David Beckworth recently conducted an excellent interview of Mike Bird, which is full of fascinating observations. At one point they were discussing the Hong Kong currency board, which since 1983 has fixed the exchange rate between the Hong Kong and US dollars. This exchange caught my eye:

Beckworth: Yeah. So, interestingly, the Fed sets monetary policy for Hong Kong effectively, right?

Bird: Yup. Absolutely, which is very noticeable in the Hong Kong housing market over the past 10 years or so.

I think that’s right. But this doesn’t necessarily mean what you think it means. While the US is setting the monetary policy in Hong Kong, that policy is nothing like monetary policy it sets in the US.

Because of arbitrage, interest rates tend to be roughly the same in any two free market economies with fixed exchange rates and open capital markets. Thus when the Fed moves its target short-term interest rate up and down, interest rates in Hong Kong tend to move in unison.

However, interest rates are not monetary policy. What matters is the difference between the policy rate and the equilibrium interest rate. For simplicity, let’s assume the equilibrium rate is the interest rate that maintains 2% inflation. (In practice, employment also affects the equilibrium rate.) In the US, the Fed moves the policy rate up and down in an attempt to keep interest rates close to equilibrium. This doesn’t work perfectly (inflation fell to 0% in 2009) but overall the Fed does a reasonably good job of keeping inflation close to 2%.

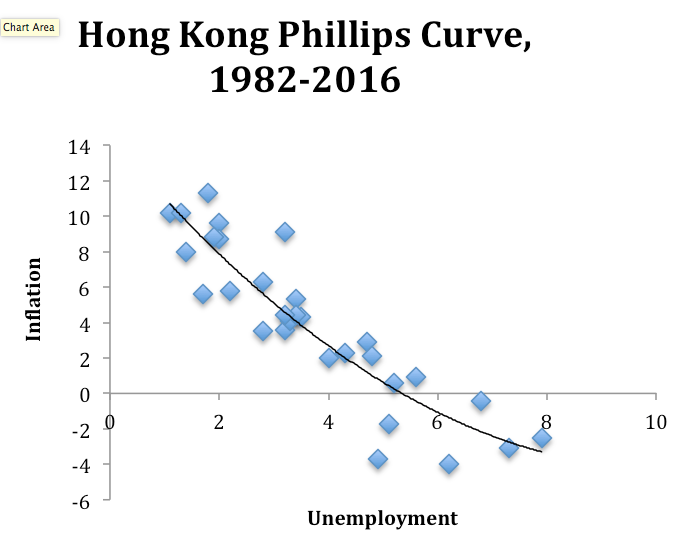

But the equilibrium interest rate in Hong Kong is very different from the equilibrium rate in the US. As a result, there are often wide gaps between the actual interest rate in Hong Kong and the equilibrium rate. This causes wild swings in inflation, from double digits to negative 4%. These wild swings in monetary policy result in the Hong Kong economy being dominated by demand shocks, one of the three prerequisites for the Phillips Curve model to work.

Interestingly, Hong Kong also has the other two prerequisites for a stable Phillips Curve. First, inflation expectations are stable due to the US dollar peg combined with the Fed’s 2% inflation target, despite big fluctuations in actual inflation. And second, the natural rate of unemployment is stable due to Hong Kong’s relatively laissez-faire labor market regulations. Put the three together and you have one of the few countries where the Phillips Curve still holds:

We should all thank Hong Kong for being willing to perform a natural experiment as to what would happen if you arbitrarily used monetary policy to create large swings in actual inflation, in an economy with stable inflation expectations (roughly 2%) and a stable natural rate of unemployment (roughly 4%).

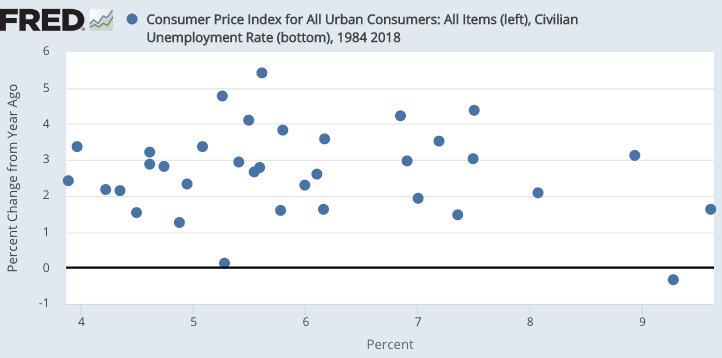

PS. This also explains why the Phillips Curve is such a bad model. There are very few countries where all three Phillips Curve prerequisites hold true. And the US is not one of them. The Fed should stop relying on the Phillips Curve.

READER COMMENTS

Brian Donohue

Jun 21 2019 at 4:45pm

Very clever.

ChrisA

Jun 22 2019 at 3:49am

Agreed. With empirical data like this, who can deny the monetary framework is the right way to do macro-economics. The theory is sound but that doesn’t always transfer into empirics.

Basil H

Jun 21 2019 at 5:50pm

If you’re not already familiar: Jorda, Schularick, and Taylor have a cool paper generalizing this same idea in a panel of countries across pegged exchange rates during the 20th century, to estimate the effect of monetary policy shocks.

https://sites.google.com/site/oscarjorda/home/files/MP_Text_07may2018_OJ.pdf?attredirects=0

marcus nunes

Jun 21 2019 at 10:02pm

Hong Kong´s PC also satisfies the “geography restriction”

https://thefaintofheart.wordpress.com/2015/01/31/geography-is-a-great-predictor/

Thaomas

Jun 22 2019 at 9:24am

DOES the Fed rely on a Philips Curve?

It seems like they have an ironclad inflation rate ceiling combined with a half hearted commitment to full employment with some funny notion of interest rate “normality” plus some vague fears of financial “instability” which has resulted in movement in their instruments that have been insufficient to maintain 2% average inflation, much less until recently, full employment.

BTW, do you agree with this from Brad DeLong

Njnnja

Jun 22 2019 at 9:00pm

Has anyone checked if the Phillips curve hold for other jurisdictions such as the Commonwealth of Massachusetts or the State of Florida? They “peg” their currency to the FRB despite having different drivers, which seems similar to HK, and state by state inflation and unemployment numbers are tracked.

If if it doesn’t hold, what is the difference between a state and HK?

Scott Sumner

Jun 24 2019 at 1:17am

Njnnja, One difference is that the Fed cares about the economy of states, but not HK.

I’d guess that the PC works better at the state level than the national level. A boom would push up housing costs for instance, and vice versa.

Kurt Schuler

Jun 22 2019 at 9:04pm

From 1983 to 2018, Hong Kong’s real GDP per person in purchasing power parity terms rose from 60% of the U.S. level to 103%, according to the IMF’s World Economic Outlook database. Hong Kong is the second most populous place without huge oil or gas deposits (behind Switzerland) to have a GDP per person exceeding the United States. Not a bad result from what you term “wild swings in monetary policy.” Maybe you are underestimating the stabilizing effect of the exchange rate and overestimating the stabilizing effects of other possible monetary targets.

Scott Sumner

Jun 24 2019 at 1:19am

Kurt, That’s completely consistent with my view of macro, which is that demand shocks don’t affect long run growth.

So no, I did not underestimate the stabilizing effects of exchange rates, because what you report is exactly what I would have expected from the world’s freest economy.

kathmandu

Jun 23 2019 at 8:05am

Hi Scott, do you think Hong Kong would be better without the peg?

Scott Sumner

Jun 24 2019 at 1:20am

I have no idea.

Matthias Görgens

Jun 29 2019 at 9:59am

Another alternative would be a soft peg to a basket, like Singapore does.

But yeah, answering the question about those counterfactuals is hard.

But Hong Kong doing well despite these shocks does actually bode well for anyone looking to revive the classic gold standard one country at a time.

Ricardo Martins

Jun 24 2019 at 5:46pm

Do you know about Nick Rowe paper on this?

https://sciencessociales.uottawa.ca/economics/sites/socialsciences.uottawa.ca.economics/files/0201E.pdf

Comments are closed.