Average home prices remain very close to the all-time highs reached at the beginning of the year. Accordingly, public opinion surveys show rising concern about the issue of housing affordability, and politicians are taking notice. The Trump administration has waded in with a potentially forthcoming national housing emergency declaration so the President can do… something. We may have to wait until a decree is issued to see what exactly Mr. Trump thinks his emergency powers are in the realm of housing policy.

But are houses really more expensive over the long run, or is it just an economic mirage? As an economist with a background in residential construction, I think about this issue often.

When I read articles about the housing affordability crisis, I tend to agree with the economically-informed consensus that America has a fundamental housing supply problem. A combination of regulatory constraints—zoning, permitting, energy-efficiency standards, occupational licensing, etc.—raises home construction costs. Tariffs and the purge of illegal immigrant labor are not helping, either. I endorse the argument that regulatory easing would make housing significantly more affordable.

On the other hand, I sense that much of the fuss about ever-rising home prices is based on incomplete analysis. It does not account for enough of the relevant factors to provide a satisfactory explanation of the observed trends in the data. Good economic analysis must hold other factors constant—the famous ceteris paribus assumption. When it comes to home price analysis, there’s a raft of other factors to consider. Some fairly simple calculations with easily available data support an argument that home prices are not significantly higher than their long-run average.

The Other Factors that Matter in Housing

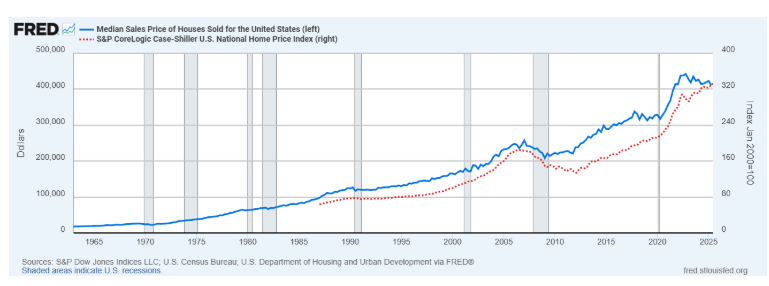

So what are the ceteris we must hold paribus when analyzing long-run trends in US home prices? Let’s start with the big, obvious one: inflation. We can’t compare nominal home prices from 2019 to 2025 (CPI grew 26% over these six years alone), much less from 1990 or 1960 or whatever date one selects as the golden age of affordability.

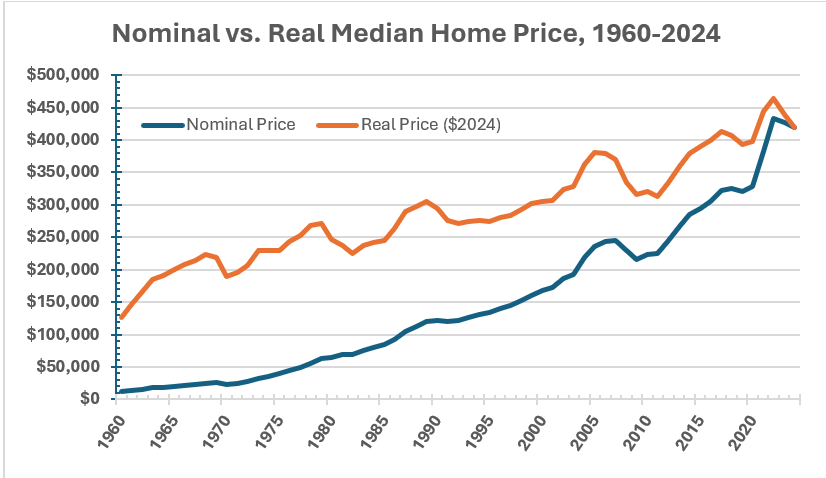

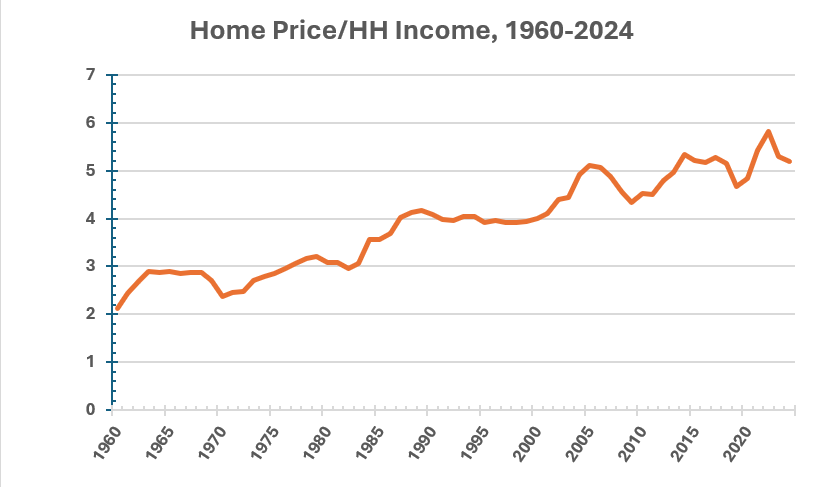

Let 1960 (the earliest year for which I can obtain data points for all of my ceteris paribus categories) represent the paragon of home affordability in the US. While the nominal median home price rose by 3,421% from 1960 to 2024, adjusting this for inflation using the Consumer Price Index shows a more modest but perhaps still distressing rise of 232%. But let’s now also factor in much smaller, but significant, growth in household incomes over this time frame. The typical practice is to divide the median home price by the median household income to get the home price/ household income ratio. In real terms, this ratio rose from about 2.1 to about 5.2, or 145%, over the same time frame.

Next, let’s consider what, exactly, people are getting with their purchase of the median home. In 1960, the median home built in the US was 1,500 square feet. Median home size rose steadily, peaking at about 2,700 square feet in the mid-2010s before declining slightly to 2,400 square feet in 2024. Assuming bigger is better and that people are happy to shell out more money for more house, we can adjust for this size factor by calculating real home price per square foot of home size. This metric increased by 107% from 1960 to 2024. Still a large increase, but far more manageable than that raw real median price by itself or adjusted merely for household incomes.

We’re getting closer, but I want this to be a comprehensive adjustment. One very important analytical factor I learned from the great Thomas Sowell is to be on the lookout for composition effects, or changes in the characteristics of groups over time that can skew simplistic statistical snapshots. Sowell teaches us to be on the lookout for composition effects in any household statistic, because household size can and does change significantly over time. In 1960, the average US household was 3.33 people. This figure dropped to about 2.5 by the 2020s, with most of that decline taking place before the 1990s.

This means that the median household income is divided amongst a smaller number of household members, understating the growth of household income over time on a personal level. In other words, real median household income per person went up by more than is apparent in the overall household income data series. We can factor this into our home price analysis by calculating the ratio of real home price to real household income per person. This metric rose by 96% over the 1960–2024 period.

Finally, let’s combine the change in home size along with the change in household composition in that last calculation. Our final adjustment results in the ratio of real home price per square foot to real household income per person. Drumroll, please: by this comprehensively adjusted metric, housing affordability rose by a paltry 6% from 1960 to 2024, and is actually down substantially from its peak in the late 1970s.

Moreover, all of these adjustments do not account for perhaps the most important change: that of home quality in terms of features and amenities that have become more common over the years. I have yet to find an index of home quality that tracks these attributes in a reliable way. I do have a strong impression, based on personal experience and tidbits of data, from which I arrive at a confident conclusion that today’s homes are nicer places to live than those of 30 or 60 years ago. As a 2011 US Census report summarizes, in addition to larger home sizes, “homes built today have almost more of everything—different types of rooms such as more bedrooms and bathrooms, more amenities such as washers and dryers, garbage disposals and fireplaces, and more safety features, such as smoke and carbon monoxide detectors and sprinkler systems.” Today’s bigger, roomier homes also have more energy-efficient utilities, more user-friendly appliances, more garage space, bigger and more well-appointed kitchens where stone countertops replaced Formica, and so on. If we could find a way to factor in all of these changes to the comprehensive home price adjustment, it might show zero change or even a fall in home prices, ceteris paribus.

In conclusion, the housing affordability crisis is a nothingburger!

While it’s important to think carefully about the changes in the ceteris, I want to reiterate that there is a housing price problem, and it deserves attention and a smart public policy response. I hope my “comprehensive” real home price adjustments here are thought-provoking, but this analysis is lacking in at least two major ways: 1. It cherry picks the start and end points; 2. It’s national aggregate data, so it does not pick up regional variations in home price changes over time.

If you look at ten-year spans, there’s a lot of fluctuation in home price shifts, even by my preferred ratio of real home price per square foot to real household income per person metric. 2024 prices were 22% higher than 10 years prior, giving the up-and-coming generation ample grounds to complain that home prices are getting out of reach. The recent spurt of home appreciation also validates the complaint that housing markets serve to transfer wealth from poorer millennials to well-off boomers. Housing price growth also varies greatly by region. Hot markets—mostly coastal and sunbelt metros—saw 10-year price growth at 1.5 to 2 times larger than the national average. Cooler markets in parts of the south and Midwest saw growth rates not much higher than overall CPI inflation.

As this excellent map from Visual Capitalist shows, it is much easier to afford a house (ceteris paribus, of course!) in the Midwest than in the West, Northeast, or Florida. (I knew there had to be a compensating differential for our miserable Michigan winters!)

Getting a handle on escalating home prices is a simple, but not politically easy, fix. We need to claw back the relative growth in home construction costs. In other words, we need the housing supply curve to “shift to the right” more than the demand curve has shifted. Builders know exactly what this would take: less restrictive zoning (especially for multifamily units), easier licensing and permitting processes, less stringent building codes and energy standards, freer markets in labor and materials, and maybe a consumer acceptance of smaller, simpler homes.

Dataset and calculations available upon request: tylerwatts53@gmail.com

Tyler Watts is a professor of economics at Ferris State University.

READER COMMENTS

David Henderson

Oct 9 2025 at 12:38pm

Excellent post, Tyler. I learned a lot.

One correction. You write, “by this comprehensively adjusted metric, housing affordability rose by a paltry 6% from 1960 to 2024, and is actually down substantially from its peak in the late 1970s.”

But when something becomes pricier, affordability doesn’t rise.

Tyler Watts

Oct 14 2025 at 11:50am

Thanks, David! Should have read “unaffordability”–I need to improve my proofreading.

Ron Browning

Oct 10 2025 at 6:30am

The superior quality of a modern home versus an older home is at least a bit superficial. The quantity and quality of the wood that makes up the structure of most homes has substantially decreased over the years. The 1955 home probably did not compare well with the 1990 home in 1990. 35 years of wear has changed the comparison. The likelihood of the 1990 home outlasting the 1955 home is questionable. The 2025 home is more feeble yet.

Jon Murphy

Oct 10 2025 at 7:18am

I second Ron’s comment. Quality can be an issue. Just some anecdotes from my small view of South Louisiana:

My apartment complex (built in 2021 to supposedly Category 4 hurricane standards) suffered extreme damage from Hurricane Francine last year (a high Category 1/low Category 2 storm when it hit us). Roofs ripped off, windows blown in, etc. The “luxury homes” neighborhood they built just outside of town had to be evacuated because they never connected the houses to the sewer system and raw sewage was just being released into the ground. Same neighborhood: foundations were cracking within months of being built.

Conversely, my 40 year old condo has survived 2 Category 5 storms (Katrina and Ida), one of which was a direct hit. My girlfriend’s 70 year old home survived 3, two of which were direct hits. Now, there certainly is survivor bias here, so take these simply as anecdotes, but I think a quality story can be told too.

steve

Oct 10 2025 at 1:00pm

It’s a mixed bag. Older homes have old growth lumber which is denser while new homes make use of softwoods which are farmed for rapid growth. However, modern engineered structural beams are stronger and more durable on average. Modern homes are safer and better insulated. So the older homes that lucked out and have natural beams that are above average and have been lucky to avoid a fire might actually last longer.

Also, you cant just focus on the wood. Those older homes likely have knob and tube wiring which didnt go away until the 40s-50s. The insulation was poor on that wiring as a rule, it had no ground wire and will overload/overheat with a lot of modern appliances. My group bought a house to use for taking call at one of our rural hospitals. It had knob and tube wiring which we had to update. I can run romex but we needed a real electrician for that.

Steve

Jon Murphy

Oct 10 2025 at 1:48pm

All good points, Steve. I was thinking on structure, but the wiring and plumbing certainly matters too. I have friends who just bought a beautiful old home in Massachusetts. But they had to spend a substantial amount of money upgrading the plumbing; it just wasn’t able to cope with modern appliances.

Jon Murphy

Oct 10 2025 at 7:23am

In what may seem like a contradiction to my comment in support of Ron, I think Dr Watts makes an excellent argument here. He helps clear up a clear contradiction in the data: housing is supposedly unaffordable at a historic rate, yet home ownership levels remain high by historical standards. Homes could certainly be more affordable by reducing NIMBY and increasing supply, but the housing affordability crisis is likely overstated.

Mark Brophy

Oct 20 2025 at 2:32pm

If houses were unaffordable, people would move into smaller houses or commute further to work. Most people bought houses at unreasonably low interest rates, endangering banks, encouraging government banking bailouts.

Matthias

Oct 10 2025 at 9:44pm

I have a feeling that you are mixing up a few different things.

And it feels like you are double counting in a sense: richer people somewhat understandably want to live in bigger and better houses. So it feels a bit strange to adjust for both income and for house sizes (and quality).

Btw, if you still want to adjust for income anyway, then there’s no need to muck around with inflation numbers: the price level cancels out when you look at nominal income Vs nominal housing costs. Unless you want to use different measures of inflation for the two, but that would be hard to justify.

Furthermore, it’s probably better to break this up into multiple perspectives. You can look at how many hours per month the average person has to work to afford one square metre of living space. (Either to rent or to pay the mortgage and maintenance.)

Naturally, thanks to technological progress and massively increasing incomes, we would expect that measure of the real price of housing to fall.

Your numbers show that it barely moved at all. So something is very wrong.

Thomas L Hutcheson

Oct 11 2025 at 10:00am

Kenneth Erdman suggests that unnecessarily strict prudential limits on mortgage lending post 2008 contribute to the no small house issue.

Knut P. Heen

Oct 13 2025 at 11:13am

People are not snails. If people tend to move from let us say Michigan to California. There will be empty houses in Michigan and unaffordable housing in California. At least until the politicians realize that people are not snails.

Comments are closed.