Broadly speaking, there are three types of economists. Those who believe the real problems in the world are due to real factors, those who think the real problems in the world are due to a lack of aggregate nominal spending, and those who put roughly equal weight on both factors. Over the past decade, I’ve often done Powerpoint presentations of the Great Recession, entitled “The Real Problem was Nominal”. Today, I’ll describe where the real problem is real.

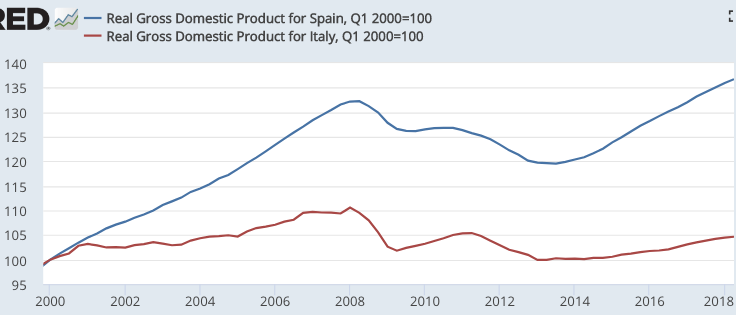

Consider the path of RGDP in Spain and Italy, since 2000:

Spain’s RGDP is up about 37%, while Italy’s has risen by 5%. So are Italy’s problems due to the euro, as many pundits seem to assume? Yes and no. If you are looking at the severe Italian slump from 2008-13, then the tight money policy of the ECB was indeed the main problem. Notice that Spain suffered an equally severe slump, for the same reason. Other countries such as Germany and Netherlands had a milder slump, due to a combination of a better product mix and a sounder economic regime.

Spain’s RGDP is up about 37%, while Italy’s has risen by 5%. So are Italy’s problems due to the euro, as many pundits seem to assume? Yes and no. If you are looking at the severe Italian slump from 2008-13, then the tight money policy of the ECB was indeed the main problem. Notice that Spain suffered an equally severe slump, for the same reason. Other countries such as Germany and Netherlands had a milder slump, due to a combination of a better product mix and a sounder economic regime.

But if you compare Spain and Italy over the past 18 years, it’s clear that Italy’s problems are not just cyclical. For some reason, the trend rate of growth in Italy is much lower than in Spain. There are probably a number of factors involved, including the fact that Spain started from a lower income level and has had somewhat faster population growth. However, it’s increasingly clear that Spain also has a better economic model, and that Italy needs to reform its economy.

Unfortunately, the new Italian government seems opposed to economic reforms, so Italy’s economic future looks bleak. For instance, the “conservative” leader in Italy’s new (populist) coalition government recently blamed EU spending caps for the Genoa bridge collapse. This in a country that where the government already spends over 50% of GDP! (In contrast, the German government spends 44%, and I don’t recall reading about major German bridge collapses.)

From Britain to Italy, the EU has become a convenient whipping boy for every problem imaginable. Consider this recent FT article:

The US president’s reckless threats to double the tariffs on steel from Turkey have sent the Turkish lira crashing on the foreign exchanges. They are also putting French, Spanish and Italian banks with substantial investments in Turkey in serious jeopardy.

Given the possibilities for contagion, another European banking crisis could be around the corner. But this is not all Mr Trump’s fault. If you live in an earthquake zone and do not take out earthquake insurance, that is your fault.

There would be no cause for concern had the European authorities put an EU-level deposit insurance programme in place to assure depositors that their money would be safe. Then there definitely would be no run on European banks.

But popular sentiment in Germany and the Netherlands that it would be the Germans and Dutch who would wind up paying for the deposit guarantee scheme won the day.

Readers know that I’m no fan of Trump’s trade polices, but it’s pretty far-fetched to blame Trump for Turkey’s economic problems. Turkey was already in crisis before the steel tariffs, which apply to only a small percentage of Turkey’s exports. But even if I’m wrong, it’s a real stretch to use Turkish steel tariffs as an excuse for banking instability in countries such as France and Italy. How much of their balance sheets represent loans to Turkish steelmakers? If European banks can’t survive a hiccup in a single (traditionally unstable) developing economy, when the global economy is strong, then they must have taken wildly excessive risks in their lending. But the FT seems dismissive of the moral hazard problem:

Keeping the EU together is what is most important. And if that means some residue of moral hazard, so what?

Some pundits tell us that 18 years of Italian stagnation is caused by “austerity”, by the Italian government spending “only” 50% of GDP and increasing the public debt to only 130% of GDP. Others tell us that the way to address grossly irresponsible bank lending is to increase moral hazard, providing even more incentives to behave recklessly.

There is an alternative vision, which rejects the one-sided solutions of both the left and the right:

1. Adopt a monetary policy of stable NGDP growth, because the right is too prone to view all problems as being real problems.

2. Adopt a neoliberal policy regime where people have incentives to create wealth without taking excessive risks, because the left is too prone to view all problems as being nominal problems.

In other words, don’t be a demand-sider or a supply-sider. Be a supply and demand-sider. Don’t be like Germany, ignoring nominal shocks, or Italy, ignoring real problems. Be like Australia, a country with persistent NGDP growth and a neoliberal policy regime.

PS. Speaking of neoliberalism, check out this interview of Sam Bowman, who has a set of policy views that are quite close to my own. The two guys interviewing Sam are amusing at times, and I was particularly interested in Sam’s discussion of how greatly the UK political discourse is influenced by developments in the US (after the 50 minute point.)

READER COMMENTS

E. Harding

Aug 21 2018 at 5:40pm

Good take, Sumner. I made this point in your blog’s comments a couple years ago.

http://www.themoneyillusion.com/yes-interest-rates-really-do-impact-the-demand-for-money/#comment-483745

https://againstjebelallawz.wordpress.com/2016/01/03/europe-the-real-problem-is-real/

Greece also has this problem:

https://fred.stlouisfed.org/series/CLVMNACSCAB1GQEL

Lorenzo from Oz

Aug 21 2018 at 6:31pm

And the systematic undermining/destruction of accountability is my biggest single issue with the EU. Along with the consequences thereof.

B Cole

Aug 21 2018 at 8:26pm

I do wonder if the EU is a good idea. The ECB is probably a bad idea.

Italians will be Italians.

B Cole

Aug 21 2018 at 9:24pm

https://www.theatlantic.com/international/archive/2018/08/greece-bailout-imf-europe/567892/

Galbraith’s point of view is interesting. I think he could have strengthened his article by pointing out that Greek GDP is still down 25% from 2008.

Galbraith also does not mention that Greece needs its own currency.

It is funny how failures become institutionalized, when government is involved. By what measure has Greece joining the EU been a success?

Yet they cannot leave!

Scott Sumner

Aug 21 2018 at 10:36pm

Lorenzo, Yes, and the more the EU does, the more it undercuts accountability for national governments. A simple free trade zone with labor mobility would have been better.

Thaomas

Aug 22 2018 at 6:16am

The key problem is that the Eurozon does not have a good way to deal with sovereign debt crisis and too many private lenders in the past have ignored country risk when making cross-border loans. This, along with the too-low price level growth target by the ECB just made the bad idea of the Euro worse.

Jean

Aug 22 2018 at 8:29am

In September of 2008 Deutsche Bank was leveraged out 55 to 1!

Scott Sumner

Aug 22 2018 at 2:44pm

Jean, Good example.

Comments are closed.