increase in the average price of some “representative” basket of goods and services. It is incorrect to take this estimate of inflation (the consumer price index or CPI, for example) and try to trace the causes of inflation back to observed individual prices, for the latter also incorporate relative price changes (among goods and services) not caused by inflation.

Consider the following standard pronouncement. The Wall Street Journal writes (“Record Diesel Prices Pressure European Drivers, U.S. Deliveries,” May 13, 2022):

Rising energy prices are a major factor contributing to the persistence of inflation

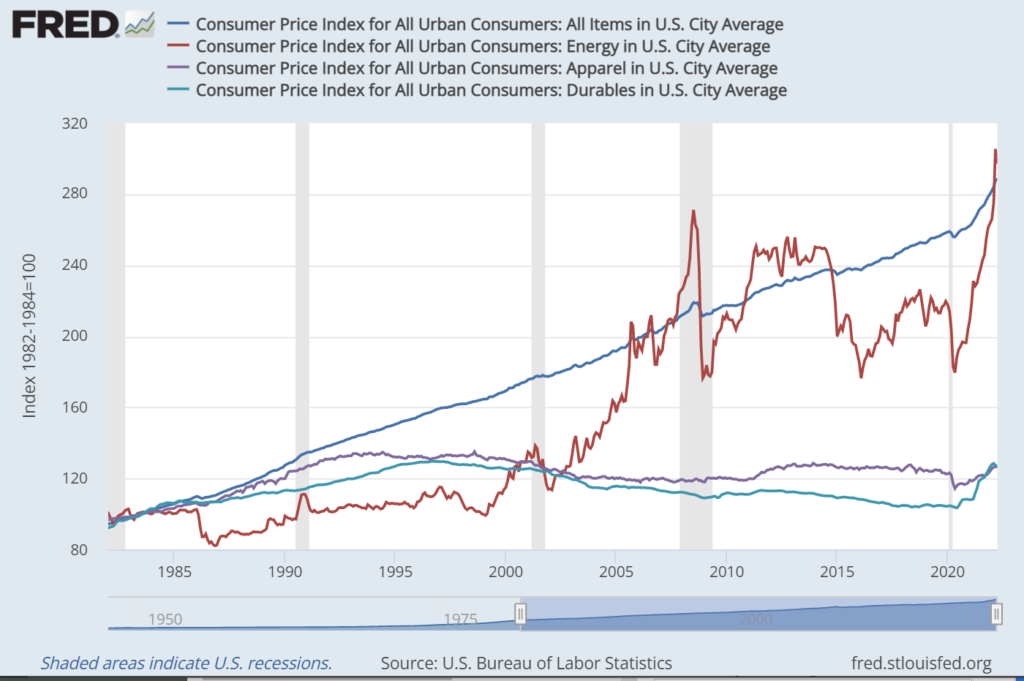

The following historical observation can serve to falsify such a claim. On the chart below, let’s focus on the period from January 1999 to July 2008. Over this period the average price of energy for American consumers (calculated from a sub-index of the CPI) increased nearly non-stop and was 172% higher at the end of the period than at the beginning. But some other prices decreased. For example, the average price of consumer durable goods (including such things as cars and appliances) decreased by 12%; the cost of apparel, by 10%. While inflation was estimated to be 33%, some prices increased, other decreased.

And that is the point. Without inflation, relative prices would continue to change, some prices increasing, others decreasing. The measured total change of a given price is, by definition, the sum of its relative change (relatively to other goods, without inflation) and of the inflation rate:

total price change = relative price change + inflation.

One cannot say that the total price change “contributed to” inflation, because inflation has already been added to the relative price change to produce the total. If you obtain 3 by adding 1 to 2 (2+1), it does not make much sense to conclude that 3 “contributes” to 1 (except perhaps in a very formal algebraic way).

It is true that if a supply shock reduced the production of oil and thus of all consumer goods that use this input, there would be a one-time increase in the general price level because the same quantity of money would be chasing fewer goods. But there is no reason why inflation would continue month after month, year after year, as we see for the CPI in our chart. A persisting inflation (what people usually mean by inflation) requires more new money chasing the existing (or a fortiori reduced) volume of goods.

This argument rests on standard microeconomic theory (which deals with relative prices and is also called “price theory” for that reason) and on a macroeconomic theory called monetarism. But note that any counter-claim must also be based on some economic theory, or else it is just a vague ad hoc intuition. The media and alas even the financial press often rely on the latter.

Over the past few decades, monetarism of the Milton Friedman type has been abandoned or modified by economists. But this does not necessarily make it invalid, especially in its fundamental result that an increase in the money supply over and above the demand of the public for money will, after a lag, generate inflation. (I understand that co-blogger Scott Sumner defends a modified version of monetarism, which does not seem to contradict my claim above, at least in ordinary circumstances.)

An argument close to mine above is presented in a recent article by John Greenwood (Invesco, Ltd.) and Steve Hanke (John Hopkins University): “On Monetary Growth and Inflation in Leading Economies, 2021-2022: Relative Prices and the Overall Price Level,” Journal of Applied Corporate Finance 33:4 (2021). A paragraph from the abstract of the article provides a good summary:

The authors argue that this consensus [on current inflation being largely generated by “supply chain disruptions”] will prove to be wrong because of its failure to distinguish between relative price changes and changes in the overall price level. The movement of any single set of relative prices fails to convey information about the overall inflation rate. And as asserted by the Quantity Theory of Money, the overall inflation rate and price level are determined by changes in the money supply broadly measured. Changes in relative prices, on the other hand, result from changes in demand and supply in the real economy, making them independent of changes in the money supply. So, while a doubling of the money supply will result in a doubling of all nominal prices, relative prices remain unaffected by monetary policy.

READER COMMENTS

Craig

May 17 2022 at 1:57pm

Confusion for some of course, but from the government? I’d suggest they’re engaged in straight up gaslighting.

Milton Friedman wrote: “Inflation is always and everywhere a monetary phenomenon.” And also:

Of course now the sheikhs are now Putin.

Mark Brady

May 17 2022 at 7:51pm

Pierre, you write that inflation is “the consumer price index or CPI, for example.” I could well imagine you taking someone to task for such a statement. 🙂

Inflation is a process, and it may be measured by the rate at which the CPI is increasing.

artifex

May 17 2022 at 8:24pm

He only gives it as an example of a price index used to estimate inflation.

Pierre Lemieux

May 18 2022 at 3:53pm

Mark: Artifex is right. I was trying to economize on words!

Mark Brady

May 18 2022 at 11:43pm

Okay, but couldn’t that be said about many writers which you take to task? 🙂

vince

May 19 2022 at 1:21am

The CPI includes imported goods. If China exports goods to the US at lower prices, the CPI declines. China exported deflation. What’s the problem?

vince

May 19 2022 at 1:46am

My earlier post was a reference to the Greenwood and Hanke paper rather than Professor Lemieux’s article. The paper criticized economists for claiming that China exported deflation.

Some separate comments:

As the FRED graph shows, energy prices start and end interestingly close to the same values, but the paths otherwise look uncorrelated.

The paper blames inflation on a lag effect of the M2 spike that started in 2020. It criticizes the Fed and others for disregarding M2. Is M2 now relevant?

Pierre Lemieux

May 19 2022 at 1:51pm

Vince: On exporting inflation or deflation, Greenwood and Hanke argue that this is impossible, for the exchange rate adjusts. “A country” can only export relative prices (that’s comparative advantage), not the general price level.

On your last comment, that is the debate. Monetarists such as Greenwood & Hanke or I believe that the broad money supply is what determines the general price level. Or were you claiming that there is a better measure of the money supply than M2?

vince

May 20 2022 at 5:29am

As Knut Heen said, inflation needs to be defined. Gains from comparative advantage provide more goods for the same money. That’s deflation IMO.

On M2, what good is it without velocity? And who can predict velocity? Of course, M2 shouldn’t be frivolously jacked up.

Spencer Bradley Hall

May 20 2022 at 10:31am

There’s a much better measure of money than M2. M2 is mud pie. Banks don’t lend deposits. Deposits are the result of lending. Unless money is turning over, there is no inflationary impact. The ratio of savings deposit turnover to transaction deposit turnover, is 1:95.

And monetary lags are not long and variable. They have been mathematical constants for over 100 years.

The problem is measuring supply-side shocks. Peak oil is permanent.

Craig

May 20 2022 at 10:54pm

“On exporting inflation or deflation, Greenwood and Hanke argue that this is impossible, for the exchange rate adjusts. “A country” can only export relative prices (that’s comparative advantage), not the general price level.”

For many yeara the Chinese maintained an artificial peg of the yuan to the dollar while subsidizing exports.

Secondly, beyond China there are a few countries that are effectively dollarized, like tbe Bahamas, Belize, Ecuador, at one point Argentina.

Third, at the moment the USDX is going up which reflects dollar strength vs euros and yen. To the extent those countries utilize the dollar to buy their imports (think oil), that country will experience higher relative costs of that commodity relative to their currency even if the price of oil remains the same in US dollars.

Knut P. Heen

May 19 2022 at 11:35am

People should define inflation clearly before talking about it. If one price increases (say the wheat price), and all other prices remain constant, the CPI will increase. But that is not what we usually mean by inflation. If many prices increase because there is a war, the CPI will increase. But that is not what we usually mean by inflation. Inflation is not a concept in microeconomics. Microeconomics explains price changes by changes in supply and demand (war, less supply, higher prices). Inflation is a macroeconomic concept related to monetary policy (increase in the supply of money, same supply of goods, higher prices). In that sense, I agree with Friedman, inflation is a monetary phenomenon. Inflation increases CPI, but an increase in CPI does not imply inflation.

Stricter and stricter climate change policies month after month may increase energy prices month after month. A steady increase in the demand for energy in China month after month will also increase energy prices month after month. There are also at least one cartel (OPEC) involved in the energy market.

Pierre Lemieux

May 19 2022 at 1:42pm

Knut: I agree with your first paragraph, If I understand what you mean by your second paragraph, my agreement stops there. Suppose that in year 1, American consumers increase their demand from energy (from where does not really matter) and, consequently, decrease their demand for something else. The (relative) price of energy increases, the (relative) price of something else decreases. There is no inflation; the economy has just moved on the production possibility frontier towards more energy and less of something else. If American consumers do the same thing again in year 2, the economy moves again in the same direction on the ppf. As you said, demand, supply, and relative prices are microeconomic phenomena.

Knut P. Heen

May 23 2022 at 9:53am

Perhaps I misunderstood you. I was just trying to say that energy prices are increasing due to a combination of policy decisions regarding supply (particularly in Europe) and a gradual increase in demand from countries that consumed less energy 20-30 years ago. Energy prices are currently high in Europe too (in Euros). Energy prices world wide tend to be very correlated due to arbitrage possibilities (because coal, oil and LNG can be shipped).

Jose Pablo

May 20 2022 at 9:12am

“If one price increases (say the wheat price), and all other prices remain constant”

Can this really happen?

If one price increases, then the Pi*Yi for that product (say wheat) will increase (how much will depend on the elasticity of wheat). But if you assume MV = cte then some other Pj*Yj should decrease.

To have a generalized price increase you need M to increase (at least if you are not in the post-Friedman world of variable V of the 90s). Otherwise, if the “monetary consumption” (Pi*Qi) of one product goes up the “monetary consumption” of some others should go down.

Knut P. Heen

May 23 2022 at 10:10am

Probably not. It was just an example. A substantial disruption to the supply of wheat would increase the price of substitutes too.

Jose Pablo

May 23 2022 at 9:24pm

Not only that.

If you assume MV remains constant, the increase in prices (or to be more precise, in the contribution to the NGDP) of some products, like wheat or their substitutes, necessarily means that some other goods or services should reduce their contribution to the NGDP. Thru a reduction in their prices, their volumes or some combination of the two.

Knut P. Heen

May 24 2022 at 1:12pm

MV = QP is an accounting identity. It says people pay for what they buy. Why assume that the payment is constant? I don’t pay the same every month/year because I buy different goods every month/year.

Jose Pablo

May 24 2022 at 2:08pm

The Federal Reserve influences M thru different mechanisms and V (apart from being defined as NGDP / M, making the whole expression and “accounting identity” as you mention) is (or is supposed to be) a function of a “small” set of variables among then the return of bonds and equities (Friedman’s Quantity Theory of Money). The FED have also the ability to influence bonds prices (and equities too, as we have seen time and again).

You need changes in those variables (M and/or V) to have inflation and so, you need an explanation of why wheat price increases alter M and/or V and why the FED is incapable of counteract those changes thru its ability to influence both.

My point was that these explanations (and not the mere fact of pointing out the increase in the wheat and/or oil prices) are the relevant ones to explain inflation.

Jose Pablo

May 24 2022 at 2:37pm

As a matter of fact, during the pandemic, the FED was deliberately trying to “compensate” the 10% reduction in real GDP during the first two quarters of 2010. And they managed to do so: real GDP grew almost 13% in the next 5 quarters … and then some since price rose 5.6% during the same period.

Managing supply shocks is tricky since increasing M*V could result in additional inflation and decreasing M*V could result in additional reductions in real GDP.

The FED first tried the first approach (the whole “transitory thing” narrative) and is now in an “aggressive” path to try the second.

https://www.dallasfed.org/research/economics/2022/0113#:~:text=Nominal%20GDP%20After%20COVID%2D19&text=Private%20analysts%20were%2C%20in%20fact,percent%2C%20and%20prices%20were%20unchanged.

These dynamics explain inflation, not the reduction of the wheat/oil quantity in the market and the increase in their prices. Inflation is always and everywhere a monetary phenomenon and governments always try the same kind of excuses.

Friedman (1977)

“All other alleged causes of inflation—trade union intransigence, greedy business corporations, spend-thrift consumers, bad crops, harsh winters, OPEC [Organization of Petroleum Exporting Countries] cartels and so on—are either consequences of inflation, or excuses by Washington, or sources of temporary blips of inflation.”

Knut P. Heen

May 30 2022 at 6:15am

During the year without a summer, 1816, most food prices rose dramatically and it had nothing to do with monetary policy. The price of oats rose almost 8-fold.

https://en.wikipedia.org/wiki/Year_Without_a_Summer

Moreover, during the last year, the US Dollar has increased in value compared to almost all other currencies.

Jose Pablo

May 19 2022 at 9:01pm

Regarding the relationship between inflation and the (specialized!) press I have seen for the last couple of days multiple versions of this analysis:

“Driving the latest selloff have been continuing concerns around inflation, including how higher costs will eat into corporate profit margins” or “retailers aren’t able to profitably pass on higher expenses”

… but, if retailers are not passing higher cost to consumers, it means, I guess, consumers are not paying higher prices but if consumers are not paying higher prices, where is the Consumer Price Index measured inflation coming from?

Now I am lost.

Michael Rulle

May 21 2022 at 11:32am

Is it possible to empirically prove the cause of inflation at any point in time? It seems to makes sense that the more money chasing the same amount of goods should increase the price level. But we also know that turnover or velocity at any point in time can impact the price level.

Currently, If I am reading the FRED charts accurately, M2 is about 20 times velocity.In 2010 it was about 4.5 times velocity. However, velocity has increased about 2% in the last 2 years while M2 has increased between 20-25%.

Under the assumption that M2 is money, it would appear there is a correlation of inflation during the last 2 years (when velocity was almost flat) with the increase in M2 with little change in velocity.

So why is the Fed going so slow in reducing M2?

Or is my question just nonsense?

Michael Rulle

May 21 2022 at 11:51am

PS

In fact, velocity has declined in the last 18 months, while Money has increased 20+%. I know it cannot possibly be that simple, but Friedman’s concept was that velocity is relatively constant and therefore inflation was caused by money supply being too high. One reason M2 is so high is that NGDP has been so high. But why has velocity stopped declining?

Covid impacted output (combined with fiscal policy changes) so much that it is easy to see why the Fed has trouble forecasting conditions. I think they don’t think they know what is happening. Friedman knew money had to keep pace with growth——maybe we have no idea what growth will be by a larger amount than we are able to normally forecast.

Jose Pablo

May 21 2022 at 2:22pm

“Covid impacted output (combined with fiscal policy changes) so much”

I am growing more skeptical about this by the day:

Scott (2013):

(…) the average person thinks recessions are caused by big real shocks, or financial shocks, of one sort or another. Asset bubbles bursting, 9/11, stock market crashes, devastating natural disasters, etc.

It’s surprisingly easy to dispose of these real theories. We know that 9/11 didn’t cause the 2001 recession, because the recovery started just 2 months later. The biggest stock market crash in my life was 1987, which was almost identical to 1929, including the subsequent stock price rebound. The biggest natural disaster to hit a rich country in my lifetime was the 2011 Japanese earthquake/tsunami/nuclear meltdown, which killed tens of thousands of people, devastated a sizable area of Japan, and caused their entire nuclear industry (25% of total electrical output) to shutdown for more than a year (causing brownouts.)

(…)

But these real shocks don’t matter (very much) for business cycles. The tsunami did cause a temporary dip in industrial output, but nothing severe enough to constitute a recession. However when you turn your attention to the labor market you can really see how little real shocks matter”

Friedman (1977)

“All other alleged causes of inflation—trade union intransigence, greedy business corporations, spend-thrift consumers, bad crops, harsh winters, OPEC [Organization of Petroleum Exporting Countries] cartels and so on—are either consequences of inflation, or excuses by Washington, or sources of temporary blips of inflation.”

It seems that some “excuses by Washington” never fall out of fashion.

Knut P. Heen

May 23 2022 at 10:32am

Money was piling up on my account during Covid because there was nothing to spend it on (no travel, no restaurants, no sports). Online chess is “surprisingly” cheap compared to many other things.

Warren Platts

May 21 2022 at 2:26pm

Speaking of the M2 money supply, I was fooling around on FRED and decided to test the theory that MV = GDP (nominal). So I took the FRED M2 money supply X the FRED M2 velocity of money and the nominal GDP, normalized both to 1 starting in 2008, and as of the end of 2021, the MV ended up like 37% higher than the nominal GDP. Not bad I guess.. I wonder how they figure out what V is?

https://fred.stlouisfed.org/graph/?g=PGTu

Jose Pablo

May 21 2022 at 3:37pm

Velocity of M2 Money Stock (M2V)

Source: Federal Reserve Bank of St. Louis

Release: Money Velocity

Units: Ratio, Seasonally Adjusted

Frequency: Quarterly

“Calculated as the ratio of quarterly nominal GDP to the quarterly average of M2 money stock.”

So, no wonder it was “no bad”

Some theoretical attemps to define the “velocity function” measured that way

https://www.mercatus.org/publications/monetary-policy/what-would-milton-friedman-say-about-recent-surge-money-growth

Thomas Lee Hutcheson

May 21 2022 at 3:50pm

there would be a one-time increase in the general price level because the same quantity of money would be chasing fewer goods.

No, because there would not necessarily be “the same quantity of money” to “chase” fewer goods. The Fed’s job is to work with the hand it’s delt, whether that’s supply shocks or fiscal deficits.

Now it is probably true that the Fed would chose to allow inflation to temporarily accelerate (a one time increase the price level above the target trajectory) to allow for an increase in the relative price of the supply shocked good rather than trying to force some prices (which may be sticky downward) to fall in absolute terms.

Comments are closed.