There are two ways of thinking about the relationship between monetary policy tools and monetary outcomes.

Standard approach: The standard view is that lower interest rates lead to higher NGDP growth. In addition, a bigger monetary base leads to a higher NGDP.

Alternate view: An alternative approach starts from the assumption that the central bank will do whatever it takes to hit its target, and then asks what the equilibrium interest rate, or equilibrium monetary base, looks like after the target is achieved.

In the alternative approach, higher NGDP growth rates lead to higher nominal interest rates, inverting the relationship in the standard approach. Furthermore, higher NGDP growth rates lead to a lower demand for base money. Thus the demand for base money is roughly 4% of GDP in Australia, 20% of GDP in the US, and 100% of GDP in Japan. That’s because demand for base money is strongly linked to nominal interest rates, which are strongly linked to NGDP growth.

In the standard view, there is often “pessimism” about monetary policy. I use scare quotes for ‘pessimism’ because the fear being described is actually a wonderful outcome, beyond our wildest dreams. The end of scarcity. It describes a world where the Japanese could print up enough money to buy the entire world, stop working, and live off the fruits of the 98% of humans that are not Japanese.

Proponents of pessimism argue that monetary policy may be unable to hit its targets, i.e. may be unable to debase the currency as much as central bankers wish, and also argue that my “buy the world” hypothetical is impractical—too risky.

Interestingly, this pessimism does not apply to one policy tool—exchange rates. No one doubts that pegging the Japanese currency at 1000 yen to the dollar would successfully debase the yen. So no one seriously believes that central banks are powerless in a technical sense. Rather the concern is that a major debasement would be too risky. It would force the BOJ to buy up lots of foreign assets in order to meet the much higher demand for yen at the debased value.

I don’t know about you, but if the yen were suddenly debased from 110 to the dollar to 1000 to the dollar, that would not make me want to go out and stuff my safety deposit box with yen currency. So I don’t believe the BOJ would have to buy lots of foreign assets to push the yen up to 1000 per dollar.

With smaller devaluations, however, I can imagine something like what the skeptics suggest. Suppose the Swiss depreciated the SF from 1 euro to 0.83 euros, and then peg it there. Also suppose that investors believed the Swiss would eventually reverse this policy and raise the SF back up to equality with the euro. The initial depreciation of the SF might lead people to invest in the currency, expecting a future appreciation. In that case, to keep the SF pegged at 0.83 euros they would need to buy enough assets to supply the Swiss currency being demanded by speculators.

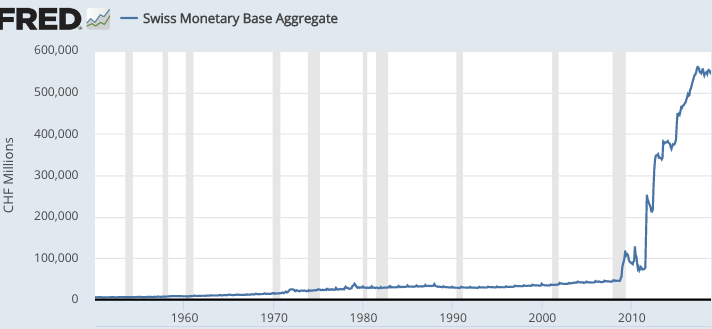

Now suppose the Swiss central bank did not want to accumulate lots of assets. What is the absolutely worst possible thing they could do? The answer is obvious. They should definitely not allow the SF to later appreciate, as that would validate the expectations of those speculators who had purchased SF in expectation of an upward revaluation.

And yet, that’s exactly what the Swiss National Bank did in January 2015. Even more shockingly, their rationale for this action was that it would allow them to have a smaller balance sheet.

Where did the Swiss go wrong? The SNB took the “standard approach”, assuming a bigger monetary base went along with easier money. In fact, in the long run exactly the opposite is true. Because currency pays no interest, speculators prefer to hold currencies that appreciate in value over time.

READER COMMENTS

Garrett

Jan 30 2019 at 4:06pm

That’s an embarrassing chart if their stated goal for the policy was to reduce their balance sheet. Has the SNB commented on the result since the policy was implemented?

Scott Sumner

Jan 30 2019 at 7:24pm

Garrett, I’m not sure.

Benjamin Cole

Jan 30 2019 at 8:38pm

The Japanese situation, in which the Bank of Japan has purchased 45% of that nation’s huge pile of Japanese government bonds, which equal 225% of GDP, is disconcerting.

Perhaps the Bank of Japan should try buying foreign bonds, and use the interest earned to lower taxes on Japanese citizens.

Given the Japanese experience, I do not see why a discussion of money financed fiscal programs is never even on the table.

Ben Bernanke advised Japan to go to money financed fiscal programs in 2003. Unfortunately, the Bank of Japan did not heed Bernanke’s advice and so we do not have an experiment about this policy tool.

The historical record is that money financed fiscal programs were extraordinarily successful in Japan in the Great Depression, in fact the Great Depression was largely sidestepped by the great Finance Minister Korekiyo Takahashi—- a history mysteriously untaught in Western universities.

Gadzooks! When conventional thinking is sacralized, you do not get economists but rather econo-shamans.

Scott Sumner

Jan 31 2019 at 1:24pm

Because it’s a foolish and wasteful policy and there’s no need for it, as I’ve pointed out 100 times. Do you have any comment on those earlier posts?

Keenan

Jan 31 2019 at 10:22am

Scott, I’m confused about one issue. Does my logic make sense here?

Currently, 1 USD = 100 Yen. So, if BOJ sets a peg at 1 USD = 1000 Yen:

I will take my dollars and convert them to yen

I will then go buy stuff with my yen

Enough people will do this that the price of things sold in yen will soon be 10x what it used to be.

When you say

“Rather the concern is that a major debasement would be too risky. It would force the BOJ to buy up lots of foreign assets in order to meet the much higher demand for yen at the debased value.”

Are you saying that when I (and others) do step 1 from above that there might not be enough yen in circulation to meet this new demand? If so, is it necessary that the BOJ buys lots of foreign assets? Wouldn’t buying any asset (even domestic) do the job of creating more yen in circulation?

Thanks

Matthias Goergens

Jan 31 2019 at 10:46am

Think about the people selling you those assets for yen. Wouldn’t they expect you to pay the debased prices? Almost right away, not just after enough people do this.

Rational expectations and efficient markets and all that. They anticipate what’s happening, so not a lot of stuff actually has to happen before the prices shift.

I think Scott Sumner coined the phrase ‘long and varying anticipation’ in the Midas Paradox in contrast to the established ‘long and variable lags’ view of monetary policy.

Keenan

Jan 31 2019 at 11:00am

Totally agree that the price level in Yen could 10x in a matter of minutes, and if I was selling stuff in Yen, I am definitely going to 10x my prices immediately. Steps 1, 2, and 3 could take place in 10 seconds, but they are still taking place.

Scott Sumner

Jan 31 2019 at 1:22pm

Keenan, They could decide to only buy domestic assets, as you say, and that would certainly “work”. I think the concern is that they might run out of the sort of domestic assets that they prefer to buy, and not want to buy riskier domestic assets. Thus the demand for foreign assets.

Keenan

Jan 31 2019 at 2:50pm

Makes sense. Thanks!

Comments are closed.